Wall Street ended Tuesday at record highs, with investors balancing weak labour market signals against hopes that forthcoming inflation data will support rate cuts. The Bureau of Labor Statistics revealed that nearly one million jobs were overcounted in the year through March, the largest downward revision since 2002. While the figures revived questions over the economy’s strength, markets largely dismissed them as backward-looking and instead focused on producer and consumer price reports due this week, which are expected to heavily influence the Federal Reserve’s September meeting. Gains in healthcare shares and renewed merger activity underpinned sentiment, even as global markets faced political uncertainty in Europe and Asia.

Key Takeaways:

- Dow Gains on Healthcare Surge: The Dow Jones Industrial Average rose 196 points, or 0.43%, to 45,711.34 as UnitedHealth rallied more than 8% and lifted peers including Centene, Molina, Elevance and CVS.

- S&P 500 Extends Record Run: The S&P 500 added 0.27% to 6,512.61 for another record finish. Healthcare leadership offset a pullback in semiconductors, with Broadcom easing more than 2% after a strong one-week advance near 13%.

- Nasdaq Sets Fresh Highs: The Nasdaq Composite climbed 0.37% to 21,879.49, achieving both a record close and a new all-time intraday high. Chip momentum remained a key support even as some recent winners consolidated.

- Europe Mixed Amid Political Shifts: The Stoxx 600 edged up 0.09% after a choppy session, masking divergent national moves. France’s CAC 40 rose 0.2% to 7,749.40 as markets absorbed the ousting of Prime Minister François Bayrou and the prospect of President Macron appointing a fifth prime minister in under two years. London’s FTSE 100 gained 0.23% to 9,242.53, aided by a 9% jump in Anglo American after agreeing to merge with Teck Resources to form “Anglo Teck,” a top-five copper producer to be headquartered in Canada and listed in New York, Toronto, London and Johannesburg; Anglo shareholders will own 62.4% and Teck holders 37.6%. Germany’s DAX slipped 0.4% to 23,733, while Italy’s FTSE MIB rose 0.68%. UK retail data also firmed, with BRC sales up 3.1% year on year in August, led by food and back-to-school demand.

- Asia-Pacific Shows Divergence: Japan’s Nikkei 225 fell 0.42% to 43,459.29 after touching a record high, with politics in focus following Prime Minister Shigeru Ishiba’s resignation; the Topix dipped 0.51%. South Korea’s Kospi gained 1.26% for a sixth straight rise, while the Kosdaq added 0.76%. Australia’s ASX 200 slid 0.52% as consumer sentiment retreated. Hong Kong’s Hang Seng rose 1.19% to its highest since 2021, but China’s CSI 300 fell 0.7%. Indonesia’s Jakarta Composite dropped 1.82% after the finance minister’s dismissal, with the rupiah weakening; India’s Nifty 50 rose 0.29% and the Sensex 0.2%. Thailand reported 22.39 million foreign visitors year-to-date, down 7.1% on the year.

- Oil Rises on Middle East Escalation: Brent settled up 0.56% at $66.39 and WTI gained 0.59% to $62.63 after Israel said it carried out an attack on Hamas leadership in Doha, Qatar, drawing regional condemnation. Traders also looked to US inventory data and monthly OPEC and IEA reports later in the week.

- Yields Firm Ahead of Inflation Data: US Treasury yields edged higher as investors awaited the August PPI on Wednesday and CPI on Thursday before the 16–17 September Fed meeting. The 10-year yield rose a little over 3 bps to 4.08%, while the 2-year gained more than 5 bps to 3.55%, reflecting positioning into the data.

- US Job Growth Marked Down Sharply: The Bureau of Labor Statistics cut non-farm payroll gains for the 12 months through March by 911,000, the largest downward revision since 2002. Although backward-looking, the downgrade adds to signs of a cooling labour market; summer monthly payroll growth averaged just 29,000, intensifying debate over the scale of rate cuts.

FX Today:

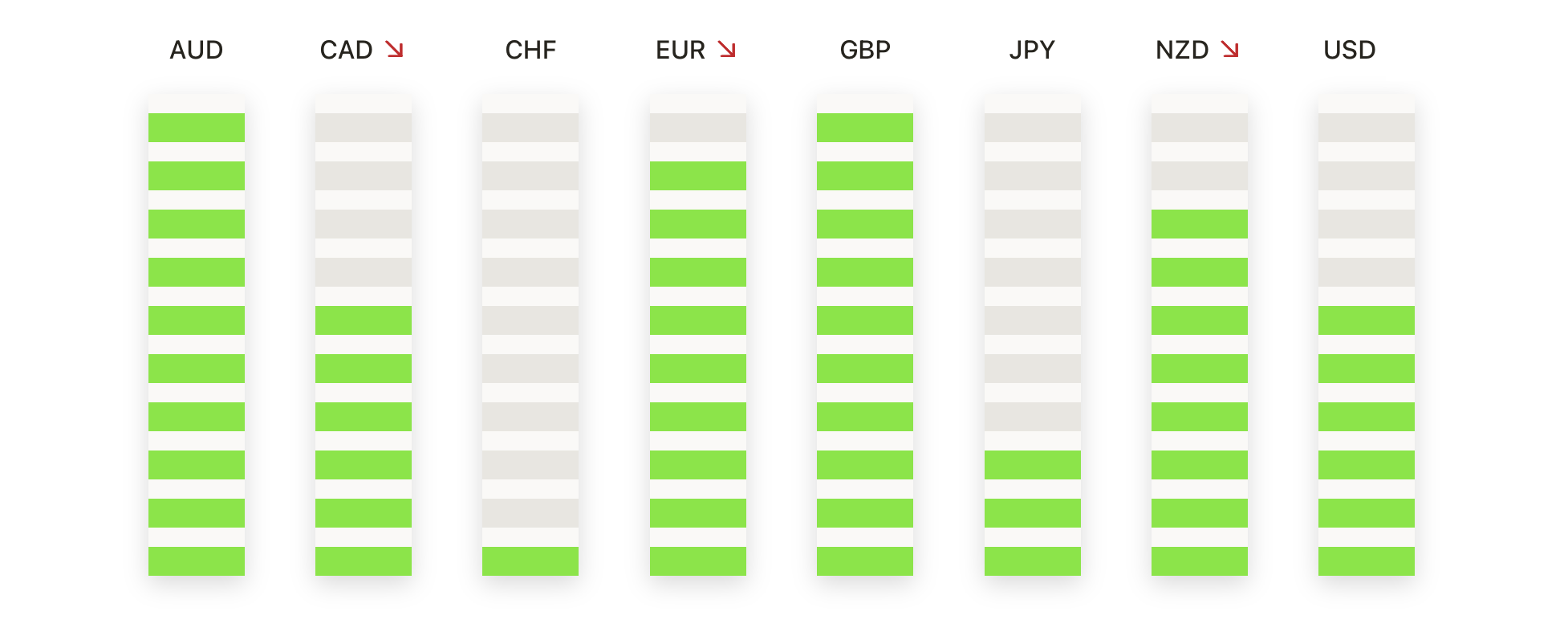

- EUR/USD Pulls Back After Testing Resistance: EUR/USD closed at 1.1706, down 0.48%, after reaching a session high of 1.1780 and a low of 1.1704. Price remains supported by the 50-day moving average at 1.1662 and the 100-day at 1.1533, while the 200-day continues to climb beneath at 1.1076, leaving the medium-term structure intact. Buyers have repeatedly held the 1.1650 area since early August, but failures around 1.1780–1.1800 highlight persistent overhead resistance.

- GBP/USD Retreats from 1.3600 Barrier: GBP/USD closed at 1.3519, down 0.19%, after posting a high of 1.3591 and ending on its session low. The pair continues to hover around the 50-day moving average at 1.3470 and the 100-day at 1.3462, with the 200-day trending higher below at 1.3074 to support the broader outlook. Since the August trough near 1.3300, higher lows have improved the medium-term tone, though upside traction stays capped. Key support now lies at 1.3460 and then 1.3400, while resistance is anchored at 1.3600. A decisive move above this level would open 1.3700, but continued failure may extend consolidation in the 1.3400–1.3600 band.

- EUR/GBP Drifts Lower Toward Support Zone: EUR/GBP closed at 0.8659, down 0.28%, after trading between 0.8683 and 0.8655. Price has been largely rangebound since mid-August, with buyers holding the 0.8600 floor while rallies stall near 0.8720. The 50-day moving average at 0.8655 now acts as immediate support, while the 100-day at 0.8564 and the 200-day at 0.8465 sit beneath to underpin the broader structure. While higher lows keep the outlook constructive, upside momentum has struggled to sustain. A break below 0.8650 would expose 0.8620 and 0.8600, while holding above the current zone could bring another push toward 0.8700–0.8720.

- USD/CAD Extends Recovery as Buyers Eye Resistance: USD/CAD closed at 1.3859, up 0.41%, after recording a high of 1.3886 and a low of 1.3793. The pair now trades above the 50-day moving average at 1.3750 and the 100-day at 1.3763, while pressing the 200-day at 1.4017, which continues to slope lower and serves as key resistance. Since mid-July, buyers have repeatedly defended 1.3650, establishing a higher base that has fuelled the rally. The 1.3900 region remains the critical cap, with a break higher opening the way to 1.4000. On the downside, immediate support rests at 1.3800 and then 1.3750, with a drop below these levels likely to spark a fresh corrective phase.

- Gold Holds Firm Above $3,600 After Rejection at Highs: Gold closed at $3,629, down 0.16%, after climbing to a high of $3,674 and dipping to $3,627 intraday. A small red candle suggested profit-taking after several strong sessions, but the broader uptrend remains intact. Price continues to trade well above the 50-day moving average at $3,380 and the 100-day at $3,352, with the 200-day also trending higher beneath at $3,090. The surge above $3,400 in late August marked a major breakout, and momentum has since accelerated with successive higher highs. Resistance emerged near $3,675, though the close well above $3,600 preserves a constructive bias. Support now lies at $3,600 and $3,550, while a decisive push above $3,675 would target the $3,700 handle. Failure to hold above $3,600 could prompt a retracement toward the breakout area around $3,500.

Market Movers:

- Tourmaline Bio Soars as Novartis Confirms Buyout: Tourmaline Bio rocketed more than 57% after Novartis announced a $1.4 billion acquisition valued at roughly $48 per share, fuelling optimism for renewed biotech deal-making.

- Nebius Group Leaps After Microsoft GPU Agreement: Nebius Group NV surged nearly 49% after unveiling a deal to provide Microsoft with GPU infrastructure capacity at its New Jersey data centre over the next five years.

- Brighthouse Financial Rallies Amid Takeover Talks: Brighthouse Financial jumped more than 12% following a Financial Times report that Aquarian Holdings is in late-stage discussions with two Middle Eastern investors to finance a potential buyout.

- CoreWeave Climbs as New AI Ventures Arm Launches: CoreWeave gained over 7% after unveiling CoreWeave Ventures, a new unit designed to back companies developing platforms and technologies across the AI ecosystem.

- Humana Slides After Medicare Ratings Concern: Humana tumbled more than 12% after analysts highlighted changes to Medicare quality thresholds that could make bonus payments harder to achieve, a significant risk given its heavy reliance on private Medicare Advantage plans.

- Albemarle Drops as Lithium Mine Restarts: Albemarle sank more than 11% after Chinese media reported that CATL’s lithium mine, previously suspended, is resuming production, putting fresh pressure on lithium markets and producers.

- Fox Corp Declines After Murdoch Family Share Sale: Fox Corporation slipped more than 6% after trusts set up for Rupert Murdoch’s children announced plans to sell 16.9 million Class B shares.

Markets demonstrated notable resilience on Tuesday, with all three major US indices closing at record levels despite the sharp downward revision to jobs growth and ongoing signs of economic softness. Investor focus is now firmly on upcoming inflation data, which could set the tone for the Federal Reserve’s policy meeting next week. The rally was supported by healthcare strength and merger activity in resources, while overseas trading reflected a mix of political turbulence in Europe and leadership uncertainty in Japan. Oil prices firmed on heightened geopolitical tensions, and yields edged higher as traders positioned for key inflation prints. Adding a further layer of uncertainty, the US Supreme Court agreed to fast-track a case on the legality of President Trump’s tariffs, with oral arguments scheduled for November, keeping trade policy risks firmly in play alongside monetary and economic challenges.