Markets ended mixed on Friday as renewed tariff headlines weighed on sentiment despite a solid week for earnings and economic data. The Dow declined over 140 points following reports that President Trump is pushing for new tariffs on EU imports, reigniting trade tensions. The S&P 500 briefly touched a record high before finishing flat, while the Nasdaq posted a modest gain, supported by strength in tech. Investors assessed a wave of corporate results and encouraging consumer sentiment figures alongside concerns over global trade. Both the S&P 500 and Nasdaq posted weekly gains, while the Dow ended marginally lower.

Key Takeaways:

- Dow Falls on Tariff Escalation and Earnings Drag: The Dow Jones Industrial Average declined 142.30 points, or 0.32%, to close at 44,342.19, as investors reacted to a report that President Trump is demanding a minimum 15% tariff on European imports. Dow constituents American Express and 3M weighed on the index, falling 2% and over 3%, respectively.

- S&P 500 Holds Near Record Despite Earnings Rotation: The S&P 500 edged down 0.01% to 6,296.79 after touching a fresh intraday all-time high earlier in the session. With 12% of companies having reported, 83% have beaten expectations.

- Nasdaq Edges Higher as Tech Rally Extends: The Nasdaq Composite rose 0.05% to finish at 20,895.66, securing a weekly gain of 1.5% and logging its tenth record close of the year. Broader optimism around mega-cap earnings and a strong showing from chip and crypto-linked stocks helped offset isolated weakness. Coinbase and Robinhood both rose, aided by rising ether prices following landmark crypto legislation.

- European Markets Slip Despite Strong Results: European indices ended mixed on Friday as earnings strength was overshadowed by renewed trade tensions with the US. The Stoxx 600 dipped 0.04%, weighed down by healthcare and tech, while oil and gas stocks outperformed. Germany’s DAX slipped 0.3% to 24,290 after giving up early gains, pressured by weak housing data and uncertainty over tariff talks. The FTSE MIB added 0.4%, and France’s CAC 40 edged higher to 7,823, supported by gains in financials and industrials. The FTSE 100 rose 0.57% for the week to 8,992.12. German producer prices dropped 1.3% annually, matching forecasts, but a 5.3% fall in apartment building permits for May revived concerns about structural weakness in the property sector.

- Asia Mixed as Japan Inflation Cools and Australia Hits Record: Asian equities delivered a mixed performance. Australia’s ASX 200 surged 1.37% to a record close of 8,757.2, boosted by commodity names and positive global sentiment. Japan’s Nikkei 225 slipped 0.21% to 39,819.11 as core inflation slowed to 3.3% in June, easing from May’s 3.7%. The Topix fell 0.19%. Mainland China’s CSI 300 rose 0.6% to 4,058.55, while Hong Kong’s jobless rate remained at a two-year high of 3.5%. South Korea’s Kospi fell 0.13%, while the Kosdaq added 0.29%. Officials from South Korea and India met to deepen steel sector cooperation, signalling potential trade expansion across Asia.

- Oil Flat as EU Sanctions and US Data Offset Each Other: Crude prices were little changed on Friday, with Brent down 0.3% to $69.32 and WTI off 0.2% at $67.41. Both contracts were on track to lose around 1% for the week. Traders weighed the impact of fresh EU sanctions on Russia, which could disrupt global supply, against mixed economic signals from the US. Chevron completed its $55 billion Hess acquisition after prevailing in a key legal dispute with Exxon over Guyana’s offshore assets.

- US Sentiment Improves but Housing Data Disappoints: US consumer confidence improved in July, with the University of Michigan’s sentiment index rising to 61.8, its highest since February, amid reduced concern about inflation and tariffs. One-year inflation expectations fell to 4.4% and the five-year outlook dropped to 3.6%. However, the housing market offered a stark contrast, with single-family home starts dropping 4.6% in June to an 11-month low of 883,000 units. Building permits also fell 3.7% to a 15-month low, pointing to a broader cooling in residential activity amid elevated mortgage rates and ongoing affordability constraints.

- Treasury Yields Ease on Data and Trade Risks: US Treasury yields fell as investors digested economic updates and the rising risk of a transatlantic trade war. The 10-year yield dipped 4 basis points to 4.423%, while the 2-year yield slid to 3.87%. The 30-year note eased to 4.99%. Cooling inflation expectations and softer housing starts helped cap yields.

FX Today:

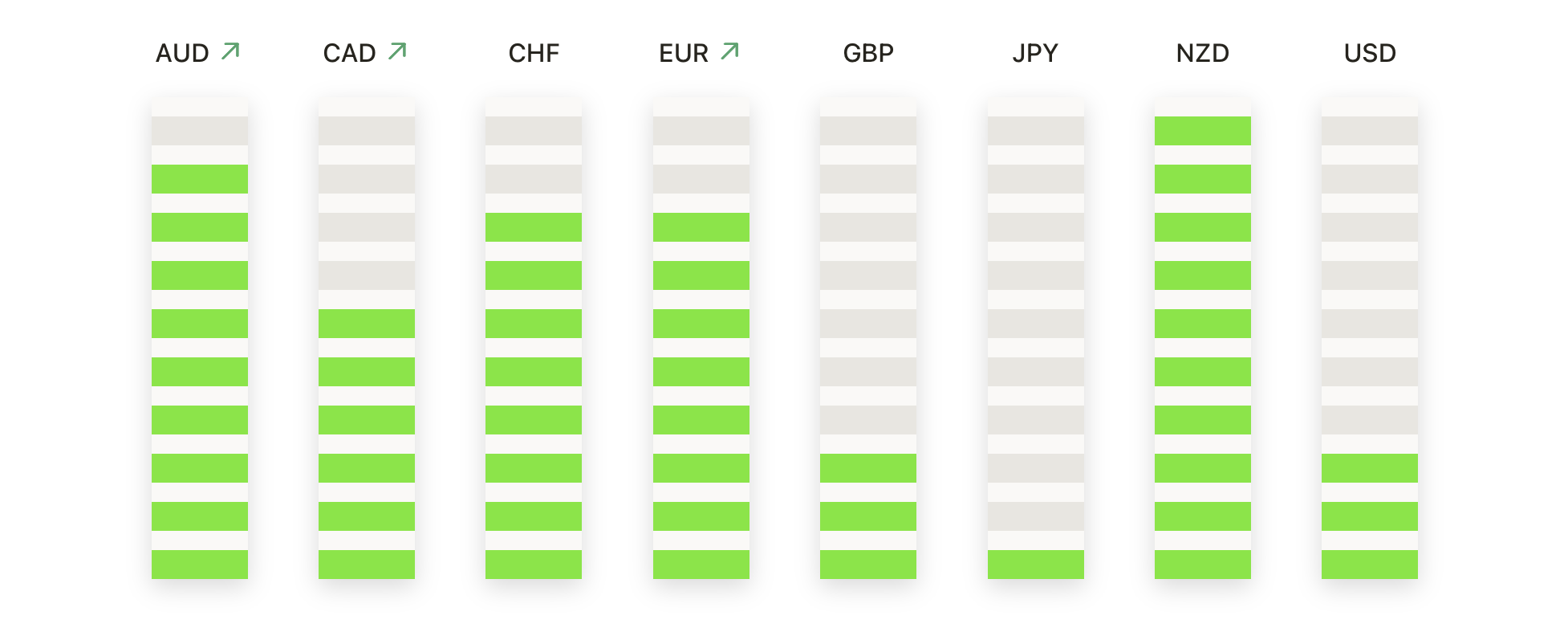

- EUR/USD Holds Ground as Buyers Defend Key Support Near 1.1600: The euro regained composure on Friday, with EUR/USD rising to settle at 1.1624 after bouncing from a low of 1.1595. The pair snapped a four-session losing streak, underpinned by renewed buying near the 1.1600 handle. Price action suggests solid demand just above the 50-day SMA at 1.1499, reinforcing a broader bullish structure that remains intact above the 100-day and 200-day moving averages. Despite the recent decline from 1.1850, the overall trend shows no sign of a breakdown. A decisive close above 1.1700 would reassert upside momentum, while a drop below 1.1490 could open the path toward 1.1400.

- GBP/USD Under Pressure as Price Slips Below Technical Support: Sterling lost ground for a second straight week, with GBP/USD closing at 1.3415 after failing to reclaim the 1.3480 region. The pair ended the day beneath its 50-day SMA at 1.3508, a level that has capped gains throughout the week. Price structure has weakened since the early July high near 1.3840, with intraday rallies consistently sold into. Momentum indicators are drifting lower, and the absence of bullish follow-through points to mounting downside risk. Immediate support sits near 1.3400, followed by the 100-day SMA at 1.3291. A break below this zone would expose 1.3200.

- USD/JPY Struggles to Extend Gains Near Long-Term Resistance: The dollar edged higher against the yen, closing at 148.71, but failed once again to break through the key 200-day SMA resistance at 149.60. While the pair has now advanced for nine consecutive sessions, Friday’s narrow candle suggests fatigue near this critical level. However, the inability to clear the 149.60 barrier raises the risk of a corrective pullback. Initial support is seen near 147.80, followed by the 100-day SMA at 145.75. A daily close above 149.60 would resume the upward push and target 151.00–152.00, but for now, consolidation appears likely.

- USD/CAD Reverses Lower After Failing to Clear 1.3750 Barrier: The Canadian dollar firmed slightly against its US counterpart on Friday, with USD/CAD falling to 1.3729 after failing to sustain early strength. The pair briefly breached the 50-day SMA at 1.3731 but was swiftly rejected, forming a bearish reversal candle. This marks the third time in recent weeks that the 1.3750 region has halted rallies, reinforcing it as a significant resistance zone. With the broader trend still pointing lower, pressure remains on the downside unless buyers can produce a clean break above 1.3780. Key support lies at 1.3650, followed by 1.3600.

- Gold Drifts Sideways as Traders Await Directional Breakout: Gold closed higher on Friday, settling at $3,348, but remained locked within a tight trading band between $3,332 and $3,361. The metal continues to consolidate above the 50-day SMA at $3,324, but buying momentum has stalled, with resistance near $3,365 proving stubborn. The overall trend remains positive while price holds above the 100-day average at $3,214, but flat momentum readings suggest neither bulls nor bears have control. A decisive move above $3,370 is needed to trigger a fresh leg higher toward the $3,420 area. Conversely, a drop below $3,300 could tilt the balance toward sellers and spark a move back to the $3,200 zone.

Market Movers:

- Talen Energy Jumps on $3.5 Billion Power Deal: Shares soared over 24% after Talen announced plans to acquire two large gas-fired power plants in Pennsylvania and Ohio. The deal, valued at $3.5 billion including tax benefits, expands its energy portfolio.

- Invesco Rallies as QQQ Structure Set to Change: Invesco rose 15% after reports said it is seeking approval to convert its flagship QQQ ETF into an open-ended fund. The shift would boost fee income and reduce costs for investors. QQQ has gained nearly 10% this year.

- Netflix Slides on Margin Warning Despite Earnings Beat: Netflix fell 5% after forecasting lower operating margins in H2 due to higher content and marketing costs. The company topped revenue and EPS estimates but investors focused on the cautious guidance.

- Sarepta Therapeutics Crashes on Trial Fatality: Shares plunged nearly 36% after a patient died during a Phase 1 study. Reports cited acute liver toxicity as the cause. The incident raised concerns about safety and regulatory risk for its pipeline.

- American Express Drops After Earnings Reaction: American Express fell 2% despite beating second-quarter estimates on both revenue and profit. Investors appeared cautious about forward guidance. The Dow component weighed on the broader index.

- Crypto Stocks Rise on Ether Breakout and Legislation: Coinbase, Robinhood, and Galaxy Digital all advanced after ether hit a six-month high. The gains followed the passage of landmark US crypto regulation. Bitmine Immersion also climbed modestly.

Markets ended the week with a mixed tone as trade tensions re-emerged, weighing on sentiment despite broadly positive earnings and macro data. While the Dow slipped on tariff headlines and earnings disappointments, the S&P 500 and Nasdaq held firm, supported by strength in tech and a rebound in consumer confidence. European and Asian markets were largely steady, though concerns over trade and inflation continued to influence direction. Investors now turn their focus to upcoming earnings from major US tech names and the evolving US-EU tariff negotiations ahead of the 1 August deadline.