US equity markets closed mixed on Friday as a slightly softer-than-expected inflation report failed to ignite a sustained risk rally, while ongoing concerns around artificial intelligence disruption continued to weigh on sentiment. The S&P 500 finished marginally higher but still notched a second consecutive weekly decline, as investors balanced easing price pressures against widening sector divergence and persistent volatility across growth-linked names.

Key Takeaways:

- Dow Posts Modest Gain While Broader Markets Struggle: The Dow Jones Industrial Average added 48.95 points, or 0.10%, to settle at 49,500.93, showing relative resilience despite broader market caution. The index benefited from rotation into select defensive and value-oriented names, even as investor appetite for risk remained fragile following a volatile week dominated by AI-related concerns.

- S&P 500 Closes Flat and Extends Losing Streak: The S&P 500 edged up just 0.05% to 6,836.17, effectively ending the session flat and marking a weekly decline of 1.4%. The benchmark struggled to build momentum despite supportive inflation data, underscoring how sector-specific fears and uneven participation are limiting upside follow-through.

- Nasdaq Underperforms as Growth Names Stay Under Pressure: The Nasdaq Composite fell 0.22% to close at 22,546.67, capping a 2.1% weekly loss. Continued selling across software, financial technology, and select consumer-facing platforms highlighted investor unease around earnings sustainability and structural disruption tied to artificial intelligence adoption.

- Europe Markets Close Mixed as Data Offsets AI Fears: European equities ended Friday with mixed performances following another AI-driven sell-off in the US The Stoxx 600 closed below the flatline, while the FTSE 100 rose 0.30% to 10,434, supported by defensive sectors. France’s CAC 40 slipped 0.31% to 8,315, and Italy’s FTSE MIB dropped 1.62% to 45,473. Germany’s DAX advanced roughly 0.3% to 24,915, snapping a three-day losing streak, while Switzerland’s SMI gained 0.52% to 13,600.67. Macro data showed the Eurozone economy expanding 0.3% in Q4, with annual growth at 1.4%, above expectations. Employment rose 0.2% quarter-on-quarter, marking a 19th straight period of job growth, though Germany continued to lag. Inflation data remained benign, with Spain’s harmonised inflation easing to 2.4% and Swiss inflation holding at 0.1%, reinforcing expectations for a cautious policy stance.

- Asia Markets Track Wall Street Losses: Asia-Pacific equities traded lower, following declines in US markets as AI disruption fears hit technology-heavy sectors. Japan’s Nikkei 225 fell 1.21% to 56,941.97, while the Topix lost 1.63%. South Korea’s Kospi slipped 0.28%, ending a four-day winning streak, and the Kosdaq fell 1.77%. In China, the CSI 300 dropped 1.25%, and Hong Kong’s Hang Seng Index slid 1.71%, though select AI-related names extended sharp gains. Australia’s ASX 200 fell 1.39%, and New Zealand’s NZX 50 retreated 2.5%, reversing recent strength.

- Oil Prices Steady but Weekly Losses Persist: Oil markets stabilised after recent volatility, with Brent crude settling up 0.34% at $67.75 a barrel and WTI rising 0.08% to $62.89. Both benchmarks still posted weekly declines after sharp losses earlier in the week, as investors weighed easing US inflation against potential OPEC+ supply increases from April.

- Treasury Yields Slide on Softer CPI: US Treasury yields moved lower following the January CPI release. The 10-year yield fell more than 5 basis points to 4.05%, the 30-year slipped to 4.695%, and the 2-year dropped to 3.406%, reflecting modestly increased expectations for interest rate cuts later in the year.

- US Inflation Cools More Than Expected: Headline consumer prices rose 2.4% year-on-year in January, down from 2.7% in December and below expectations. Core inflation eased to 2.5%, its lowest level since March 2021, supported by slower housing cost growth and cheaper petrol prices. The data reinforced the view that disinflation remains intact, though policymakers remain cautious.

FX Today:

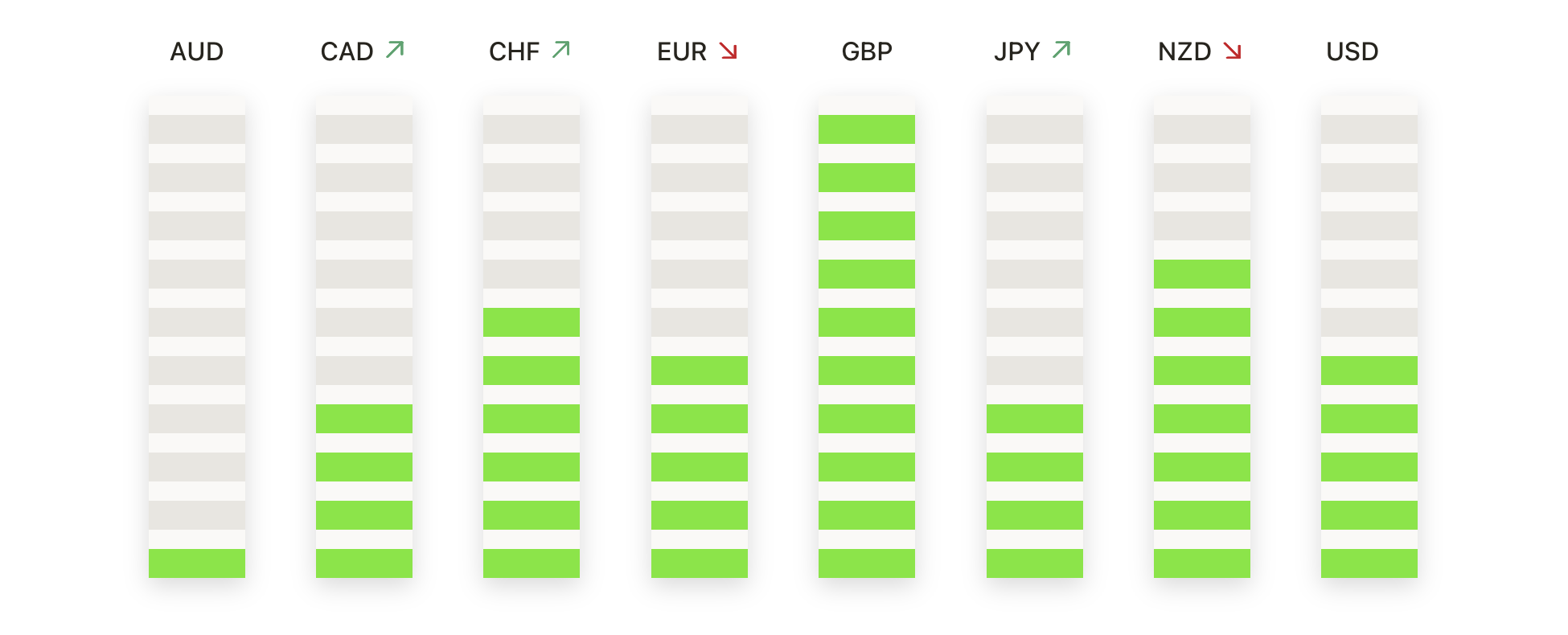

- EUR/USD Stabilises Above Key Support After Rally Pause: EUR/USD ended the session at 1.1874, edging 0.03% higher after moving within a narrow intraday range between 1.1874 and 1.1885. The subdued range resulted in a compact candle, reflecting a pause in momentum following the strong upward drive seen in recent sessions. The pair continues to trade well above its 50-day, 100-day, and 200-day simple moving averages at 1.1756, 1.1684, and 1.1632, which remain positively aligned and underline the prevailing bullish trend. The failure to extend beyond the session high suggests short-term supply emerging near recent highs, though downside pressure remains limited. The 1.1800 psychological level continues to act as an important structural support following the recent breakout. A sustained move above 1.1885 would reopen the path toward the 1.2000 region, while a close below 1.1874 would shift focus toward a corrective pullback in the direction of the 50-day SMA.

- GBP/USD Holds Firm Near Upper Range Boundary: GBP/USD closed at 1.3655, advancing 0.24% after trading between a low of 1.3591 and a high of 1.3659. The session saw buyers regain control after early volatility, allowing the pair to finish close to the top of its daily range. Price action remains constructive, with the pair holding above its 50-day and 100-day simple moving averages at 1.3508 and 1.3388, while the 200-day average at 1.3427 also remains supportive. The broader structure continues to reflect consolidation following the sharp rally in late January rather than a reversal. Immediate resistance is defined at 1.3659, with the early-February peak near 1.3800 beyond. Support is located at 1.3591, followed by the 50-day SMA, with the outlook remaining positive as long as these levels are defended.

- AUD/USD Pulls Back While Broader Uptrend Persists: AUD/USD closed at 0.7047, down 0.21%, after retreating from an intraday high of 0.7097 to a low of 0.7043. The pullback followed an earlier attempt to extend gains, leaving the pair near the lower end of its daily range by the close. Despite the decline, AUD/USD remains firmly above its 50-day, 100-day, and 200-day simple moving averages at 0.6788, 0.6659, and 0.6586, all of which continue to slope higher and confirm the dominant bullish structure. The broader trend remains defined by higher highs and higher lows following the multi-week rally. Resistance remains in place at 0.7097, with the recent peak near 0.7150 beyond, while support is seen at 0.7043 and then around the prior swing area near 0.6900. The outlook remains constructive provided price holds above these support levels.

- Gold Consolidates Above Rising Averages After Rebound: Gold settled at $5,029, gaining 2.21% after trading between a low of $4,887 and a high of $5,046. Strong buying interest emerged from the session low, lifting price back toward the upper end of its recent range, though momentum slowed as resistance was approached. The metal continues to trade well above its 50-day, 100-day, and 200-day simple moving averages at $4,617, $4,329, and $3,855, reinforcing the longer-term bullish trend. Recent price action suggests consolidation following the sharp pullback from early-February highs rather than a breakdown in structure. Resistance is located at $5,046, with the record high near $5,400 beyond, while support remains defined at $4,887 and then near the $4,700 region. Holding above support keeps the broader outlook positive.

- Silver Rebounds From Lows but Faces Heavy Resistance: Silver closed at $76.90, rising 2.23% after trading between a session low of $74.01 and a high of $79.33. Buyers stepped in aggressively following the recent correction, driving a sharp rebound from intraday lows, though price struggled to hold gains near the upper end of the range. Silver remains below its 50-day simple moving average at $79.08, while continuing to trade comfortably above the 100-day and 200-day averages at $64.41 and $50.69, preserving longer-term support. The rebound has improved near-term momentum, but overhead resistance remains significant. Immediate resistance is clustered around $79.08 and $79.33, while support is established at $74.01 and then near the structural base around $72.00.

Market Movers:

- DraftKings Slides on Weak Guidance: Shares fell about 13% after the company issued a disappointing 2026 revenue forecast despite beating Q4 earnings and revenue expectations.

- Ryan Specialty And Bio-Rad Sink On Earnings Misses: Ryan Specialty Holdings and Bio-Rad Laboratories both dropped more than 12% after reporting quarterly results below consensus estimates.

- Tri Pointe Homes And Rivian Surge: Tri Pointe Homes jumped over 26% following its acquisition by Sumitomo Forestry, while Rivian also surged more than 26% after beating revenue estimates and issuing stronger delivery guidance.

- Roku Rallies On Strong Outlook: Roku shares gained more than 8% after posting better-than-expected Q4 revenue and issuing an upbeat full-year forecast.

Markets closed the week grappling with a complex mix of easing inflation pressures and intensifying concerns around technological disruption. While the softer CPI print provided some reassurance on the inflation front, persistent AI-related uncertainty continues to drive sharp sector rotation and uneven performance across global equities. With major US indices now firmly in losing territory for the week, investor focus is likely to remain on whether disinflation trends can stabilise sentiment, or whether structural fears will continue to dominate near-term price action.