US equities pulled back on Tuesday as caution returned to markets following softer services sector data and fresh tariff threats from President Donald Trump. Investors weighed signs of slowing economic momentum against a strong start to the week, with technology and industrial stocks under particular pressure. Sentiment weakened further after Trump signalled plans to introduce new duties on semiconductors and pharmaceuticals within days, a move that rattled global chipmakers. While a handful of corporate results offered support, broader gains were capped as traders reassessed the economic outlook.

Key Takeaways:

- Dow Slips After Strong Start to Week: The Dow Jones Industrial Average eased 61.90 points, or 0.14%, to close at 44,111.74, giving back part of Monday’s sharp rebound. Caution returned after Trump’s comments on impending tariffs and the release of weaker US services data. The pullback came just days after Friday’s steep drop, as investors continued to weigh signs of slowing growth against expectations for easier monetary policy.

- S&P 500 and Nasdaq Weaken on Tariff Concerns: The S&P 500 lost 0.49% to finish at 6,299.19, while the Nasdaq Composite fell 0.65% to 20,916.55. Technology shares were among the hardest hit, with chipmakers retreating after Trump signalled plans to target semiconductors and pharmaceuticals with new import duties.

- ISM Services Index Stalls in July: US services activity flatlined last month, with the ISM non-manufacturing PMI slipping to 50.1 from 50.8 in June, missing expectations for an increase. Employment in the sector contracted further, while prices paid jumped at the fastest pace in nearly three years. The soft reading added to recent data showing weakening job growth.

- European Markets Edge Higher but Chip Stocks Sink: The Stoxx Europe 600 added 0.1% as gains in London and Frankfurt offset modest declines in Paris. The FTSE 100 rose 0.16% to 9,142.73, buoyed by financials, while the DAX gained 0.4% to 23,857.2. The CAC 40 slipped 0.1% to 7,635, giving back some of Monday’s rebound. Semiconductor stocks reversed early gains after Trump’s tariff remarks, with BE Semiconductor falling 2.3% and VAT Group and STMicro both down 0.9%. Investors also digested mixed macro data, including France’s services PMI falling to 48.5, signalling a faster pace of contraction, while Eurozone PMI was revised slightly lower and UK PMI revised higher.

- Asia Markets Rally on Rate Cut Bets Despite India Tariff Threats: Asian equities advanced broadly, led by South Korea’s KOSPI, which surged 1.6% for its biggest rise in nearly a month, and Vietnam’s VNINDEX, which jumped almost 3% to a record high. Taiwan, Jakarta, and Bangkok also gained more than 1%, while Japan’s Nikkei rose 0.64% and the Topix climbed 0.7%. The Hang Seng added 0.7% after data showed China’s services activity growing at its fastest pace in 14 months. Gains came despite Trump’s warning of higher tariffs on Indian goods, which weighed on the Sensex and Nifty 50. Expectations for a September Fed rate cut rose sharply, helping sustain risk appetite across the region.

- Oil Falls on OPEC+ Output Hike: Brent crude slid 1.63% to settle at $67.64 a barrel, while WTI dropped 1.7% to $65.16. The declines came as OPEC+ agreed to raise output by 547,000 barrels per day in September, ending recent cuts earlier than planned. Concerns over slowing demand and Trump’s tariff threats to India, the largest buyer of Russian seaborne crude, added to the downward pressure.

- Treasury Yields Hold Steady After Services Data: The 10-year Treasury yield was little changed at 4.20% as investors weighed softer ISM services data against a sharp rise in prices paid. The 2-year yield rose 3 basis points to 3.716%, while the 30-year yield dipped 2 basis points to 4.771%. The data showed new export orders and imports contracting, with employment in services falling further into negative territory.

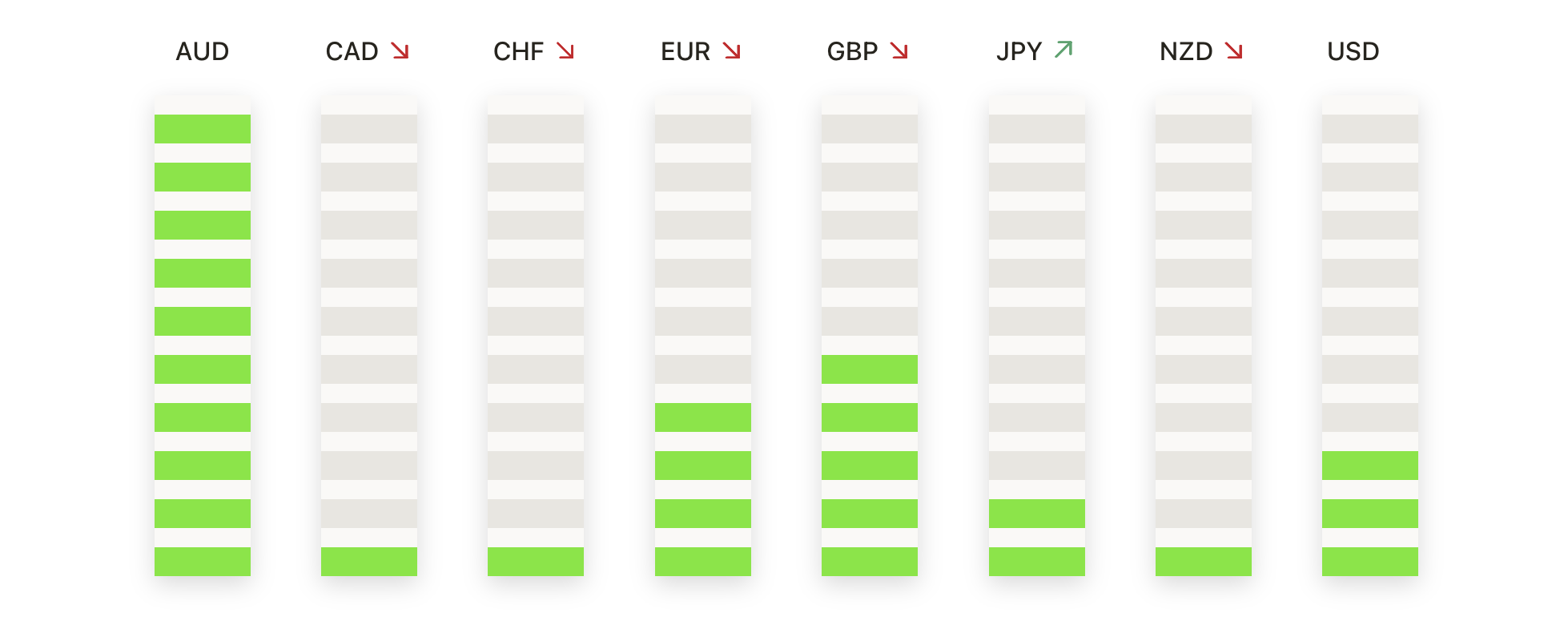

FX Today:

- EUR/USD Holds Below 1.1600 as Buyers Struggle to Extend Rebound: EUR/USD closed at 1.1575, up 0.02% after trading between 1.1572 and 1.1588, marking a calm session following last week’s sharp recovery from the 200-day SMA near 1.1377. The rebound has pushed price back above the 100-day SMA at 1.1424 and just over the 50-day SMA at 1.1587, yet the 1.1600 psychological level remains a firm barrier. Structurally, the market is now in the upper half of its recent range, but the narrow-bodied candle signals hesitation on direction. The broader tone is tentatively bullish while above 1.1500, though a clear daily close above 1.1620 is needed to target 1.1700 and the July high at 1.1740. First support lies at 1.1530, with stronger demand at 1.1470, where a break lower would risk a slide into the 1.1400–1.1420 area.

- GBP/USD Consolidates Near 1.3300 as Recovery Momentum Slows: GBP/USD closed at 1.3296, up 0.08% after ranging between 1.3288 and 1.3316, extending its bounce from last week’s low near 1.3100 but lacking follow-through ahead of key technical barriers. Price is holding below the 100-day SMA at 1.3348 and the declining 50-day SMA at 1.3508, keeping the medium-term tone cautious despite recent gains. The rally has lifted the pair into the lower half of July’s range, though resistance at 1.3350 continues to cap progress. A confirmed break above 1.3350 would expose 1.3450, the late-July lower high, while initial support is seen at 1.3240 and stronger demand at 1.3180. A daily close under 1.3180 would undermine the rebound and bring 1.3100 back into focus.

- USD/JPY Holds Above 147.50 as Bulls Defend Support After Pullback: USD/JPY closed at 147.61, up 0.36% after trading between 146.62 and 147.83, posting a bullish daily candle that lifted price from the lower end of the recent range. Buyers defended the 50-day SMA at 145.86 and the 100-day SMA at 145.67, maintaining a mild bullish bias while above the mid-145.00s. The 200-day SMA at 149.45 remains the key upside barrier, with a break required to re-establish sustained bullish momentum. Structurally, the pair is consolidating between 146.00 and 149.50, with immediate resistance at 148.00, then 149.00 and the 200-day SMA. First support is at 146.60, with a drop below 145.70 risking a deeper slide towards 144.50, while a close above 149.50 would put the July highs near 151.00 back in view.

- Gold Climbs Back Above $3,380 as Bulls Regain Control: Gold closed at $3,381, up 0.18% after trading between $3,350 and $3,390, marking a third straight daily gain from last week’s low just above $3,250. Price is back above the 50-day SMA at $3,344, with the 100-day SMA at $3,268 and 200-day SMA at $3,003 well below, confirming the broader bullish trend. The recovery has lifted the metal into the upper half of July’s range, with momentum targeting the $3,400 level that capped gains late last month. Immediate resistance is at $3,390, followed by $3,420, while support is at $3,355 and then $3,344. A close above $3,400 would open the door for a move towards the April high near $3,460, while failure to clear it could lead to renewed consolidation.

- Silver Advances Above $37.75 as Recovery Extends From Support: Silver closed at $37.79, up 1.06% after trading between $37.32 and $37.88. Price remains above the 100-day SMA at $34.66 and 200-day SMA at $33.00, keeping the broader bullish structure intact. The rally has returned the market to the upper half of the late-July range, with immediate resistance at $37.88 and then $38.40. Support lies at $37.50, with stronger demand at $37.00. A daily close above $38.00 would confirm renewed bullish momentum and open the way to retest the recent highs near $39.00, while slipping under $37.50 could trigger a move back into the mid-$36.00s.

Market Movers:

- Inspire Medical Systems Plunges on Weak Forecast: Shares fell over 34% after cutting full-year revenue guidance to $900–$910 million from $940–$955 million.

- Gartner Drops Sharply After Guidance Cut: The stock sank more than 27% as the company lowered its full-year revenue forecast to $6.46 billion, missing the $6.57 billion consensus.

- GlobalFoundries Leads Semiconductor Declines: Shares dropped more than 9% after forecasting Q3 EPS below expectations, dragging down chipmakers including KLA, ARM, and AMD.

- Fidelity National Information Weakens on Outlook: The stock lost more than 8% after Q3 EPS guidance of $1.46–$1.50 fell short of consensus forecasts.

- Henry Schein Drops After Earnings Miss: Shares fell over 7% after reporting Q2 EPS of $1.10, missing the $1.19 consensus.

- Eaton Tumbles on Soft Revenue Guidance: The stock fell more than 7% after forecasting organic revenue growth of 8.50%–9.50%, with the midpoint below expectations.

- Axon Enterprise Jumps on Strong Results: Shares surged more than 16% after Q2 sales topped estimates and full-year EBITDA guidance was raised.

- Palantir Advances on Record Revenue: The stock gained over 7% after Q2 revenue exceeded $1 billion for the first time, prompting a higher full-year sales forecast.

- Leidos Holdings Climbs on Earnings Beat: Shares rose more than 7% after Q2 revenue beat forecasts and the company raised its full-year guidance.

Wall Street’s rally paused on Tuesday as weaker US services data and renewed tariff threats prompted a more cautious tone across global markets. While optimism over potential rate cuts and selected corporate beats provided some support, the latest macro readings underlined the fragility of economic momentum. European indices managed modest gains despite pressure on semiconductor stocks, and Asian markets advanced on rate cut expectations even as India faced fresh US trade tensions. With earnings season continuing and key trade announcements looming, investors appear set for a period of consolidation as they balance growth risks against the prospect of looser policy.