A cautious mood settled over markets on Friday as another wave of pressure on artificial intelligence stocks pulled the Nasdaq lower and left technology investors reassessing the strength of the recent rally. While the S&P 500 and Dow managed to claw their way back into positive territory by the close, the sense of unease was clear, shaped by fading consumer confidence and a continued lack of economic visibility amid the government shutdown. A late-day proposal in Washington offered a possible path toward reopening federal agencies, but with negotiations still uncertain and key labour data unavailable for a second month, traders were left navigating without their usual guideposts.

Key Takeaways:

- Dow Edges Modestly Higher: The Dow Jones Industrial Average rose 74.80 points, or 0.16%, to 46,987.10 after being down more than 400 points earlier in the session before dip-buying and selective rotation supported a late recovery.

- S&P 500 Closes Slightly in the Green: The S&P 500 gained 0.13% to finish at 6,728.80, recovering from earlier weakness driven by pressure in large-cap technology. Defensive and value-oriented sectors provided stability, helping the benchmark avoid a broader decline.

- Nasdaq Posts Its Worst Week Since April: The Nasdaq Composite slipped 0.21% on the day to 23,004.54 and fell more than 3% over the week, marking its steepest weekly drop since early April. AI-linked names continued to face valuation scrutiny.

- Europe Ends Lower as AI Valuation Concerns Pressure Sentiment: European equities extended losses on Friday, with the Stoxx 600 closing 0.6% lower and all major bourses finishing the week in negative territory amid continued caution around artificial intelligence-related valuations. The FTSE 100 slipped 0.36% this week to 9,682.57, while France’s CAC dipped 0.2% and Germany’s DAX fell 0.78%, reflecting broader downside across the region. Rightmove plunged 12.5% after cautioning that heavy investment in AI would weigh on operating profits, prompting analysts to warn that the company’s strategic pivot raises near-term uncertainty. By contrast, ITV surged 16.6% after confirming discussions with Comcast over a potential £1.6 billion sale of its television business. German exports rose 1.4% in September, beating forecasts, while UK house prices increased 0.6% month-on-month to a record £299,862 ahead of the upcoming budget. Swiss and French reserve data pointed to differing policy positioning heading into year-end.

- Asia-Pacific Markets Track US Tech Weakness: Asia-Pacific equities declined on Friday, mirroring renewed selling pressure in US AI and semiconductor names. Japan’s Nikkei 225 fell 1.19%, led by weakness in major technology names, with SoftBank falling 6.87%, Advantest losing 5.54%, Renesas Electronics declining 3.75%, and Tokyo Electron slipping 1.35%. The Topix index ended near 3,298.85. South Korea’s Kospi dropped 1.81% and the Kosdaq lost 2.38%, as Samsung Electronics and SK Hynix both weakened. Hong Kong’s Hang Seng declined 0.92%, while China’s CSI 300 eased 0.31% after October exports unexpectedly fell 1.1% year-on-year, highlighting ongoing strain from weak domestic demand amid a prolonged property downturn. Australia’s S&P/ASX 200 slipped 0.66%, while India’s Nifty 50 edged 0.11% higher even as Bharti Airtel came under pressure following Singtel’s SG$1.5 billion stake sale.

- Oil Records a Second Weekly Decline: Brent crude rose 0.54% to $63.72 a barrel and WTI gained 0.71% to $59.85, though both fell around 2% over the week. Concerns over rising global supply and slowing US demand were reinforced by a 5.2 million-barrel inventory build.

- Treasury Yields Little Changed Amid Data Blackout: The 10-year yield held at 4.093%, the 2-year eased to 3.557%, and the 30-year edged higher to 4.697%. With the government shutdown halting official releases, markets continued to navigate without key labour and inflation data.

FX Today:

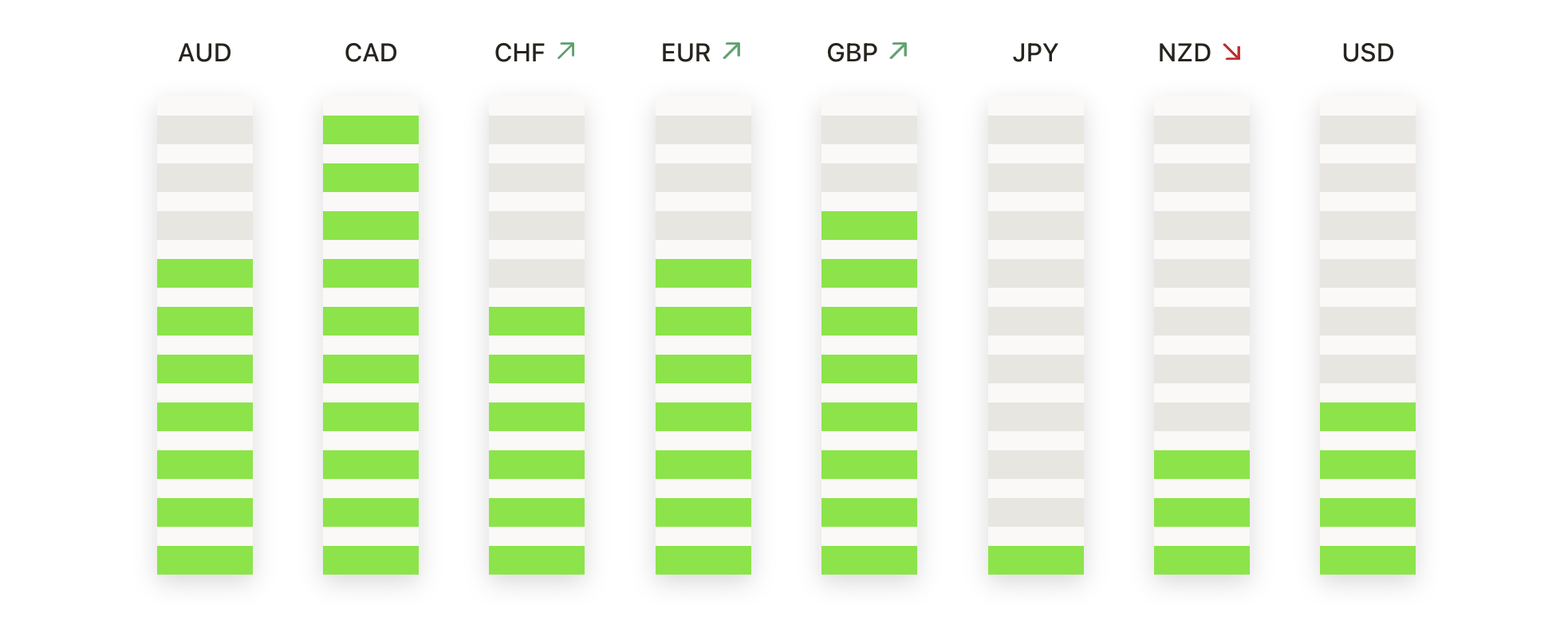

- EUR/USD Finds Support but Faces Heavy Resistance Ahead: EUR/USD closed at 1.1565 after trading between 1.1591 and 1.1529, with buyers stepping in at lower levels to steady the recent recovery attempt. Despite the bounce, the pair continues to trade beneath the 50-day and 100-day moving averages at 1.1666 and 1.1685, which together form a notable resistance zone that has contained upside momentum. The broader structure of higher lows since March 2025 remains intact, suggesting the longer-term trend still leans constructive, though near-term progress may be limited without a break above these moving averages. Initial resistance lies at 1.1591, while support is located at 1.1529 and then 1.1480.

- GBP/USD Attempts Stabilisation After Recent Selling: GBP/USD closed at 1.3163 after trading between 1.3175 and 1.3095, showing signs of stabilisation following a persistent decline over recent weeks. The pair still trades below the 50-day, 100-day and 200-day moving averages at 1.3395, 1.3446 and 1.3265 respectively, which continue to weigh on attempts to rebuild upside momentum. Buyers defended the 1.3095 level, establishing it as initial support for now, while resistance emerges at 1.3175 and more significantly near the 200-day moving average. A sustained move above 1.3175 would suggest scope for a broader corrective recovery, whereas a break back below 1.3095 would refocus attention on the 1.3000 psychological level.

- USD/CAD Pulls Back After Rejection Near Range Highs: USD/CAD closed at 1.4030 after trading between 1.4130 and 1.4030, with the pair rejecting gains near the upper boundary of its recent range. The 200-day moving average at 1.3997 acted as a key pivot during the session, with the close back below it signalling easing upside momentum. Resistance remains firm at 1.4130, which capped advances throughout the day. Initial support is now seen at 1.4030, followed by the 50-day moving average at 1.3929 if downside pressures deepen. A sustained break below the 200-day moving average would reinforce a shift in near-term bias back toward the lower end of the multi-month range.

- AUD/USD Holds Key Long-Term Support but Upside Still Limited: AUD/USD closed at 0.6498 after trading between 0.6498 and 0.6467, with support emerging above the 200-day moving average at 0.6448. While the pair has steadied, it continues to trade below the 50-day and 100-day moving averages at 0.6559 and 0.6537 respectively, which together form a notable resistance zone. Short-term momentum remains cautious following the decline from the October highs, and the pair will likely require a break above the cluster of moving averages to build a more meaningful recovery. Immediate support lies at 0.6467 and then the 200-day moving average. A daily close below 0.6448 would signal renewed downside pressure.

- Silver Pauses as Market Consolidates Recent Moves: Silver closed at $48.38 after trading between $48.88 and $47.98, settling into a consolidation phase following recent volatility. The metal remains supported by the 50-day, 100-day and 200-day moving averages at $46.27, $41.94 and $37.41 respectively, highlighting a firmly constructive longer-term trend. Immediate resistance is located at $48.88, where recent attempts to firm have stalled. Initial support is seen at $47.98, with the 50-day moving average providing a more substantial downside buffer should selling pressure re-emerge. A close above $48.88 would open scope for a retest of prior highs.

- Gold Maintains Stability Above Psychological Support: Gold closed at $4005 after trading between $4027 and $3975, maintaining a firm footing above the $4,000 psychological level despite recent consolidation. The metal continues to trade comfortably above the rising 50-day, 100-day and 200-day moving averages at $3877, $3613 and $3364 respectively, confirming that the broader uptrend remains in place. Resistance sits at $4027, with a break above this level likely to attract renewed buying interest and refocus attention on the October highs. Initial support is found at $3975, while a close beneath this level would shift attention back toward the 50-day moving average.

Market Movers:

- Globus Medical Surges on Upgraded Outlook: Shares jumped more than 35% after Q3 net sales of $769 million topped expectations.

- Expedia Advances on Strong Earnings Beat: The stock rose over 17% after adjusted Q3 EPS of $7.57 exceeded consensus estimates of $6.83.

- Akamai Pushes Higher on Improved Revenue Forecast: Shares gained about 15% after the company guided Q4 revenue to $1.07 billion–$1.09 billion, above market expectations.

- Affirm Rallies on Higher GMV Targets: Affirm climbed more than 11% after raising its 2026 gross merchandise volume forecast to above $47.5 billion from above $46 billion.

- Intellia Therapeutics Plunges on Clinical Trial Update: Shares dropped more than 25% after the company reported a patient death in its gene-editing therapy study.

- Universal Display Drops After Missing Revenue Expectations: Shares slid over 8% after Q3 revenue of $139.6 million came in below the expected $166 million.

- Block Retreats on Revenue Miss: The stock declined more than 7% after Q3 net revenue of $6.11 billion fell short of the $6.34 billion estimate.

The week closed with market leadership narrowing and investors showing greater selectivity as the rally in AI-linked names continued to unwind. While value and defensive pockets helped offset pressure in technology, sentiment remains hesitant with key economic indicators still unavailable due to the government shutdown. Attention now shifts to whether negotiations in Washington can restore data visibility and whether upcoming corporate guidance can offer clearer direction on the health of demand. With confidence indicators weakening and sector performances diverging, markets enter the new week looking for catalysts capable of restoring momentum and broadening participation beyond a concentrated group of leaders.