European markets lost ground on Friday as investors grew wary of renewed US tariffs and the lack of progress on trade deals, while losses in banking and mining shares weighed on broader sentiment. Asian markets were also subdued ahead of President Trump’s tariff deadline this week, adding to the cautious tone globally. Oil prices slipped on expectations of another OPEC+ output hike, while gold held firm in a tight consolidation zone. Meanwhile, currency markets showed mixed moves, with the dollar broadly softer against major peers. With US markets closed on Friday for the 4 July holiday, traders are set to return with fresh focus on tariffs and economic data in the days ahead.

Key Takeaways:

- European Stocks Retreat as Tariff Risks Mount: European shares closed broadly lower on Friday as renewed fears over the expiry of a US tariff pause and worries about stalled trade negotiations weighed on sentiment. The Stoxx Europe 600 fell 0.48% to 541.14, while Paris’ CAC 40 dropped 0.76%, Frankfurt’s DAX declined 0.61%, and Milan’s FTSE MIB shed 0.80%. London’s FTSE 100 posted a modest weekly gain of 0.27% to finish at 8,822.91, supported partly by strength in defensive healthcare names. Eurozone banks slumped 1.3%, led by BBVA with a 2.6% slide. Mining stocks also underperformed on weaker commodity sentiment. Spirits makers such as Pernod Ricard, Remy Cointreau, and LVMH, however, bounced from session lows after China spared certain EU cognac producers from new duties provided minimum pricing is observed, helping to limit broader market losses.

- German and Italian Data Add to Europe Concerns: Industrial data from Germany showed a much sharper-than-expected decline in May, with orders tumbling 3.1% overall, and a dramatic 17.7% drop in orders for computer, electronic, and optical products after a large April spike. Domestic eurozone demand remained weak, with orders down 6.5% from neighbouring partners. In Italy, retail sales disappointed, falling 0.4% month-on-month in May after a modest gain in April, missing forecasts for continued growth, raising concerns about the consumer backdrop in southern Europe.

- Asian Markets Trade Uneven Ahead of Tariff Decisions: Asia-Pacific markets showed mixed to negative performance on Friday as traders braced for potential tariff changes from the United States. Japan’s Nikkei 225 closed flat, while the broader Topix also held steady at 2,827.95, supported by robust household spending data showing an 8.9% annual rise in May. In South Korea, the Kospi tumbled 1.99% and the Kosdaq lost 2.21%, with renewed selling hitting technology names despite a strong improvement in the country’s current account surplus to $10.14 billion. Hong Kong’s Hang Seng fell 0.64%, reversing a 1.5% gain for the prior week, as investor caution dominated ahead of President Trump’s tariff deadline. Mainland China’s CSI 300 index managed a 0.36% rise to 3,982.20, underpinned by selective bargain buying. In Australia, the ASX 200 finished flat, consolidating strong gains from earlier in the week, while Indian benchmarks saw mild declines with the Nifty 50 down 0.17% and the Sensex off 0.18%. Indonesia’s Jakarta Composite fell for a fourth straight session, down 0.42%, as traders reacted to a proposed $34 billion import agreement with US partners ahead of the tariff deadline.

- Oil Slips Ahead of OPEC+ Output Decision: Oil prices fell more than 1% on Friday as traders anticipated a further production hike by OPEC+. Market watchers expect the alliance to raise August output by another 411,000 barrels per day, extending four consecutive months of increases, potentially leading to a sizeable build in global reserves during the second half of 2025. Brent crude still ended about 0.5% higher for the week, with WTI roughly 1.2% stronger from last Friday’s close. Barclays raised its Brent price outlook by $6 to $72 for 2025.

- Bitcoin Sees Record ‘Satoshi Era’ Transfers: On Friday, more than $8 billion worth of bitcoin mined during the so-called “Satoshi era” was moved in what analysts described as the largest transfer of its kind. Two wallets dormant for over 14 years each shifted 10,000 BTC, initially mined in 2011 when bitcoin traded at just 78 cents, to new addresses. Another six wallets moved an additional 60,000 BTC in rapid succession, bringing the total to 80,000 BTC worth over $8.6 billion at current prices. Blockchain analysis suggested all eight wallets are controlled by the same entity, although no one has come forward publicly to claim ownership. The new addresses have not moved the coins further, leaving the ultimate intent unknown.

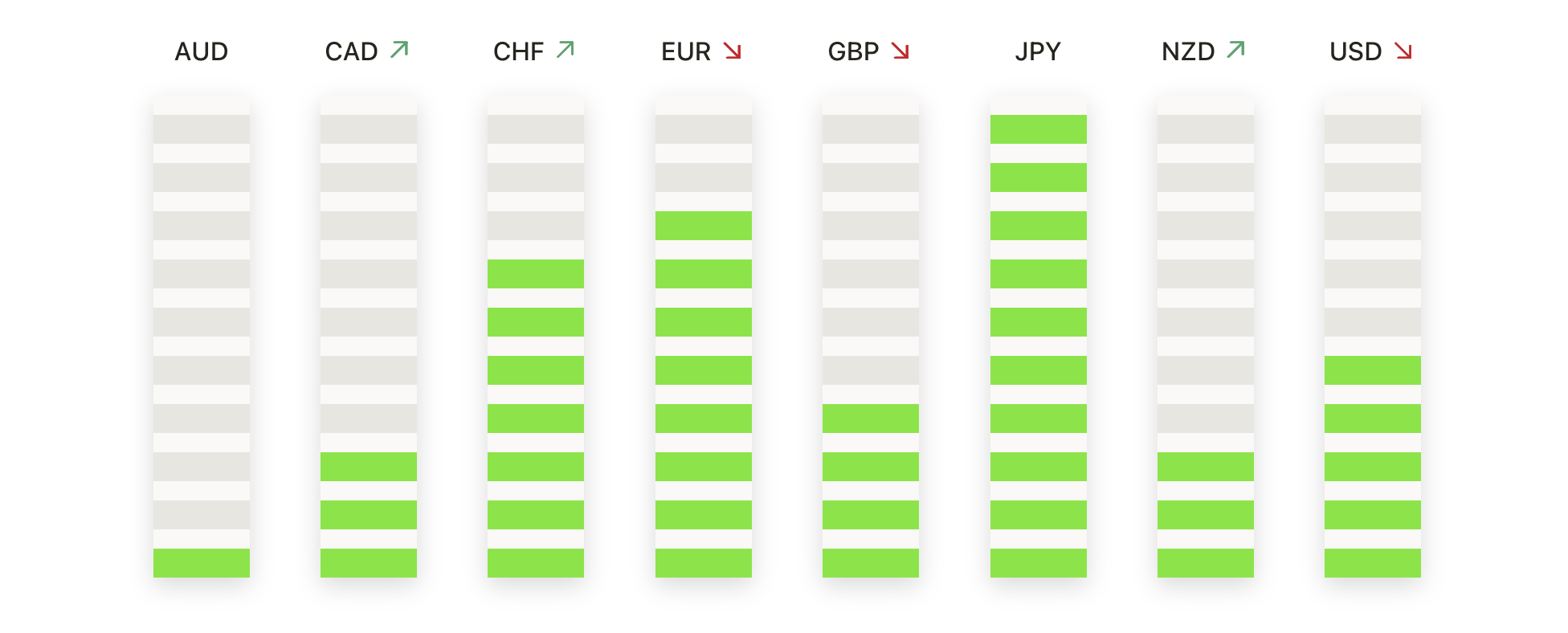

FX Today:

- EUR/USD Holds Firm Near 1.1800: The euro closed at 1.1774 on Friday, gaining 0.15% after trading between 1.1750 and 1.1787. EUR/USD has extended its robust uptrend from March, comfortably above its 50-day simple moving average at 1.1428, the 100-day at 1.1580, and the 200-day at 1.0872. Buyers continue to defend minor pullbacks around 1.1500, keeping the pair well supported while aiming for the psychological barrier at 1.1800. A successful break above that level may drive prices toward 1.1850 or higher in the coming sessions. If a short-term correction emerges, support is seen around 1.1650, with the rising 50-day average providing a more solid floor.

- GBP/USD Steadies Below 1.3700 After Recent Surge: Sterling settled at 1.3651 on Friday, edging down 0.02% after hitting a daily high of 1.3681 and a low of 1.3636. GBP/USD retains a strong bullish tone after rallying from mid-April, holding above its 50-day simple moving average at 1.3474, the 100-day at 1.3204, and the 200-day at 1.2951. The pair has consistently formed higher highs and higher lows, suggesting any near-term weakness may draw fresh buying interest. Resistance remains just below the 1.3700 level, with a clean break above that potentially targeting 1.3800. Initial support rests near 1.3500, with deeper backing at the 50-day average.

- USD/JPY Weakens Further Toward Key Support: The yen strengthened on Friday, pushing USD/JPY down 0.23% to settle at 144.57 after a range of 144.17 to 144.97. The pair continues to struggle beneath its 50-day SMA at 144.48, the 100-day at 146.02, and the 200-day at 149.54, highlighting persistent bearish momentum. Sellers have repeatedly faded rebound attempts, keeping pressure on the pair since its March peak near 158.00. If weakness persists, USD/JPY could retest support around 143.50, with 142.00 as the next possible downside target. A recovery back above the 146.00 handle would be needed to shift the bias and challenge the declining trend.

- USD/CAD Remains Heavy Near 1.3600 in Prolonged Downtrend: USD/CAD ended Friday at 1.3605, up 0.18% after moving between 1.3565 and 1.3616. Despite the modest uptick, the pair remains within a bearish pattern defined by lower highs and lower lows since peaking in April, with the 50-day SMA at 1.3760, the 100-day at 1.3979, and the 200-day at 1.4035 providing layers of resistance. Friday’s small-bodied green candle suggests more of a pause than a reversal, with immediate resistance at 1.3700 and stronger caps near the 50-day average. Short-term support rests at 1.3550 and the psychological 1.3500 zone.

- EUR/GBP Consolidates Above Recent Breakout: The euro-pound cross finished at 0.8625 on Friday, advancing 0.18% after trading between 0.8603 and 0.8637. EUR/GBP has pushed sharply higher in recent weeks, comfortably above its 50-day SMA at 0.8479, the 100-day at 0.8446, and the 200-day at 0.8390. Friday’s action showed only mild consolidation near the highs, suggesting the breakout remains intact. Traders may look for an immediate upside test of 0.8650 if momentum resumes, while the prior resistance near 0.8550 could now act as first support. A deeper pullback might find more robust backing around 0.8500, where the 50-day average is converging.

- Gold Holds Steady Near $3,334 Amid Tight Consolidation: Spot gold closed Friday at $3,334, gaining 0.26% after ranging between $3,324 and $3,345. The yellow metal continues to respect its rising trend structure, holding well above its 50-day SMA at $3,321, the 100-day at $3,177, and the 200-day at $2,928. Despite a slowdown in upside momentum since peaking in early May, higher lows and shallow pullbacks suggest the medium-term bullish posture is intact. Immediate resistance is seen around $3,350, with a break potentially targeting $3,400 or higher. First support is near $3,320, with stronger backing at $3,200 if prices correct further.

Market Movers:

- Chip Stocks Rally on China Export News: Semiconductor names posted strong gains, with Intel up 2.4%, and Broadcom, ON Semiconductor, Nvidia, and Marvell Technology all advancing more than 1%. Synopsys and Cadence Design surged over 4% after the US lifted licence restrictions on chip design software sales to China, improving prospects for resuming business in the region.

- ASML Drops on Samsung Factory Slowdown: Shares of ASML fell 0.6% after a Nikkei Asia report indicated Samsung Electronics is delaying the ramp-up of its new Texas chip plant due to weak demand, raising questions over the pace of equipment installations in the facility.

- FedEx Gains on Double Upgrade: FedEx shares rose 0.8% after BNP Paribas upgraded the stock by two notches, citing oversold conditions and expectations that it will outperform rival UPS in coming quarters.

- Olo Surges on Buyout Deal: Restaurant software firm Olo closed up more than 13% after revealing it would be acquired by private equity giant Thoma Bravo for $10.25 per share in cash, valuing the deal above $1 billion.

Asian and European markets ended the week under pressure as trade concerns and soft regional data weighed on sentiment, while investors remained wary of President Trump’s upcoming tariff decisions. Oil traders looked to the OPEC+ meeting for fresh signals on production policy, and gold continued to consolidate at elevated levels. Bitcoin, meanwhile, drew headlines after a record movement of Satoshi-era coins sparked speculation across the crypto community. With US markets returning from the Independence Day holiday, traders will focus on renewed trade negotiations, inflation data, and corporate earnings over the coming days to gauge the market’s next direction.