Equities pushed higher as investors rotated back into technology leaders, with enthusiasm around artificial intelligence demand helping offset uncertainty surrounding the Federal Reserve’s next policy move. Strength in heavyweight chipmakers and select mega-cap names underpinned the advance, even as traders digested cautious signals from the latest Fed minutes and remained alert to geopolitical risks influencing energy markets. The session reflected a market that is becoming more selective, rewarding earnings visibility and structural growth themes while remaining sensitive to shifts in monetary policy expectations.

Key Takeaways:

- S&P 500 Gains on Technology Strength: The S&P 500 climbed 38.31 points, or 0.56%, to finish at 6,881.31, buoyed by a recovery in high-growth technology stocks. Gains were led by Nvidia and Amazon, which helped the index overcome investor anxiety following the release of Federal Reserve minutes that highlighted internal debate over the future of interest rates.

- Nasdaq Composite Outperforms Amid AI Optimism: The Nasdaq Composite added 176.12 points, or 0.78%, to close at 22,753.63, outperforming the broader market as artificial intelligence optimism regained momentum. Strength in the semiconductor sector, particularly Micron Technology, provided a significant tailwind despite ongoing concerns about the potential for AI-driven disruption in the software industry.

- Dow Jones Industrial Average Edges Higher: The Dow Jones Industrial Average rose 129.47 points, or 0.26%, to settle at 49,662.66, lagging its peers as investors adopted a more discerning approach to cyclical names. While the blue-chip index benefited from the general risk-on sentiment, gains were tempered by a cautious outlook on monetary policy and mixed performance across industrial components.

- European Markets Rally as Inflation Data Reinforces Rate Cut Expectations: European equities closed firmly higher, with the STOXX 600 rising 1.2% as most sectors ended in positive territory. The FTSE 100 jumped 1.28% to 10,691, while the CAC 40 gained 0.81% to 8,429 and Italy’s FTSE MIB advanced 1.30% to 46,361. Germany’s DAX rose 1.12% to 25,278 and Switzerland’s SMI added 0.39% to 13,807. UK inflation eased to 3.0% in January from 3.4% in December, the lowest reading in ten months, strengthening expectations for a Bank of England rate cut. Core UK inflation softened slightly to 3.1%. In France, headline inflation slowed sharply to 0.3%, the weakest since December 2020, with harmonised inflation at 0.4%, reinforcing the disinflationary trend across the region.

- Asia Markets Mixed but Resilient Despite AI Concerns: Asian equities mostly moved higher despite lingering uncertainty around the long-term implications of artificial intelligence investment. Japan’s Nikkei 225 rose 0.93% to 57,090.14, poised to snap a three-day losing streak, while several regional markets including China, Hong Kong, South Korea, Taiwan, and Singapore were closed for Lunar New Year holidays. In Australia, the S&P/ASX 200 gained 0.5% to 9,007, lifted by a near 4% surge in National Australia Bank after a 16% rise in quarterly cash earnings. New Zealand’s benchmark climbed 0.8% to 13,132 as investors looked ahead to the RBNZ policy meeting. In India, the Sensex rose 0.34% to 83,734.25 and the Nifty 50 added 0.37% to 25,819.35, led by financials and metals, while IT shares lagged amid persistent AI-related uncertainty.

- Oil Jumps Sharply on Escalating US-Iran Tensions: Oil prices surged more than 4% after US Vice President JD Vance said Iran failed to address key US demands during nuclear talks and that military action remained on the table. US crude settled at $65.19 per barrel, up 4.59%, while Brent crude climbed 4.35% to $70.35. The sharp rebound reversed losses from the previous session, when comments from Iran’s foreign minister had raised hopes of a potential diplomatic breakthrough.

- Treasury Yields Rise as Fed Minutes Highlight Policy Division: US Treasury yields moved higher after minutes from the Federal Reserve’s January meeting revealed disagreement over the next steps for monetary policy. The 10-year yield rose more than 3 basis points to 4.087%, while the 30-year yield climbed above 4.711%. The 2-year yield also edged more than 3 basis points higher to 3.468%. Policymakers broadly agreed on holding rates steady at 3.5% to 3.75%, but debate intensified over whether future decisions should prioritise inflation risks or labour market conditions.

- US Data Shows Mixed Growth Signals: US durable goods orders fell 1.4% in December, a smaller decline than expected, following a revised 5.4% surge in November, with weakness concentrated in transport equipment. In contrast, industrial production rose 0.7% in January, the strongest increase since February, while manufacturing output climbed 0.6%, both exceeding forecasts. Housing starts also surprised to the upside, rising 6.2% in December to an annualised rate of 1.404 million, marking a second consecutive monthly increase and the highest level since July.

FX Today:

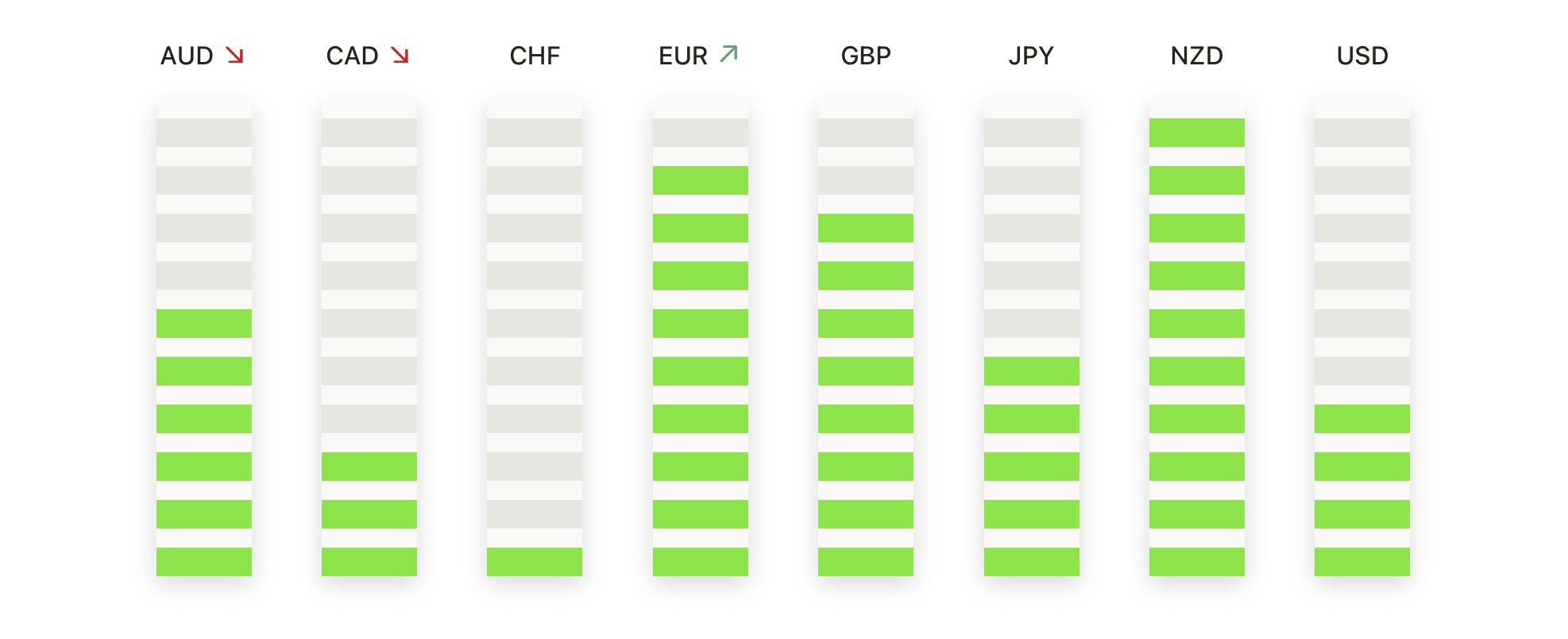

- EUR/USD Extends Losses as Downside Momentum Builds: EUR/USD closed at 1.1784, down 0.60%, after trading between a high of 1.1858 and a low of 1.1782. The pair remained under sustained selling pressure, slipping below the 50-day moving average at 1.1767 while still holding above the 100-day at 1.1688 and the 200-day at 1.1642. Price action has produced a sequence of lower highs since the early-February peak, confirming a corrective phase is in play. The short-term bias has turned bearish, even as the longer-term trend remains supported by the rising 200-day average. Immediate resistance is seen at 1.1858 and then the 1.1900 area. Support rests at 1.1782, with a more critical floor near the 200-day moving average.

- GBP/USD Slides After Breaking Below 50-Day Average: GBP/USD settled at 1.3499, down 0.50%, with the session ranging between 1.3582 and 1.3495. A firm bearish candle pushed the pair beneath the 50-day moving average at 1.3522, signalling growing downside momentum following the recent peak. Despite the decline, price continues to trade above the 200-day average at 1.3442 and the 100-day at 1.3393, which are acting as nearby supports. The short-term structure now reflects lower highs, pointing to a more cautious outlook. Resistance is located at 1.3522 and 1.3582. Support is initially at 1.3495, followed by the 200-day moving average.

- USD/JPY Rebounds Sharply Toward Key Resistance: USD/JPY finished at 154.80, up 1.01%, following a strong rebound from the 153.07 low to a session high of 154.87. The move saw the pair reclaim the 100-day moving average at 154.68, while remaining comfortably above the 200-day at 150.57. Price is now approaching the 50-day average at 156.00, a key resistance level that has capped recent upside attempts. The broader trend remains constructive, with higher lows still intact despite recent volatility. Immediate resistance is located at 154.87 and the 50-day average. Support sits at 154.68, followed by 153.07.

- Gold Rebounds Strongly to Reassert Bullish Bias: Gold closed at $4985, up 2.18%, after trading between $4854 and $5011. The strong bullish session reversed recent weakness, keeping price firmly above the 50-day moving average at $4648, as well as the 100-day and 200-day averages at $4353 and $3872. The broader structure of higher highs and higher lows remains intact, reinforcing the dominant uptrend. Momentum has turned decisively higher, with buyers once again targeting record levels. Immediate resistance is located at $5011. Support is seen at $4854, with stronger backing near the 50-day average.

- Silver Surges as Buyers Regain Control: Silver settled at $77.33, up 5.21%, after a volatile session that ranged from $72.33 to $78.33. The powerful advance followed a sharp correction, with price holding well above the 100-day moving average at $65.05 and the 200-day at $51.13. Silver remains just below the 50-day moving average at $79.80, which now stands as a key upside hurdle. The broader trend remains firmly bullish, underpinned by a pattern of higher highs and higher lows since late 2025. Resistance is defined by $78.33 and $79.80. Initial support rests at $72.33.

Market Movers:

- Global Payments Jumps on Strong Earnings Outlook: Shares surged more than 16% after the company forecast full-year adjusted EPS, including SBC, of $13.80 to $14.00, comfortably above the consensus estimate of $13.59.

- Global-e Online Rallies After Upbeat Revenue Guidance: The stock climbed over 16% after issuing full-year revenue guidance of $1.21 billion to $1.27 billion.

- Palo Alto Networks Slides on Weaker Guidance: The stock fell more than 6% after forecasting full-year adjusted EPS of $3.65 to $3.70, below the consensus estimate of $3.87, weighing on sentiment across the cybersecurity sector.

- Applied Digital Falls After Nvidia Exit: Shares declined over 4% after Nvidia disclosed it had exited its equity investment in the company, pressuring confidence in the firm’s near-term growth outlook.

Markets ended the session with a firmer tone as leadership from AI-focused companies reinforced confidence in selective growth themes. Cooling inflation across Europe strengthened the case for eventual policy easing, while Asian equities found support despite ongoing debate around the sustainability of AI investment. Rising bond yields and a sharp move higher in oil prices underscored the delicate balance between growth optimism and macro uncertainty, leaving investors closely attuned to upcoming policy signals and geopolitical developments.