Stocks climbed on Thursday as markets weighed a stronger-than-expected monthly inflation reading against growing signs of a slowing US economy, leaving expectations for a Federal Reserve rate cut next week firmly intact. The Dow surged more than 600 points to close at a fresh record, while the S&P 500 and Nasdaq also settled at all-time highs after touching new intraday peaks during the session. Although consumer prices rose more than forecast on the month, the annual pace of inflation remained aligned with expectations, easing fears that higher price pressures might derail monetary easing. A drop in Treasury yields and a jump in jobless claims reinforced the sense that growth is cooling, boosting bets that the Fed will cut by at least a quarter point at its September meeting.

Key Takeaways:

- Dow Surges to Record Highs on Rate Cut Hopes: The Dow Jones Industrial Average jumped 617.08 points, or 1.36%, to close at 46,108.00, its highest ever. Gains were broad-based, with financials and consumer stocks among the leaders.

- S&P 500 Climbs as Inflation Fails to Deter Bulls: The S&P 500 advanced 0.85% to finish at 6,587.47, also setting a new record close. Traders looked past the hotter-than-expected monthly CPI print, focusing instead on signs of economic softening and the likelihood of Fed easing.

- Nasdaq Extends Gains to All-Time High: The Nasdaq Composite rose 0.72% to settle at 22,043.07, after touching a fresh intraday high earlier in the session. Semiconductor names, led by Micron and Lam Research, provided notable support.

- US Consumer Inflation Climbs While Jobless Claims Spike to Multi-Year High: Inflation accelerated in August, with CPI up 0.4%, the strongest monthly rise since January, as shelter and food costs pushed prices higher. Grocery prices jumped 0.6% amid tariffs on coffee, import duties on beef and farm labour shortages tied to immigration crackdowns. Annual CPI came in at 2.9%, matching forecasts and up from 2.7% in July, while core inflation held at 0.3% on the month and 3.1% year on year. Alongside this, weekly jobless claims unexpectedly rose by 27,000 to 263,000, well above expectations and marking the highest level since October 2021, reinforcing evidence of a slowing labour market.

- European Stocks Advance After ECB Holds Rates Steady: Europe’s major indices closed higher as investors absorbed the European Central Bank’s decision to keep its deposit rate unchanged at 2%. The pan-European Stoxx 600 gained 0.51%, the FTSE 100 rose 0.78% to 9,297.58, and France’s CAC 40 climbed 0.75%. Germany’s DAX added 0.30% to 23,703.65, while Italy’s FTSE MIB rose 0.89%. Auto stocks led the rebound, with Stellantis surging more than 9% after outlining plans to reintroduce key models to boost sales. Analysts were split on the ECB’s outlook, with some suggesting another cut remains possible later this year while others argued rates are now on hold.

- Asia Mixed as Japan and South Korea Hit Records: Japan’s Nikkei 225 set a new all-time high at 44,396.95 before closing 1.22% higher at 44,372.5, driven by a more than 10% surge in SoftBank on optimism around cloud-computing partnerships. South Korea’s Kospi also reached record territory, rising 0.9% to 3,344.2. Gains were less uniform elsewhere, with Australia’s ASX 200 down 0.29% and Hong Kong’s Hang Seng off 0.21%, though mainland China’s CSI 300 jumped 2.31% and Taiwan’s TSMC-led rally pushed the Taiex to a fresh high at 25,541.

- Oil Slides on Oversupply Concerns: Brent crude fell 1.66% to $66.37 a barrel, while WTI dropped 2.04% to $62.37 as oversupply worries weighed on sentiment. Rising US inventories and the International Energy Agency’s warning of potential market oversupply offset geopolitical risks tied to conflicts in the Middle East and Ukraine.

- Treasury Yields Fall as Jobless Claims Rise: The 10-year Treasury yield dropped to 4.00% after data showed consumer inflation rising 0.4% on the month and jobless claims jumping to 263,000, the highest since October 2021. The figures reinforced expectations of softer growth, boosting market confidence in at least a quarter-point rate cut at the Fed’s September meeting, with traders assigning some chance to a larger half-point move.

FX Today:

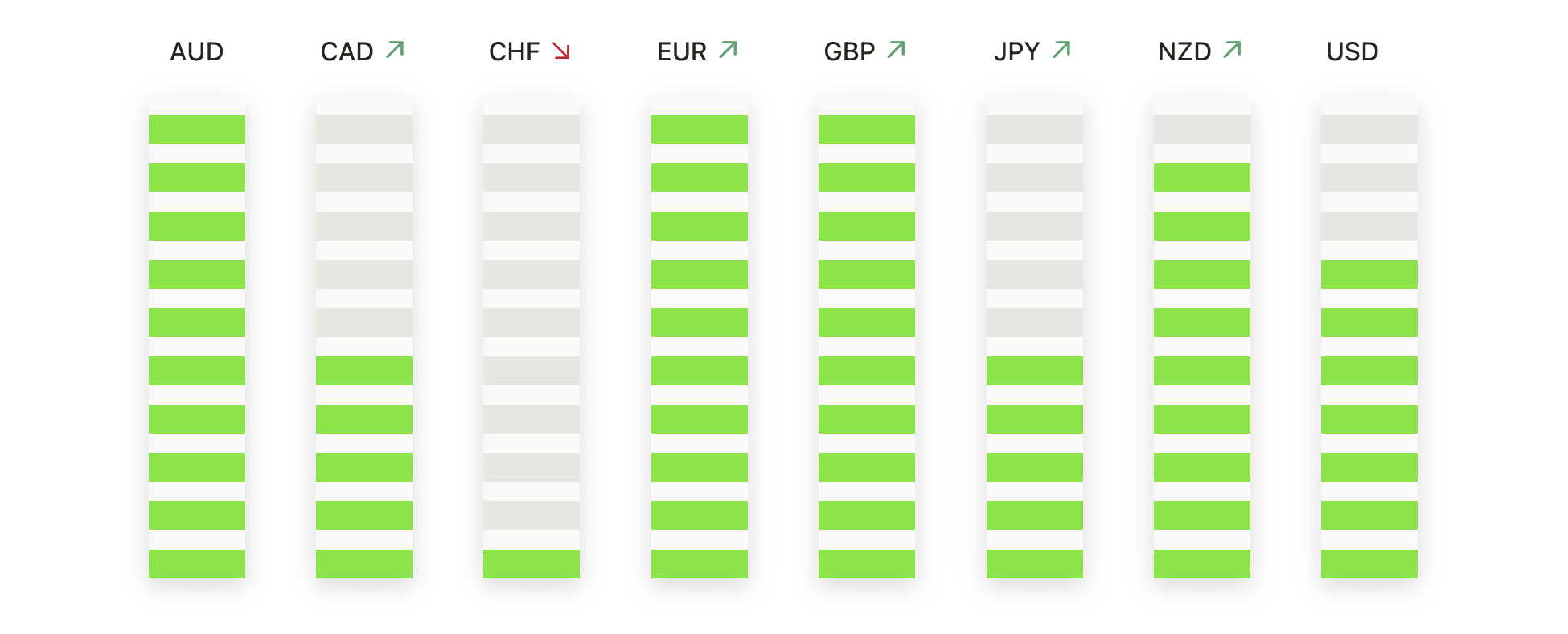

- EUR/USD Extends Uptrend Toward 1.1750: EUR/USD closed at 1.1737, rising 0.36% after trading between 1.1661 and 1.1746. The 50-day average at 1.1660 offers immediate support, while the 100-day at 1.1540 and the 200-day at 1.1089 confirm a firm long-term base. Structurally, the pair has held a sequence of higher supports since the early August rebound from 1.1500, underlining persistent demand on dips. Resistance remains concentrated just under 1.1750, and a clear break above this level would expose 1.1800 and potentially 1.1850. On the downside, support lies first at 1.1660 and then at 1.1600, with the broader bias staying constructive while those levels hold.

- GBP/USD Approaches Key 1.3600 Resistance: GBP/USD settled at 1.3578, gaining 0.35% after trading between 1.3494 and 1.3583. Buyers lifted the pair to the upper end of its recent range, leaving resistance just below 1.3600 as the key barrier to watch. The 50-day and 100-day averages near 1.3466–1.3467 continue to underpin the broader structure, alongside the 200-day at 1.3083. Since bottoming near 1.3300 in August, sterling has carved out higher lows, restoring bullish momentum. A close above 1.3600 would signal breakout potential toward 1.3700, while initial support sits around 1.3500 and stronger protection lies near 1.3460.

- AUD/USD Builds Momentum After Clearing 0.6600: AUD/USD finished at 0.6663, advancing 0.75% after ranging between 0.6586 and 0.6665. The 50-day average at 0.6521, the 100-day at 0.6495, and the 200-day at 0.6389 combine to provide a strong base, while the recovery from the August lows near 0.6400 has established a consistent pattern of higher lows and highs. Resistance at 0.6700 is now the immediate focus, with a decisive close above that level opening scope for 0.6750. On the downside, first support is at 0.6600, followed by 0.6550, with only a sustained move back under 0.6500 threatening the bullish outlook.

- Silver Climbs Toward $42.00 After Fresh Record Close: Silver ended at $41.61, up 1.18% after trading between $40.90 and $41.76. Rising averages underpin the trend, with the 50-day at $38.46, the 100-day at $36.31, and the 200-day at $33.90 confirming a robust long-term structure. The breakout beyond the August peak has accelerated momentum, with support now consolidating around $41.00. Immediate focus is on a decisive push through $42.00, which would pave the way toward $43.00. On the downside, a move back under $41.00 could trigger retracement toward $40.20, though the broader picture remains firmly bullish while $39.50 holds.

- Gold Consolidates Below $3,650 After Record Surge: Gold settled at $3,637, easing 0.11% after ranging between $3,613 and $3,649. Despite the minor dip, the metal held firm near record highs following the sharp rally earlier in the week. The 50-day average at $3,392 continues to rise steeply, supported by the 100-day at $3,358 and the 200-day at $3,100, anchoring the long-term uptrend. Structurally, a strong base has formed around $3,550, leaving the bias clearly tilted higher. Immediate focus is on a sustained break through $3,650, which would confirm upside continuation toward $3,700. On the downside, initial support lies at $3,600, with deeper retracement only considered if price falls beneath $3,550.

Market Movers:

- Micron Leads Chip Stocks Higher on Target Boost: Micron Technology surged more than 7% after Citigroup raised its price target to $175 from $150, lifting peers Lam Research and Applied Materials, which gained over 7% and 4% respectively, while ASML, ARM, and Qualcomm also advanced.

- Homebuilders Rally as Falling Yields Ease Mortgage Pressure: Shares of Builders FirstSource rose more than 4% alongside gains of over 2% in PulteGroup, Lennar and Toll Brothers as the drop in the 10-year Treasury yield signalled lower borrowing costs for housing demand.

- Warner Bros Discovery Soars on Takeover Speculation: Warner Bros Discovery jumped more than 28% on reports that Paramount Skydance is preparing a bid for the company, fuelling a surge in takeover-driven trading.

- Red Cat Holdings Jumps After NATO Approval: Shares in the drone maker climbed more than 30% after its Black Widow system was approved and added to the NATO Support and Procurement Agency catalogue.

- Oxford Industries Rallies on Earnings Beat: The stock gained more than 26% after reporting adjusted Q2 EPS of $1.26, topping consensus expectations of $1.18.

- Revolution Medicines Climbs on Trial Results: Shares advanced more than 13% after the firm released encouraging initial results from a Phase 1 trial of daraxonrasib for pancreatic cancer.

- Netflix Weakens on Executive Departure: Netflix shed more than 3% after Chief Product Officer Kim announced she would leave the company, pressuring sentiment in the streaming giant.

Wall Street’s latest rally underscored how investors remain firmly positioned for policy easing, even with consumer prices showing renewed monthly strength. Softer jobless data and sliding Treasury yields reinforced the case for a September rate cut, with markets confident the Federal Reserve will deliver at least a quarter-point move. European and Asian markets mirrored the optimism, with record highs in Japan and South Korea highlighting the global breadth of momentum. Commodities presented a mixed picture, with oil weighed down by oversupply while precious metals consolidated at record territory, leaving investors focused on whether the coming Fed meeting can validate expectations and sustain the advance in risk assets.