Global equity markets displayed a mixed performance on Wednesday, as investors digested the US Federal Reserve’s latest monetary policy decision. While the central bank implemented its second interest rate cut of the year, Chair Jerome Powell’s subsequent remarks cast doubt on the likelihood of further easing in December, prompting a significant reversal in sentiment. This hawkish commentary led to a retreat in broader indices, with the Dow giving up earlier gains, while the technology-heavy Nasdaq Composite managed to advance, lifted by strong corporate earnings in the sector.

Key Takeaways:

- Dow Reverses After Record High: The Dow Jones Industrial Average slipped 74.37 points, or 0.2%, to 47,632.00 after rising more than 300 points earlier in the session to a new all-time high. The reversal came after Powell stated that a further cut in December was “not a foregone conclusion,” prompting caution and pushing consumer and payments names including Costco, McDonald’s, Visa and Mastercard lower.

- S&P 500 Ends Slightly Lower: The S&P 500 closed slightly lower at 6,890.59, with sector performance mixed as markets reassessed the likelihood of continued policy easing. Powell noted that inflation progress remains uneven, highlighting “strongly differing views” within the committee.

- Nasdaq Outperforms on Tech Strength: The Nasdaq Composite rose 0.55% to 23,958.47, supported by a 3.1% rise in Nvidia, which briefly crossed the $5 trillion valuation mark, becoming the first US company to do so. Alphabet gained after beating revenue expectations and signalling higher capital spending linked to AI and cloud growth. Microsoft reported strong quarterly results, though shares eased in extended trading.

- European Equities Conclude Lower Despite Select Earnings Boost: European stock markets ended Wednesday’s session predominantly lower, with the pan-European Stoxx 600 index finishing down 0.1%. Major indexes and sectors across the continent displayed mixed performances. While Germany’s DAX fell 0.64% to 24,124 and France’s CAC 40 was down 0.2%, the UK’s FTSE 100 index closed up 0.6% at 9756.14. Italy’s FTSE MIB rose 0.3%, and Spain’s IBEX 35, which has shown strong performance recently, ended the session up 0.4%. Luxury carmaker Mercedes-Benz Group saw its shares gain 4.5%, marking its best trading day since 2022, despite reporting a 70% fall in third-quarter operating profit. Meanwhile, British lenders approved more mortgages in September than in any month so far in 2025, and the Spanish economy grew 0.6% quarter-on-quarter in the three months to September 2025, driven by domestic demand. Portugal’s unemployment ticked up to 6.0%, while Belgium recorded modest quarter-on-quarter GDP growth of 0.3%.

- Asian Markets See Mixed Performance; Nikkei Hits Record: Asian markets presented a mixed picture, with Japan’s Nikkei 225 index jumping 2.17% to hit a record high, crossing above 51,000 for the first time and closing at 51,307.65. This surge was fuelled by renewed optimism over US-Japan trade ties following a new rare earths framework signed by President Donald Trump and Prime Minister Sanae Takaichi. Conversely, the Topix lost 0.23% to end at 3,278.24. South Korea’s Kospi rose 1.76% to 4,081.15, while the small-cap Kosdaq lost 0.19%. Australia’s S&P/ASX 200 declined 0.96% after consumer prices rose 3.2% in the third quarter, exceeding expectations. Mainland China’s CSI 300 was up 1.19%, and India’s Nifty 50 gained 0.45%. Hong Kong markets remained closed for holidays. US-China trade tensions appeared to alleviate, with President Trump indicating he expects to cut fentanyl-related tariffs on China.

- Treasury Yields Surge Following Powell’s Remarks: Treasury yields experienced a significant increase following Federal Reserve Chair Jerome Powell’s comments, even after the central bank cut rates for the second time this year. The benchmark 10-year Treasury yield climbed over 8 basis points to 4.072%, while the 2-year Treasury note yield added more than 10 basis points, reaching 3.602%. The 30-year bond yield also rose over 6 basis points to 4.613%.

- Oil Prices Advance on Inventory Drawdowns and Trade Optimism: Oil prices rose on Wednesday, driven by larger-than-expected declines in US crude and fuel inventories, alongside easing economic jitters from US-China trade optimism. Brent crude futures gained 53 cents, or 0.8%, to settle at $64.93 a barrel, while US West Texas Intermediate (WTI) crude futures advanced 40 cents, or 0.7%, to $60.55. Data from the US Energy Information Administration showed crude oil stocks fell by nearly 7 million barrels, significantly more than the anticipated 211,000-barrel drop, prompting a reassessment of expectations for a large market surplus.

FX Today:

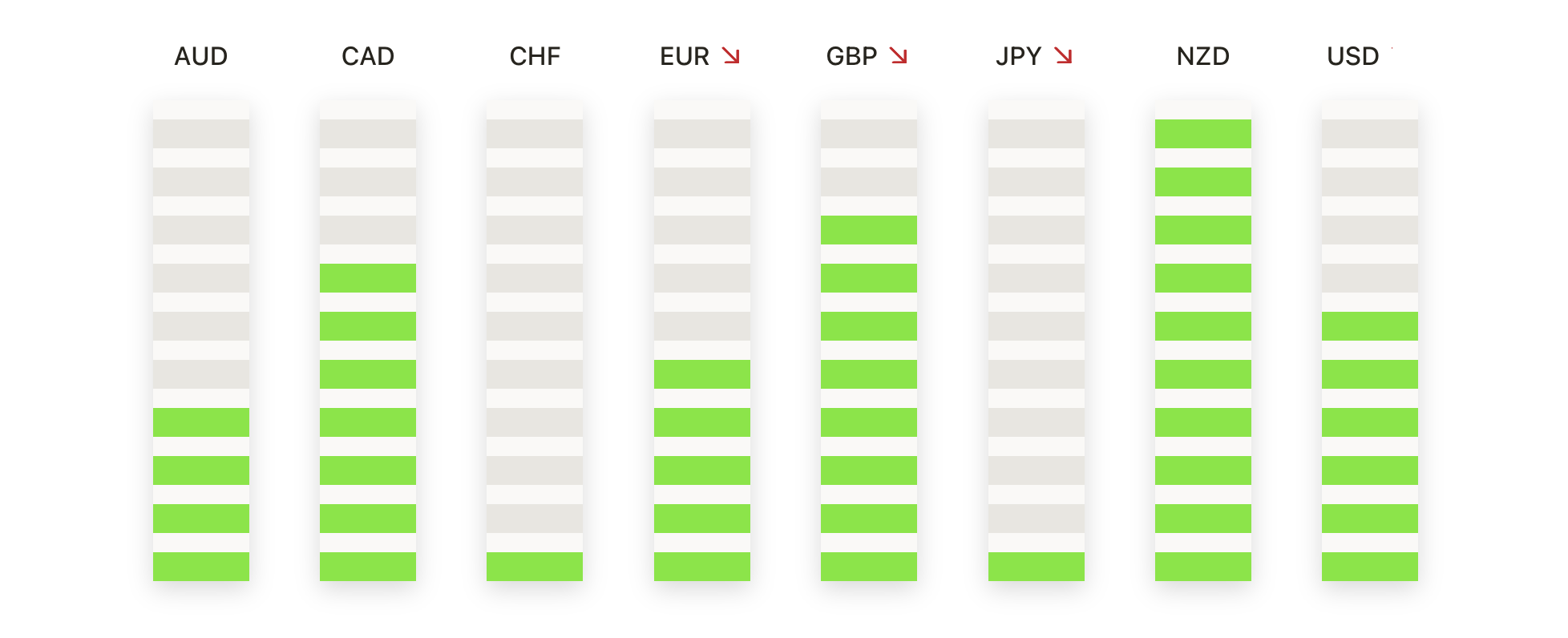

- EUR/USD Drifts Lower: EUR/USD closed at 1.1598, down 0.45%, after moving between 1.1666 and 1.1578. The pair remained under steady selling pressure throughout the session, reflecting a continuation of recent downside momentum. Price is holding below the 50-day SMA at 1.1686 and the 100-day SMA at 1.1665, reinforcing a near-term bearish tone. The 1.1600 area remains a key pivot, with a break below opening scope toward the 1.1578 session low and then 1.1490. A recovery would require a move back above 1.1665 to stabilise sentiment toward 1.1700.

- GBP/USD Extends Declines After Key Break: GBP/USD fell 0.61% to 1.3191 after trading between 1.3281 and 1.3140. The pair has now closed decisively below the 200-day SMA at 1.3241, marking a meaningful shift in longer-term tone. The 50-day and 100-day SMAs at 1.3446 and 1.3473 remain well above, keeping the broader bias pointed lower. Immediate resistance is set at 1.3241, followed by 1.3281. Support lies first at 1.3140, with the 1.3000 psychological level coming into focus if downside pressure persists.

- USD/JPY Holds Firm Near Recent Highs: USD/JPY closed at 152.83, up 0.49%, after reaching a high of 153.06 and a low of 151.53. The pair continues to trade above rising 50-day, 100-day and 200-day SMAs (149.19, 147.91 and 147.75), maintaining a solid bullish backdrop. The immediate focus is the resistance cluster around 153.06–153.20, a zone that has capped upside attempts recently. Initial support is located at 151.53, followed by 150.50. A sustained hold above 152.80 increases the likelihood of a breakout toward new highs.

- USD/CHF Strengthens Through Key Levels: USD/CHF rose 0.97% to 0.8006, after ranging between 0.8020 and 0.7925. The move pushed price back above the 50-day SMA at 0.7975 and the 100-day SMA at 0.8004, shifting short-term momentum back in favour of buyers. The longer-term 200-day SMA at 0.8307 remains above price, meaning broader trend repair is still ongoing. Immediate resistance stands at 0.8020, followed by 0.8060. Initial support is located at 0.8004 and 0.7975, with a break below signalling fading upside momentum.

- Gold Consolidates Below the $4,000 Pivot: Gold closed at $3,946, down 0.17%, after moving between $4,030 and $3,915. The metal continues to consolidate following recent highs, but remains supported by rising 50-day, 100-day and 200-day SMAs ($3,792, $3,570 and $3,319). The $4,000 level remains a key psychological barrier, with overhead resistance at $4,030 and higher near $4,060. Support is seen at $3,915 and $3,850. A sustained hold above $3,915 would keep consolidation constructive, while a break lower may pullback toward the 50-day SMA.

- Silver Rebounds to Resume Upward Momentum: Silver closed at $47.66, up 1.32%, after ranging between $48.45 and $46.84. The recovery aligns with upward-sloping 50-day, 100-day, and 200-day SMAs ($44.93, $41.13, and $36.80), reinforcing bullish structure. Immediate resistance sits at $48.45, followed by the key swing high near $54.00. Support lies at $46.84 and then $45.50, with demand continuing to emerge on dips.

Market Movers:

- Teradyne Rises on Strong Revenue: Teradyne shares closed up over 20% after reporting better-than-consensus Q3 net revenue and forecasting Q4 revenue significantly above expectations.

- Fiserv Plummets on Reduced Full-Year Guidance: Fiserv shares plunged over 44% after the company cut its full-year adjusted EPS estimate significantly.

- Seagate Technology Holdings Posts Earnings Beat: Seagate Technology Holdings Plc gained over 19% following Q1 adjusted EPS that exceeded consensus and a Q2 adjusted EPS forecast midpoint above analyst estimates.

- Bloom Energy Surges on Robust Q3 Earnings: Bloom Energy shares climbed over 16% after reporting Q3 adjusted EPS of 15 cents, which was stronger than the consensus of 7.9 cents.

- Deutsche Bank Reports Stronger-Than-Expected Profit: Deutsche Bank shares gained almost 5% after it reported better-than-expected net profit of 1.56 billion euros in the third quarter.

- Avantor Declines on Missed Q3 Sales Expectations: Avantor shares fell over 23% after reporting Q3 net sales of $1.62 billion, which was below the consensus estimate.

- Smurfit WestRock Shares Fall on Weaker Q3: Smurfit WestRock Plc saw its shares decline over 12% after reporting Q3 adjusted Ebitda of $1.30 billion, weaker than the consensus.

- Adidas Shares Decline Following Preliminary Results Confirmation: Adidas shares were down more than 10% following the confirmation of its preliminary results for the period.

Wednesday’s trading session was largely defined by the Federal Reserve’s latest monetary policy announcement and Chair Powell’s cautious remarks on future rate cuts, which introduced uncertainty into market expectations. Global markets reflected this mixed sentiment, with European indices generally lower and Asian markets showing varied performances. Looking ahead, investors will continue to monitor corporate earnings reports for insights into economic health, while remaining attuned to any further guidance from central banks and developments in international trade relations, particularly between the US and China, which could influence market direction.