Wall Street wrapped up a strong May with a muted session on Friday, as investors digested fresh trade tensions and mixed economic signals. Markets wavered early after President Trump accused China of violating its trade agreement and reports surfaced of new restrictions targeting Chinese technology. Adding to the uncertainty, the administration announced a doubling of tariffs on steel imports, drawing criticism from European officials. Despite the unsettled backdrop, equities steadied into the close, with the S&P 500 ending flat while still posting a 6.2% monthly gain, its best since November 2023. Investors now turn their attention to upcoming data and policy events that could shape the path ahead.

Key Takeaways:

- Dow Edges Higher to Cap a Strong May: The Dow Jones Industrial Average added 54.34 points, or 0.13%, to finish at 42,270.07. The index gained 1.6% for the week and rose 3.9% in May, posting its best monthly gain since November 2023.

- S&P 500 Ends Flat After 6% Monthly Surge: The S&P 500 inched down by just 0.01% to close at 5,911.69 on Friday. Despite the muted session, the benchmark index locked in a 6.2% gain for May and advanced 1.9% on the week.

- Nasdaq Slides as Tech Faces Trade Headwinds: The Nasdaq Composite fell 0.32% to 19,113.77. The index still gained 2% this week and surged 9.6% for May. Investors showed caution after reports of planned US restrictions on Chinese technology and legal uncertainty surrounding reciprocal tariffs.

- Europe Closes Mixed as Steel Tariff Hike Stokes Trade Tensions: European equities ended mixed Friday, with the Stoxx 600 eking out a 0.1% gain after two days of losses. Germany’s DAX rose 0.31% to 23,997.48 as May inflation held steady at 2.1%, near the ECB’s target, though retail sales disappointed. The FTSE 100 climbed 3.27% this month to 8,772.38, supported by easing UK inflation and firm consumer demand. France’s CAC 40 slipped 0.36%, marking its fourth consecutive daily decline amid concerns over global trade. Spain’s inflation cooled to 1.9%, while Sweden’s Q1 GDP contracted, adding pressure for potential rate cuts. The EU strongly criticised Washington’s decision to double steel tariffs, warning it would undermine efforts for a negotiated solution.

- Asia Stocks Decline on Tariff Jitters and Inflation Fears: Asia-Pacific markets broadly fell as a US appeals court reinstated reciprocal tariffs, reigniting trade worries. Japan’s Nikkei 225 dropped 1.22% after Tokyo’s core inflation hit a fresh 3.6%. The Topix edged lower by 0.37%. Hong Kong’s Hang Seng retreated 1.2%, while mainland China’s CSI 300 slid 0.48% amid signs that US-China trade talks remain stalled. South Korea’s Kospi lost 0.84%. India’s Sensex and Nifty slipped despite stronger-than-expected 7.4% GDP growth. Australia’s ASX 200 rose 0.3%, with gains tempered by a surprise dip in retail sales.

- PCE Inflation Softens as Consumer Sentiment Steadies: The core personal consumption expenditures (PCE) price index rose 2.1% annually in April, slightly below economists’ 2.2% forecast. Consumer spending grew 0.2%, down from 0.7% in March, as tariff concerns tempered demand. Meanwhile, the University of Michigan’s sentiment index held steady at 52.2 in May. The one-year inflation outlook eased to 6.6%, while the five-year view dipped to 4.2%, reflecting modestly improving consumer confidence.

- Treasury Yields Slip amid Trade and Inflation Signals: US 10-year Treasury yields declined 3 basis points to 4.394% as investors digested softer inflation data and heightened trade policy uncertainty. The 2-year yield eased to 3.897%, while the 30-year yield was little changed at 4.921%.

- Oil Drops as OPEC+ Eyes Output Boost: US crude futures fell 0.34% to $60.73 a barrel, while Brent settled at $63.93. Prices dipped on expectations that OPEC+ may approve a larger-than-expected July production increase at its upcoming meeting. Both benchmarks were on track for weekly declines exceeding 1%.

FX Today:

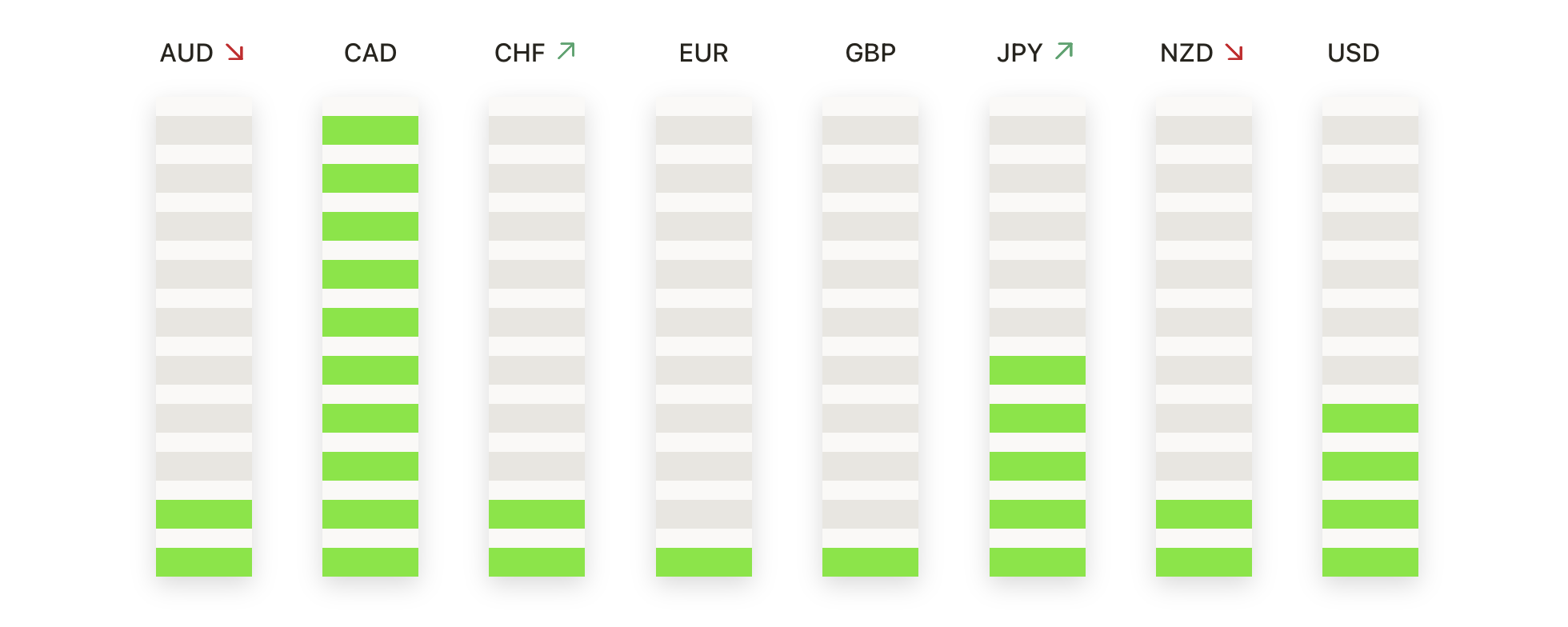

- EUR/USD Holds Below 1.1400 as Bulls Consolidate Gains: EUR/USD finished the week at 1.1346, easing 0.17% on Friday as the pair consolidated after a sharp April–May rally. The broader trend remains bullish with the pair holding above the 50-day SMA at 1.1194. Key resistance remains at the 1.1400 level, which capped gains over the past two weeks. Momentum indicators are flattening, pointing to short-term consolidation. Initial support lies near 1.1300, while deeper pullbacks could test the 50-day SMA. A sustained break above 1.1400 would target the April high near 1.1500.

- GBP/USD Stalls Near 1.3500 as Bulls Pause: GBP/USD closed Friday at 1.3457, slipping 0.26%, as the pair took a breather near multi-month highs. The uptrend remains intact above the 50-day SMA at 1.3217. Resistance at the 1.3500 psychological level continues to cap upside moves. Momentum has cooled, suggesting possible near-term consolidation. Support is seen near 1.3400 and at the rising 50-day SMA. A decisive close above 1.3500 would open the path toward 1.3600–1.3700 targets.

- USD/JPY Holds Near 144.00 as Bears Maintain Control: USD/JPY ended the week at 144.04, slipping 0.09% as downward momentum persisted. The pair remains below key resistance at the 50-day SMA of 145.20, with the broader trend still bearish. Sellers continue to defend levels above 145.00. Support is near 143.00, with a break lower targeting 141.50. Only a sustained move above the 50-day SMA would neutralise the current bearish tone.

- USD/CAD Slides Toward 1.3700 as Canadian Growth Surprises: USD/CAD closed the week at 1.3735, down 0.52% on Friday, extending its recent downtrend. Canada’s Q1 GDP grew 2.2% annualised, beating expectations and strengthening the Canadian dollar. The pair is now testing key support near 1.3700. Resistance is seen at 1.3800, followed by the 50-day SMA at 1.3966. The trend remains bearish while price holds below key moving averages.

- Gold Pulls Back From Highs but Remains in Uptrend: Gold settled at $2,657 on Friday, down 0.50% as traders booked profits after recent highs. The metal remains well supported above the 50-day SMA at $2,488. Immediate support is near $2,650, with stronger demand expected near $2,600. A breakout above recent highs at $2,685 would target the $2,700–$2,750 zone. The bullish structure remains intact unless the price closes below the 50-day SMA.

- Silver Retreats Toward $30.00 as Rally Cools: Silver closed at $30.28, falling 0.91% after testing multi-year highs this week. The metal remains in a bullish trend, supported above the 50-day SMA at $28.41. Immediate support is at $30.00, with potential for deeper pullbacks toward $29.00. A close back above $31.00 would signal a resumption of the uptrend. The medium-term outlook stays positive while silver holds above its key moving averages.

Market Movers:

- Costco Gains on Strong Earnings Beat: Costco shares rose over 3% after the wholesaler reported fiscal third-quarter earnings that topped estimates. Sales surged 8% year-on-year, driven by strong membership growth and resilient consumer demand.

- Ulta Beauty Soars on Raised Guidance: Ulta Beauty surged nearly 13% to a 52-week high after the company raised its annual profit forecast. Quarterly results beat expectations, supported by lower inventory losses and successful new product launches.

- Gap Plunges on Weak Sales Outlook: Gap sank 20% after forecasting flat current-quarter sales, missing analyst expectations for slight growth. The disappointing outlook overshadowed its first-quarter earnings and revenue beat.

- Elastic NV Slumps on Revenue Forecast Miss: Elastic NV dropped 12% after issuing full-year revenue guidance below analyst estimates. The company projected revenue between $1.655 billion and $1.67 billion, short of the $1.68 billion consensus.

- Marvell Technology Drops After Mixed Earnings: Marvell Technology fell 6% as first-quarter earnings failed to impress investors. Adjusted EPS came in at 62 cents, just above estimates, but guidance and demand commentary weighed on sentiment.

- Regeneron, Sanofi Slide on Drug Trial Results: Regeneron shares tumbled 18% while Sanofi fell 5.6% after mixed results from late-stage trials of their respiratory drug itepekimab.

- PagerDuty Sinks on Weak Guidance: PagerDuty fell 11% after the cloud firm issued a softer-than-expected second-quarter profit forecast. The company projected EPS of 19–20 cents, below the 23 cents expected by analysts.

- Zscaler Jumps on Earnings Beat: Zscaler climbed 8% after posting stronger-than-expected third-quarter results. The company reported adjusted EPS of 84 cents on $678 million in revenue, beating analyst forecasts on both top and bottom lines.

- Palantir Advances on Government Contract Report: Palantir Technologies gained more than 5% following a New York Times report that the Trump administration tapped the company to assist in compiling citizen data, expanding its government partnerships.

With May’s rally complete, markets now face a complex backdrop of trade policy uncertainty and shifting economic signals. Easing inflation data and solid earnings have helped support sentiment, but renewed tariff tensions with China and the European Union introduce fresh risks. Investors will monitor legal proceedings related to US tariffs and key outcomes from the OPEC+ meeting. The coming weeks are likely to remain data-driven, with inflation trends, central bank decisions, and geopolitical events shaping market direction.