US equities closed lower on Thursday for a third straight session as rising Treasury yields and a pullback in major technology names weighed on sentiment. Oracle was again under pressure during regular trading, extending a steep multi-day decline, but the stock rebounded more than 1% after hours following confirmation that it will play a central role in the newly approved $14 billion TikTok US venture. President Trump signed an executive order backing the deal, with Oracle, Silver Lake and Abu Dhabi’s MGX fund set to take a controlling stake, giving the software giant a renewed boost despite lingering concerns over stretched valuations.

Key Takeaways:

- Dow Retreats as Selling Persists: The Dow Jones Industrial Average slipped 173.96 points, or 0.38%, to 45,947.32, weighed down by weakness in Tesla and Oracle. The index recorded its third straight day of losses.

- S&P 500 Slides on Tech Weakness: The S&P 500 fell 0.50% to 6,604.72, with declines in chipmakers and cloud names dragging the benchmark lower.

- Nasdaq Extends Decline: The Nasdaq Composite settled 0.50% lower at 22,384.70 as technology stocks broadly sold off. Tesla dropped 4%, while chipmakers including Micron and Nvidia also closed in the red.

- European Stocks Close Broadly Lower: The Stoxx 600 ended down 0.71% with all major indices negative. London’s FTSE 100 lost 36.45 points, or 0.39%, to 9,213.98, while the CAC 40 fell 48 points, or 0.62%. Germany’s DAX slid 0.6% to 23,521, and Italy’s FTSE MIB retreated 0.4% to 42,242. Luxury shares came under pressure after short-seller allegations against Brunello Cucinelli, which plunged nearly 20% before trading was halted. Medical technology firms also weighed after the US launched a national security probe into imports of devices and robotics, sending Siemens Healthineers down 3.5%, Philips 3% lower, and Convatec off 5.6%. In contrast, H&M surged 9.8% after posting stronger-than-expected quarterly earnings, leading gains in the retail sector. SAP shed 1.2% after the European Commission opened an antitrust investigation, while Petershill Partners surged over 33% after announcing plans to delist from London. Elsewhere, eurozone bank lending growth accelerated, while German sentiment data showed tentative signs of recovery.

- Asia-Pacific Markets Mixed, Japan Hits Record: Japan’s Nikkei 225 gained for a sixth straight day, closing at a record 45,754.93, while the Topix also touched fresh highs at 3,185.35. Elsewhere the picture was mixed: Hong Kong’s Hang Seng dipped 0.13% to 26,484.68 despite Chery’s debut, while Xiaomi rose 3.7% on product launches. China’s CSI 300 gained 0.6% to 4,593.49, South Korea’s Kospi finished flat at 3,471.1, and the Kosdaq lost 0.98%. Taiwan’s Taiex fell 0.66% as TSMC slipped 1.49% on reports Intel sought Apple investment, though a shift away from Intel chips makes such backing unlikely. Australia’s S&P/ASX 200 reversed early weakness to finish up 0.1% at 8,773, with resilience in resource stocks offsetting tech losses.

- US Jobless Claims Fall, GDP Revised Higher: Initial jobless claims came in at 218,000 for the week ended September 20, well below expectations for 235,000 and down from the prior week’s 232,000. The data pointed to ongoing labour market resilience despite a slowing pace of hiring. Meanwhile, US GDP for the second quarter was revised sharply higher to an annualised 3.8% from 3.3%, reflecting stronger consumer spending and investment in intellectual property.

- Oil Prices Edge Higher: Brent crude added 33 cents, or 0.48%, to $69.64 a barrel, while WTI climbed 29 cents, or 0.45%, to $65.28. The modest gains extended a rally from the prior session, when a surprise drop in US crude inventories and geopolitical risks lifted prices. Supply dynamics were in focus after Russia extended restrictions on fuel exports.

- Treasury Yields Rise on Data: The 10-year Treasury yield climbed to 4.172% after strong labour and GDP data. The 2-year yield rose over 6 basis points to 3.661%, while the 30-year was little changed at 4.749%. The resilience of the US economy has tempered expectations for near-term Fed easing, adding pressure to equities.

FX Today:

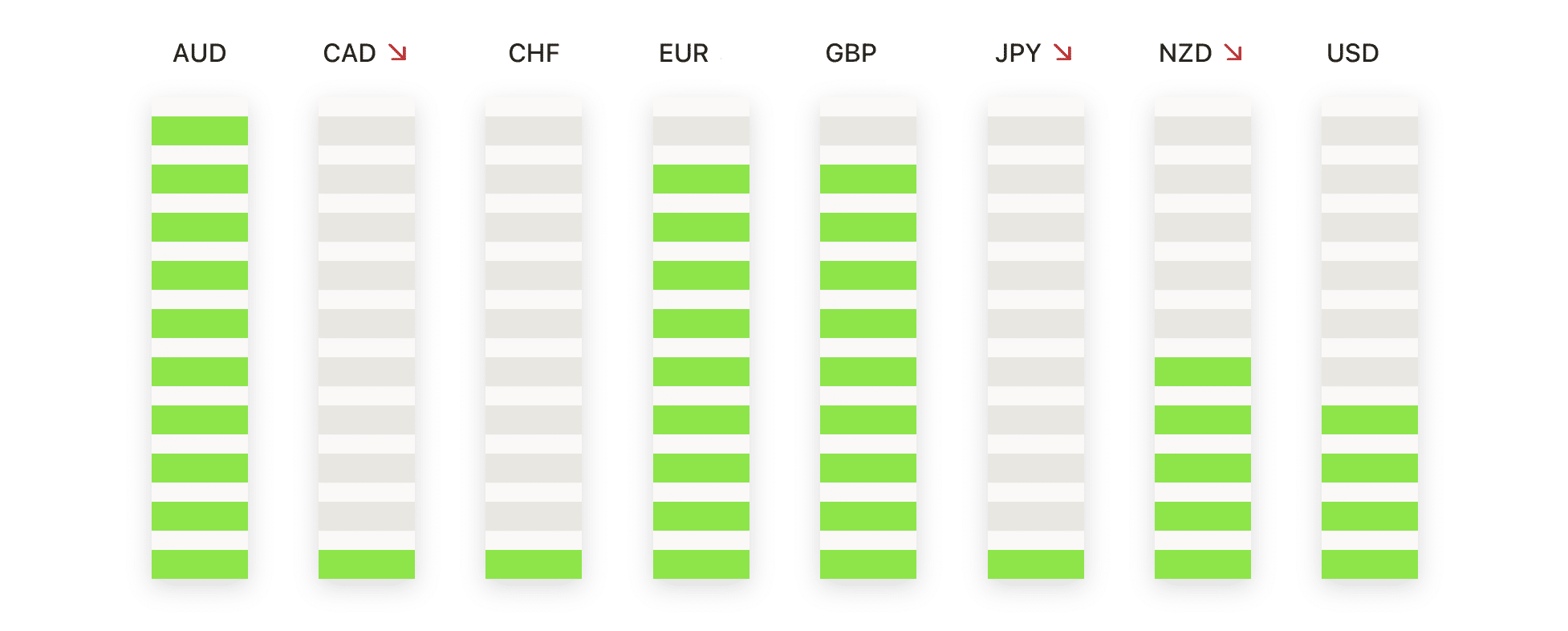

- EUR/USD Falls Back Towards Key Support: EUR/USD closed at 1.1661, down 0.66%, after trading between 1.1754 and 1.1661. The pair ended at the session low, underlining strong selling pressure as momentum shifted against the bulls following recent highs above 1.1850. Support came from the 50-day moving average at 1.1678, though the close beneath 1.1700 left the bias more defensive. The broader uptrend since May remains intact, helped by successive higher lows and the 100-day moving average at 1.1585, while the 200-day sits lower at 1.1151. Short-term sentiment, however, is tilted to the downside, with immediate support at 1.1650 and 1.1600, while resistance stands at 1.1720 and 1.1780.

- GBP/USD Extends Decline After Breaking 1.3400: GBP/USD settled at 1.3338, down 0.82%, after ranging between 1.3450 and 1.3333. The pair closed at the session low, marking a decisive break beneath the 1.3400 handle that had previously provided a base. The move lower reinforced the bearish shift, with price now holding well below the 50-day moving average at 1.3469 and the 100-day at 1.3487, which together form a new resistance zone. Although the broader trend since July had shown higher highs, repeated failures near 1.3700 and the latest selloff underline a weakening structure. The 200-day moving average at 1.3124 provides a longer-term reference point should pressure continue. Immediate resistance is now at 1.3400 and then 1.3480, while support lies at 1.3300, followed by 1.3250 and 1.3200.

- USD/JPY Tests 150.00 as Bulls Build Momentum: USD/JPY finished at 149.78, up 0.59%, after trading between 148.56 and 149.93. The pair closed near the top of the range, highlighting a strong bullish session driven by a break through the 200-day moving average at 148.48. This shift has put the psychological 150.00 level into focus, a threshold where heavy resistance is expected given repeated past failures. Both the 50-day at 147.71 and the 100-day at 146.41 now sit below, supporting the bullish tone and confirming momentum has turned in favour of buyers. Immediate support is at 149.00 and then 148.50, levels that coincide with former resistance

- AUD/USD Slides Back Towards 0.6500 Support: AUD/USD closed at 0.6537, down 0.69%, after trading between 0.6604 and 0.6526. The pair produced a firm bearish session, continuing the retreat from the September peak above 0.6700 and slipping back into a key support area. Price is now testing the 50-day moving average at 0.6538, with the 100-day just below at 0.6514, leaving the 0.6500 zone pivotal in the near term. The 200-day moving average at 0.6399 offers deeper support further down. Sellers have repeatedly capped advances near 0.6650, and the latest rejection underlines near-term dominance by bears. Resistance is now at 0.6580 and then 0.6620, while a close below 0.6500 would expose 0.6460 and 0.6400.

- Gold Holds Firm as Rally Consolidates Near Highs: Gold ended at $3,745, up 0.28%, after trading between $3,761 and $3,722. The session produced a contained range, with buyers defending dips and keeping price within reach of recent highs. The broader rally since early September remains well supported, with price holding comfortably above all major moving averages, the 50-day at $3,466, the 100-day at $3,396, and the 200-day at $3,153. The steepness of the recent climb raises the risk of corrective swings, yet the structure remains firmly bullish. Immediate resistance is seen at $3,760–3,780, while support lies at $3,720 and then $3,680, levels that could be retested on consolidation.

Market Movers:

- Chip Stocks Weigh on Nasdaq: Micron Technology fell more than 3%, while ARM Holdings and ON Semiconductor lost over 2%. Other sector names including Microchip Technology, Broadcom, Qualcomm, NXP Semiconductors and Texas Instruments also slipped more than 1%, dragging the group lower.

- Crypto-Linked Shares Retreat: Bitcoin’s drop of more than 2% to a two-week low hit cryptocurrency-exposed companies. MicroStrategy tumbled more than 7%, while Coinbase, MARA Holdings, Riot Platforms, Galaxy Digital and Bit Digital all fell over 4%.

- CarMax Slumps on Weak Results: CarMax shares sank more than 20% after reporting Q2 sales and revenue of $6.59 billion, well below expectations of $7.01 billion.

- Intel Gains on Apple Investment Report: Intel surged over 8% after reports the company approached Apple about securing an investment. The move lifted the stock to the top of the S&P 500 and Nasdaq 100.

- IBM Rallies on Quantum Breakthrough: IBM advanced more than 5% to lead gainers in the Dow after HSBC highlighted progress using the firm’s Heron quantum processor to improve bond price predictions in financial markets.

- Freeport-McMoRan Extends Heavy Losses: Freeport-McMoRan fell over 6%, compounding a 16% plunge the previous day after the company suspended activity at its Grasberg mine in Indonesia following a fatal mudslide and declared force majeure on copper contracts.

- Lithium Names Surge on US Interest: Lithium Americas jumped more than 22%, adding to Wednesday’s near-doubling after reports the Trump administration may seek a stake in the company. Albemarle also gained more than 4% on the news.

Equities extended their pullback as investors weighed stretched valuations, rising yields and fading momentum in high-profile technology stocks such as Oracle and Tesla. Stronger economic data added to the pressure by clouding prospects for further Fed easing, while caution over upcoming inflation figures and political risks limited risk appetite. With Europe and Asia also showing uneven performances, markets remain finely balanced as participants look for fresh direction into the end of the week.