A steady risk tone carried US equities higher into the close, rounding off a strong week and month across major benchmarks. Gains were supported by renewed interest in large-cap growth and AI-linked names, while market breadth held firm and sector rotation remained orderly. Europe was more subdued as investors assessed inflation data and earnings, while Asia delivered a divided picture, with strength in Japan and South Korea contrasting with ongoing weakness across China.

Key Takeaways:

- Dow Inches Higher into Month End: The Dow added 40.75 points or 0.09% to 47,562.87 on Friday, capping a weekly gain of 0.8%. For October the blue-chip index rose 2.5%, its sixth straight positive month and the longest winning run since 2018, as investors balanced tech leadership with broader rotation.

- S&P 500 Extends Weekly Advance: The S&P 500 rose 0.26% to 6,840.20, up 0.7% on the week and 2.3% for October. Gains were paced by large-cap growth and AI beneficiaries, with defensives and select financials supporting breadth as investors leaned into earnings resilience and capex-driven AI demand.

- Nasdaq Outperforms on Amazon Surge: The Nasdaq Composite gained 0.61% to 23,724.96, up 2.2% on the week as Amazon rallied 9.6% on faster AWS growth and upbeat AI commentary. Netflix rose 2.7% after a 10-for-1 split announcement, and Tesla advanced 3.7%, helping cement the tech-led tone into month end.

- Europe Slips as Inflation Moderates and Earnings Shape Sentiment: European equities ended the session lower, with the Stoxx 600 down 0.5% as investors weighed a mix of softer inflation data and varied corporate earnings. The FTSE 100 outperformed on a monthly basis, rising 3.92% to 9,717.25, while Germany’s DAX fell 0.72% and France’s CAC dipped 0.53%. Eurozone headline inflation eased to 2.1% in October from 2.2%, while core held steady at 2.4% as services inflation remained firm at 3.4% and energy remained in decline. Country-level inflation diverged, led by Estonia at 4.5% and Cyprus at just 0.3%. Eurozone Q3 GDP grew 0.2% q/q, slightly above expectations and suggesting resilience despite weak manufacturing. The ECB left its deposit facility rate unchanged at 2% for the third consecutive meeting, reinforcing a wait-and-watch stance while earnings continued to drive individual stock moves.

- Asia Mixed as Japan and South Korea Rally While China Softens: Asian markets delivered contrasting performances. Japan’s Nikkei 225 climbed over 2% to a fresh record of 52,411.34 and the Topix also advanced, supported by easing geopolitical tensions following a US–China trade truce. South Korea’s Kospi and Kosdaq extended gains to 4,107.5 and 900.42 respectively, lifted by major AI infrastructure investment plans involving Nvidia, which boosted names such as Naver and Hyundai. Australia’s ASX 200 finished flat at 8,881.9. In contrast, Hong Kong’s Hang Seng fell 1.43% to 25,906.65 and China’s CSI 300 slid 1.47% to 4,640.67, pressured by an October manufacturing PMI of 49, the weakest since May and underscoring ongoing pressure from weak global demand and renewed trade uncertainty.

- Oil Whipsaws and Heads for a Monthly Decline: Oil prices fluctuated during the session, initially firming on reports of possible US air strikes on Venezuela before reversing after a White House denial. Brent closed around $65.06, up roughly 0.1% on the day, while WTI settled near $60.87, up around 0.5%. A stronger US dollar and expectations of softer Saudi pricing for December shipments weighed on sentiment, alongside steady OPEC+ export levels. Despite the intraday volatility, both benchmarks are set to finish October lower, with Brent on track for a decline of about 2.9% and WTI down around 2.3%, reflecting persistent questions over demand resilience.

- Yields Hold after Fed Cut and Cautious Tone: The 10-year US Treasury yield hovered around 4.093% after touching 4.10%, the 2-year stood near 3.596% and the 30-year around 4.665%. The Fed trimmed rates by 25 bps to 3.75%–4.00% but warned a December cut is “far from” assured; one dissent cited easy financial conditions.

FX Today:

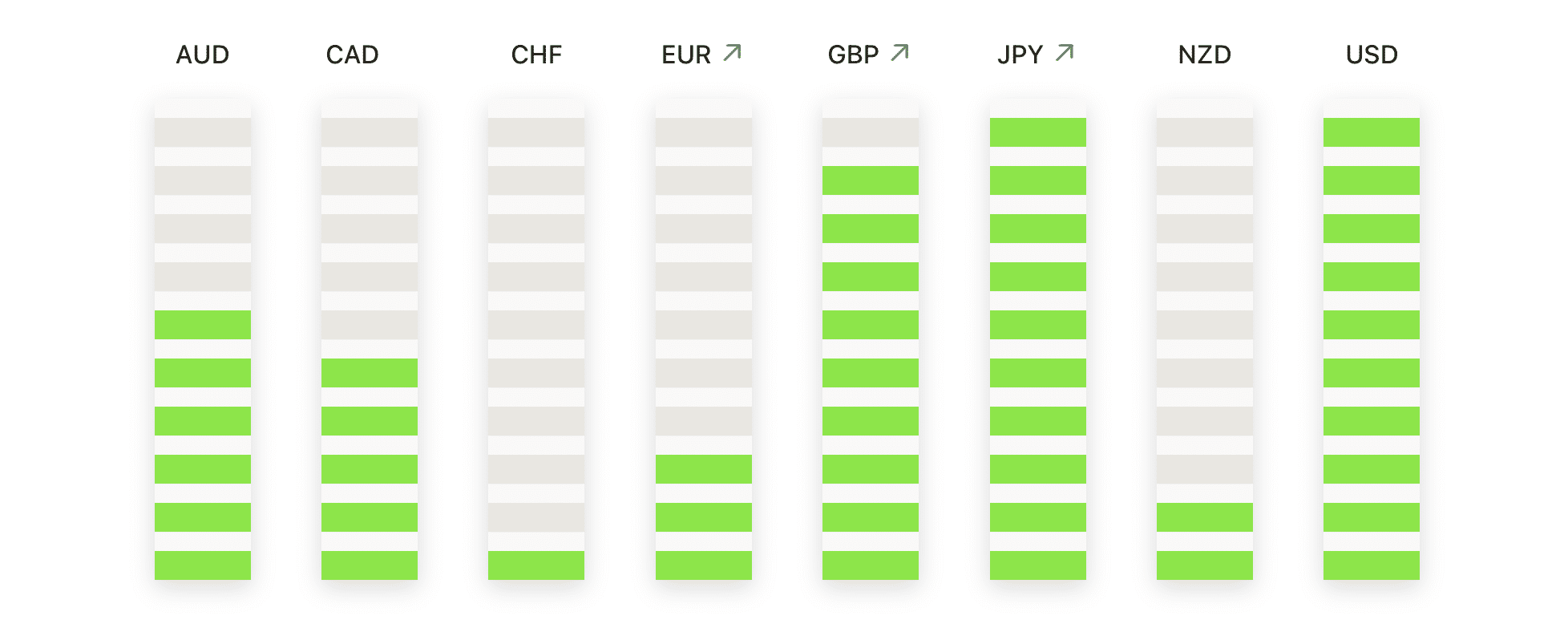

- EUR/USD Extends Decline Below Former Support: EUR/USD closed at 1.1537, down 0.24%, after trading between 1.1578 and 1.1522. The pair continues to trade below the former 1.1600 support level and below both the 50-day moving average at 1.1682 and the 100-day at 1.1665, which have recently crossed lower, confirming a shift in momentum to the downside. Immediate resistance remains at 1.1578 and 1.1600, while support sits at 1.1522 and then the more defined psychological level at 1.1500. The near-term directional bias stays negative unless the pair can regain and hold above the 1.1600 region.

- GBP/USD Consolidates Just Above Recent Lows: GBP/USD ended the session unchanged at 1.3151 after trading between 1.3165 and 1.3097. The pair remains weighed down below the 50-day moving average at 1.3434, the 100-day at 1.3464, and the 200-day at 1.3249, keeping the near-term bias tilted to the downside. The 1.3097 level provides initial support, followed by the key psychological 1.3000 level, while resistance is seen at 1.3165 and then the 200-day average at 1.3249. A stabilisation phase may emerge while price holds above 1.3097, though sustained recovery attempts are likely to be capped unless the pair reclaims ground above the major averages.

- USD/JPY Steadies Near Multi-Year Highs: USD/JPY closed at 154.00, down 0.07%, after trading between 154.42 and 153.85. The pair remains positioned near multi-year highs and well above the 50-day moving average at 149.45, the 100-day at 148.12, and the 200-day at 147.73, reinforcing a strong underlying uptrend. The 155.00 level remains a notable psychological resistance threshold, while initial resistance sits at 154.42 and near-term support lies at 153.85, followed by 152.00 on a deeper pullback. The broader backdrop continues to favour upside as long as the pair holds above 153.85.

- USD/CHF Maintains Rebound Above Key Averages: USD/CHF finished at 0.8041, up 0.33%, after trading between 0.8052 and 0.8007. The pair has regained both the 50-day moving average at 0.7974 and the 100-day at 0.8003, signalling improving near-term momentum despite the longer-term downtrend defined by the descending 200-day average at 0.8296. Resistance stands at 0.8052, followed by the 0.8100–0.8150 region, while support is now clustered around 0.8007/0.8003 and then the 50-day level below. Sustained closes above 0.8003 would reinforce the stabilisation phase and support a continued recovery bias.

- EUR/GBP Pulls Back but Retains Upward Bias: EUR/GBP slipped 0.22% to 0.8773 after trading between 0.8818 and 0.8771. The broader trend remains constructive, with the pair trading above the 50-day moving average at 0.8693, the 100-day at 0.8661, and the 200-day at 0.8537, while the 0.8700 level continues to act as a key support base. Resistance is located at 0.8818 and then 0.8850, while support rests at 0.8771 ahead of the 50-day average at 0.8693. Dips are still likely to draw demand while the upward trend structure remains intact.

- Gold Holds Above the $4,000 Threshold: Gold closed at $4,002, down 0.57%, after trading between $4,046 and $3,973. The metal continues to sit comfortably above the 50-day moving average at $3,818, the 100-day at $3,584, and the 200-day at $3,333, maintaining a firmly upward longer-term trend. The $4,000 mark remains a key psychological and technical level, having seen repeated tests as both support and resistance in recent sessions. Immediate support is located at $3,973 and then the more meaningful zone near $3,900, while resistance is seen at $4,046 and the $4,100 region. As long as gold holds above the $4,000 handle, buyers are likely to remain in control, keeping the broader bullish bias intact.

Market Movers:

- Amazon Jumps on AWS Acceleration and Strong Guide: Shares rose over 9% after Q3 net sales of $180.17bn beat $177.82bn consensus and Q4 guidance of $206bn–$213bn topped the midpoint of expectations, with AI demand lifting sentiment.

- Brighthouse Financial Soars on M&A Talk: The stock rallied more than 25% after reports that Aquarian Holdings is in advanced talks to acquire the company, prompting a sharp re-rating.

- Twilio Rallies on Revenue Outlook: Shares gained over 20% as Q4 revenue guidance of $1.31bn–$1.32bn topped the $1.29bn consensus, easing demand concerns.

- Cloudflare Pops after Raising Full-Year Sales: The company advanced more than 14% after lifting revenue guidance to $2.14bn from $2.11bn–$2.12bn, ahead of the $2.12bn consensus.

- Western Digital Advances on Beat: The stock climbed over 8% after Q1 net revenue of $2.82bn topped $2.73bn estimates, aided by storage pricing and AI-linked demand.

- Reddit Gains on User Growth: Shares rose more than 8% after reporting 116m daily active users in Q3 versus 114.16m expected, bolstering monetisation prospects.

- Coinbase Rises on Revenue Beat: The stock added over 5% as total Q3 revenue printed $1.87bn versus $1.80bn expected, with higher volumes and staking income helping.

- GoDaddy Climbs on Strong Print and Raise: Shares were up more than 5% after Q3 revenue of $1.30bn beat $1.23bn and full-year guidance increased to $4.93bn–$4.95bn.

- Dexcom Slides on Margin Cut: The stock fell over 14% after trimming full-year adjusted gross margin guidance to 61% from 62%, below the 61.8% consensus.

US equities finished the month on a constructive footing, supported by firm demand for growth sectors and resilient earnings momentum. While Europe contended with mixed corporate results and Asia presented a split landscape, broader sentiment remained stable and yields held steady following the Federal Reserve’s latest policy move.