Wall Street opened the week in cautious fashion as a long-awaited trade deal between the US and European Union failed to lift sentiment meaningfully, with investors instead turning their focus to a potentially pivotal stretch of central bank decisions and corporate earnings. This week brings one of the busiest earnings schedules of the season, alongside the Federal Reserve’s latest policy statement and a raft of labour market data that could shape expectations for rate cuts into the autumn. With risk appetite tempered by uncertainty, equities struggled for direction, bond yields edged higher, and commodities responded more sharply to geopolitical headlines.

Key Takeaways:

- S&P 500 Closes Flat After Brief Record High: The S&P 500 edged up 0.02% to 6,389.77 after briefly touching a fresh intraday high, but failed to hold gains as enthusiasm over the US-EU trade deal quickly faded. Investors turned their focus to a packed week featuring the Federal Reserve’s policy meeting and over 150 S&P 500 earnings, including Microsoft, Meta, Amazon, and Apple.

- Dow Slips, Nasdaq Outperforms as Semis Lift Tech: The Dow Jones Industrial Average dipped 64.36 points, or 0.14%, to 44,837.56, weighed by cautious sentiment ahead of Wednesday’s FOMC decision. The Nasdaq Composite rose 0.33% to a record 21,178.58, led by strength in AI-linked chipmakers and server hardware stocks.

- European Stocks Retreat as Trade Optimism Disappears: The Stoxx 600 closed down 0.23% as initial enthusiasm over the US-EU tariff deal faded. Germany’s DAX dropped 1.02%, Paris’ CAC 40 pared a 0.9% intraday gain to end flat, and London’s FTSE 100 declined 0.43%, extending its two-day slide. Autos led losses, falling 1.8% amid warnings of higher costs. UK goods exports fell to a record-low 40.8% share of total trade, reinforcing the UK’s shift toward services. Meanwhile, CBI data showed UK retail sales remained in contraction for a tenth straight month, with July’s reading at -34, better than June’s -46.

- Asia-Pacific Markets Mixed as Trade Talks With China Begin: Markets across the region saw uneven performance as US-China negotiations commenced in Stockholm. China’s CSI 300 rose 0.21% and Hong Kong’s Hang Seng added 0.68%, led by rare earth and insurer gains. Samsung shares surged over 6% in Seoul on confirmation of a $16.5 billion chip deal with Tesla, lifting the Kospi 0.42%, though the Kosdaq slipped 0.32%. Indonesia’s benchmark jumped 1.34% to a nine-month high, Vietnam extended its rally to a five-day win streak, and Australia’s ASX 200 rose 0.36%. India’s Nifty 50 fell 0.60% as profit-taking set in after recent strength.

- Oil Prices Jump as EU Energy Commitments and Russia Deadline Boost Bulls: Brent crude rose 2.34% to $70.04 and WTI gained 2.38% to $66.71 after President Trump shortened his deadline for Russia to end the war and confirmed Europe’s large-scale US energy purchases. LNG stocks rallied, and OPEC+ reiterated calls for compliance ahead of a production decision due Sunday.

- Treasury Yields Edge Higher Ahead of Fed and Inflation Data: Bond markets were steady but upwardly pressured, with the 10-year yield rising to 4.416%, the 2-year at 3.93%, and the 30-year at 4.963%. Traders remain sensitive to any hint of a September rate cut, especially as new tariffs add uncertainty to the inflation outlook.

FX Today:

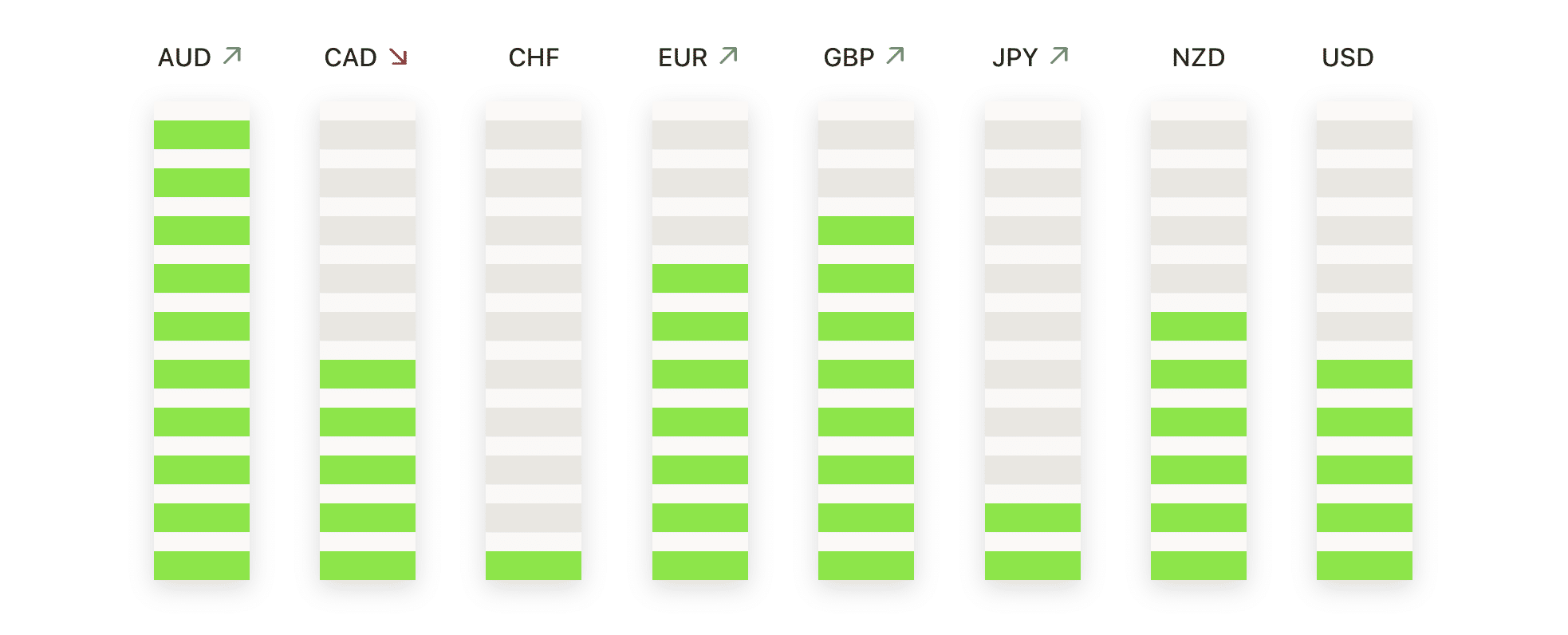

- EUR/USD Breaks Down to 50-Day SMA as Double-Top Reversal Gathers Pace: EUR/USD closed at 1.1589, falling 1.30% after printing a high of 1.1771 and a low of 1.1585 in its steepest one-day drop since early June. Monday’s large red candle marked a third consecutive daily decline and drove price directly into the rising 50-day SMA at 1.1564, which now acts as immediate support. The move confirms a double-top rejection from the 1.1900 region, where price failed twice during July, with momentum clearly turning against the prior bullish trend. The 50-day average is the last defence before deeper levels at 1.1440 and the 100-day base near 1.1340 come into play. A bounce above 1.1670 could help stabilise the pair, but only a close back above 1.1770 would neutralise current bearish pressure.

- GBP/USD Falls Below 50-Day SMA as Sellers Regain Short-Term Control: GBP/USD ended the session at 1.3354, down 0.61% after reaching a high of 1.3453 and a low of 1.3352, closing beneath the 50-day SMA at 1.3532 for the first time in over a month. This marks the third straight red candle for the pair, confirming the loss of bullish momentum and shifting the near-term focus to the 100-day SMA at 1.3329, which sits just below current price. Despite the 100-day and 200-day SMAs rising at 1.3329 and 1.2978 respectively, July’s sharp pullback has now erased most of the month’s gains. The failure to hold the July high near 1.3800 and the break of trend support beneath the 50-day average points to a deeper correction unfolding. If the 100-day SMA fails to hold, bears could drive price toward 1.3250 and potentially the 1.3000–1.2980 zone anchored by the 200-day. On the upside, a rebound above 1.3450 is needed to restore stability and reopen the 1.3530–1.3600 resistance band.

- USD/JPY Tests Resistance Zone as Bulls Push Toward 200-Day SMA: USD/JPY settled at 148.54, climbing 0.60% after reaching a high of 148.58 and a low of 147.51 as buyers extended their control into a third consecutive session. Monday’s strong green candle advanced the rally from mid-July, lifting the pair above both the 50-day SMA at 145.28 and the 100-day at 145.67, with price now just beneath the 200-day SMA at 149.54. Since bottoming below 141 earlier this month, the pair has rebounded sharply, reclaiming key levels and entering a significant resistance band between 148.50 and 149.50. Momentum remains bullish above 147.00, but the approach toward the 200-day may trigger exhaustion and profit-taking. A break above 149.50 would expose the 151.00 region, while failure to clear resistance could prompt a retreat toward 147.30 or the 100-day SMA near 145.67.

- EUR/GBP Eases From Highs but Maintains Strong Bullish Structure: EUR/GBP ended the day at 0.8679, slipping 0.64% after reaching a high of 0.8752 and a low of 0.8667. The dip marked the second red candle in a row but remains contained within a well-established uptrend that has been in place since mid-May. The 50-day, 100-day, and 200-day SMAs all continue to rise steadily at 0.8544, 0.8503, and 0.8415 respectively, underscoring the strength of the underlying bullish structure. Monday’s rejection from 0.8750 appears corrective rather than trend-ending, and as long as price holds above 0.8600 and especially above the 50-day SMA, the upward trajectory remains intact. A move back above 0.8720 would resume the rally and open the way toward 0.8780 and 0.8820. However, a daily close below 0.8600 would soften the short-term outlook and invite a retest of the breakout zone near 0.8540.

- Gold Slips Below Key Support as Bears Eye Deeper Pullback Toward $3,300: Gold closed at $3,317, declining 0.55% after trading between a high of $3,345 and a low of $3,301 as the metal posted its fourth straight red daily candle. Monday’s session produced a clean break beneath the 50-day SMA at $3,335, with price closing well below that key level for the first time since May and signalling a shift in short-term control. While the broader trend remains bullish, with the 100-day and 200-day SMAs still rising at $3,242 and $2,982 respectively, momentum has clearly weakened following last week’s failure to hold above $3,400. Near-term bias has turned bearish, with price sitting just above $3,300 and no immediate signs of support beyond that. A clean break under $3,300 would open the path toward the 100-day SMA at $3,242, with the $3,260 level also offering minor support.

Market Movers:

- Super Micro Computer Soars on AI Optimism: Shares surged over 10% to lead the S&P 500 after investor enthusiasm grew around continued demand for its AI server products.

- AMD and Semiconductor Stocks Rally on Trade Deal Relief: Advanced Micro Devices jumped 4% while ON, KLA, ASML, and Marvell rose 2–3% as chipmakers benefitted from reduced US-EU tariff uncertainty.

- Energy Stocks Rise as Oil Prices Jump 2%: Diamondback Energy gained 4%, Devon rose 3%, and APA, ConocoPhillips, and Phillips 66 all advanced over 2% as crude rallied on geopolitical headlines.

- LNG and Gas Exporters Gain on EU Commitments: Venture Global surged 4% and Cheniere Energy added 1% after the EU pledged major US energy purchases as part of the trade deal.

- Nike Advances After JPMorgan Upgrade: The stock led Dow gainers after analysts raised their rating to overweight with a $93 target, citing improved brand momentum.

- Revvity Sinks on Weaker Earnings Outlook: The company cut its full-year EPS forecast below consensus, triggering the steepest drop in the S&P 500 on the day.

- Centene Falls After Downgrade: Shares declined after Cantor Fitzgerald downgraded the stock to neutral, citing limited near-term catalysts.

- Coinbase Slides on Analyst Downgrade: The stock dropped after Monness Crespi Hardt cut its rating to neutral from buy, citing valuation concerns.

- Gilead Drops on Regulatory Risk: Investors reacted to reports that HHS may disband a key advisory panel, raising questions about future coverage of HIV prevention drugs.

Markets opened the week cautiously as investors looked beyond the US-EU tariff breakthrough and focused instead on the more immediate drivers ahead, including the Federal Reserve’s policy decision, earnings from key tech names, and a closely watched US jobs report. While chip and energy stocks outperformed on trade-related headlines and rising oil prices, broader sentiment remained restrained across global equities. European markets lost ground as optimism over the trade deal faded, and mixed moves in Asia reflected anticipation ahead of renewed US-China talks.