US equities pulled back on Friday after weaker-than-expected labour market data reinforced the likelihood of a Federal Reserve rate cut but at the same time stirred fresh concern about economic momentum. The Dow led losses, shedding more than 220 points as banks and industrials fell on signs of slowing demand. All three major indices had earlier touched record intraday highs before retreating, reflecting the fragile balance between optimism for policy easing and anxiety that growth may be faltering. With unemployment at its highest level in nearly four years and job creation slowing to a crawl, investors are assessing whether the Fed’s expected intervention will be enough to steady sentiment.

Key Takeaways:

- Dow Slides After Jobs Report Weakness: The Dow Jones Industrial Average dropped 220.43 points, or 0.48%, to 45,400.86, with JPMorgan, Boeing and GE Aerospace leading declines. The index had briefly hit record intraday levels earlier but closed the week down 0.32%.

- S&P 500 and Nasdaq Ease From Records: The S&P 500 fell 0.32% to 6,481.50, while the Nasdaq Composite edged 0.03% lower to 21,700.39. Both benchmarks had posted fresh highs intraday before momentum faded, though they still ended the week higher, with the S&P 500 up 0.33% and the Nasdaq gaining 1.14%.

- Labour Market Stalls With Smallest Gain Since Pandemic: US nonfarm payrolls rose just 22,000 in August, well below forecasts of 75,000. Revisions showed June payrolls fell by 13,000, the first monthly job loss since December 2020, while July was revised up to 79,000. The unemployment rate rose to 4.3%, the highest since late 2021, underscoring labour market weakness.

- Europe Stocks Decline as German Orders Slide: The Stoxx 600 slipped 0.2% on Friday, with Frankfurt’s DAX down 0.73% and Milan’s FTSE MIB falling 0.91%. Paris’s CAC 40 also dropped 0.3%, while London’s FTSE 100 posted a weekly gain of 0.23% to 9,208.21, rising in 17 of the past 21 weeks. German industrial orders unexpectedly fell 2.9% in July, their third straight monthly drop, driven by weaker demand for aircraft, ships and trains. UK data showed house prices up 0.3% in August and retail sales up 0.6% in July, both stronger than expected.

- Asia-Pacific Markets Gain on Tariff and Wage Boost: Asia-Pacific equities advanced after President Trump cut Japanese auto tariffs from 27.5% to 15% and confirmed $550 billion in Japanese investments. Japan’s Nikkei 225 climbed 1.03% to 43,018.75 and the Topix gained 0.82%, supported by stronger household spending and the first rise in real wages since December. South Korea’s Kospi added 0.13% and Kosdaq 0.74%, while Australia’s ASX 200 rose 0.51%. Hong Kong’s Hang Seng jumped 1.41% and China’s CSI 300 surged over 2% after the central bank pledged a 1 trillion yuan liquidity injection.

- Oil Posts First Weekly Loss in Three Weeks: Brent crude fell 1.94% to $65.69 a barrel, while WTI dropped 2.30% to $62.02. Both benchmarks logged weekly declines, with Brent down nearly 4% and WTI more than 3%, as rising US inventories and expectations of an OPEC+ production boost weighed on prices. Reports suggested members may accelerate the unwinding of output cuts by 1.65 million barrels per day.

- Treasury Yields Drop to Multi-Month Lows: The 10-year Treasury yield fell over 8 basis points to 4.091%, its lowest since April, while the 2-year yield slid to 3.526% and the 30-year dropped to 4.769%. The sharp move reflected expectations of Fed easing after weak payrolls data, adding to the downward pressure from earlier soft private-sector jobs figures.

FX Today:

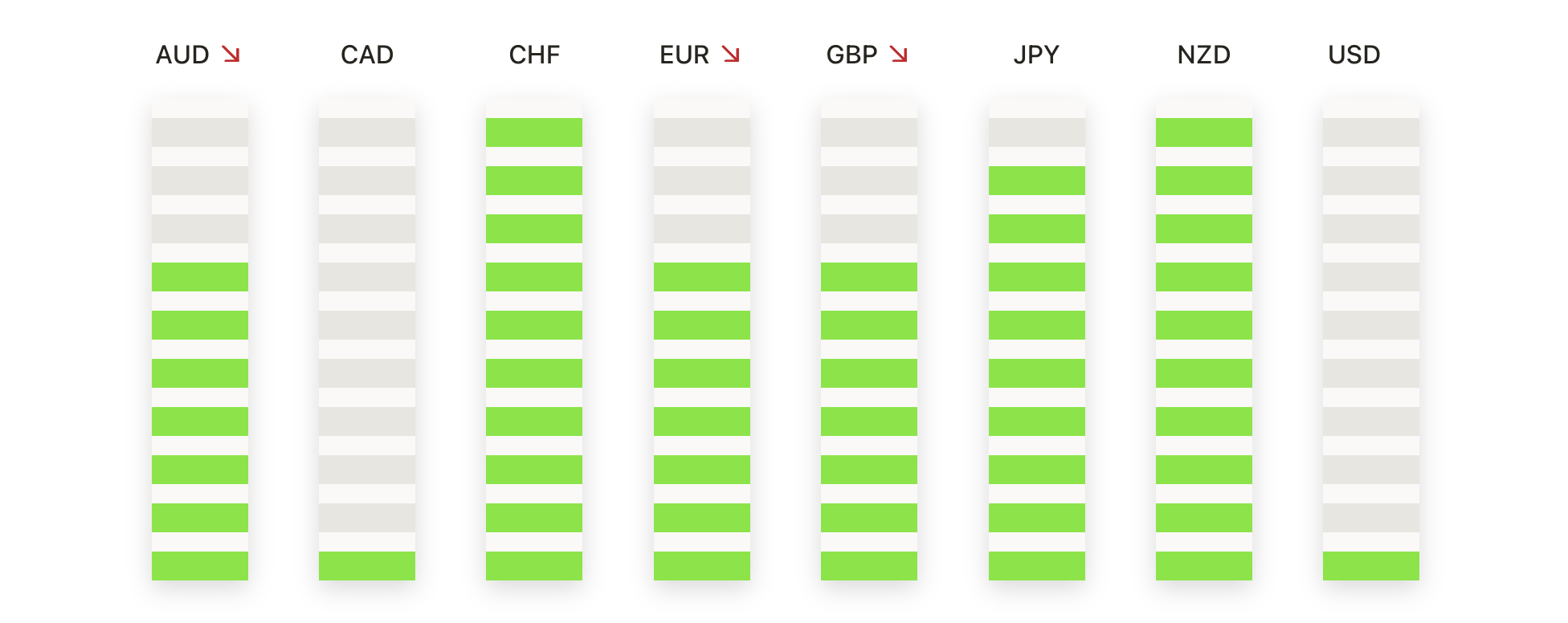

- EUR/USD Builds Momentum as Buyers Target 1.1800: EUR/USD closed at 1.1716, up 0.57% after trading between 1.1649 and 1.1759. The rebound carried price above the 50-day SMA at 1.1665 and kept it supported above the 100-day SMA at 1.1528 and the 200-day SMA at 1.1064. Although recent months brought a corrective phase from the July highs near 1.1850, buyers have consistently returned to defend the 1.1600 handle, showing that downside pressure remains limited. The consolidation through August formed a well-defined range, with sellers repeatedly unable to force a break under 1.1650 while upside progress stalled just below 1.1750. Resistance is set at 1.1750 and 1.1800, while support remains at 1.1665 and then 1.1600, levels that would need to fail to weaken the bullish outlook.

- GBP/USD Recovers as Sterling Reclaims 1.3500 Handle: GBP/USD settled at 1.3504, gaining 0.50% after swinging between 1.3430 and 1.3555. A bullish daily candle showed renewed demand, with the 200-day SMA at 1.3458 and the 50-day SMA at 1.3478 forming a reinforced support base that has repeatedly underpinned the broader trend. The pair has been oscillating between 1.3400 and 1.3600 for several weeks, with momentum shifting back toward buyers after a firm close near the highs of the session. Immediate resistance is marked at 1.3555 and 1.3600, where a breakout would open the way toward the July peak near 1.3800. Support remains at 1.3450 and 1.3400.

- USD/CHF Breaks Lower as Sellers Regain Control Below 0.8000: USD/CHF closed at 0.7985, down 0.88% after ranging between 0.8058 and 0.7959. The decisive break beneath the 0.8000 level produced a strong bearish candle that confirmed sellers are reasserting control. Price action remains well capped under the 50-, 100- and 200-day SMAs, keeping the broader trend negative and leaving little sign of recovery strength. Momentum has now shifted clearly back to the downside, with lower highs reinforcing persistent weakness. Resistance is set at 0.8050 and 0.8120, while support lies at 0.7950 and 0.7900, levels that could soon come into play if bearish pressure intensifies.

- USD/JPY Retreats After Sellers Reject 148.50 Test: USD/JPY ended at 147.48, down 0.68% after moving between 146.82 and 148.52. A firm bearish candle confirmed rejection at 148.50, dragging the pair back under the 50-day SMA at 147.27 and leaving buyers unable to establish control. The broader market remains caught in a wide range between the July high near 151.00 and the August low just below 146.00, with rallies repeatedly checked by overhead barriers. The 200-day SMA at 148.75 continues to act as a strong ceiling, preventing sustainable breaks higher, while the 100-day SMA at 145.79 provides an underlying layer of support. For now, bias has shifted lower, with immediate focus on 147.00 and 146.00. Resistance remains at 148.50 and 148.75, levels that must be cleared to restore upward momentum.

- AUD/USD Advances as Bulls Press Toward 0.6600: AUD/USD closed at 0.6553, up 0.54% after trading between 0.6511 and 0.6589, finishing near session highs. The advance allowed price to reclaim the 50-day SMA at 0.6519, with the 100-day SMA at 0.6486 and 200-day SMA at 0.6386 continuing to underpin the broader trend. The pair has been consolidating between 0.6450 and 0.6600 since July, with repeated failures to clear resistance at the top of the range. Momentum has now tilted back toward the upside, with resistance at 0.6590 and 0.6600 set to be retested. Support is found at 0.6520 and then 0.6485.

- Gold Extends Breakout as Bulls Drive Toward Fresh Highs: Gold settled at $3,592, rising 1.29% after swinging between $3,540 and $3,600. The session produced a tall bullish candle that extended the sharp breakout seen in recent sessions, with price now firmly above the 50-day SMA at $3,367 and the 100-day SMA at $3,343. Structurally, the move above $3,450 triggered a decisive acceleration, while repeated closes above $3,550 confirm renewed demand. The broader trend remains firmly bullish, with steepening moving averages reinforcing the upward trajectory. With price action now pressing into uncharted territory, there is little overhead supply to limit further advances. Resistance is seen at $3,600 and beyond, while support lies at $3,550 and then $3,500, levels that would need to give way before any meaningful pullback develops.

Market Movers:

- Broadcom Soars on AI Deal With OpenAI: Broadcom jumped 9.4% after strong quarterly results and a partnership to design a new AI chip, fuelling hopes it can challenge Nvidia.

- Nvidia Slips on Competition Concerns: Nvidia fell 2.7% as investors weighed Broadcom’s push into AI chips and the prospect of intensifying rivalry.

- Tesla Advances on Musk Pay Package: Tesla rose 3.6% after unveiling a pay deal for Elon Musk that could be worth up to $1 trillion if aggressive targets are met.

- Chip Complex Rallies Beyond Broadcom: Micron rose 5.8%, while ASML, KLA-Tencor and Align Technology gained more than 3% as semiconductor sentiment improved.

- Homebuilders Gain on Lower Yields: DR Horton, Lennar and PulteGroup climbed more than 2%, with Toll Brothers up 1.4% as falling Treasury yields eased mortgage-rate pressure.

- Palantir Extends Weak Patch: Palantir slipped about 2% amid ongoing pressure on AI-linked software names.

- Crypto Stocks Mixed as Bitcoin Rises: Bitcoin rose about 1%; Coinbase fell 2.5% while MicroStrategy gained 2.5%, with Riot Platforms and MARA Holdings up more than 0.5%.

- Megacaps Hit $21 Trillion Week Led by Google: A Google-led surge pushed the combined value of megacap tech to roughly $21 trillion over the week. Google rose over 1% on Friday.

Markets ended the week on a cautious note as a weak jobs report confirmed expectations for a Federal Reserve rate cut but also raised doubts about the strength of the economy. Technology shares showed resilience, but losses in banks, energy and consumer stocks left indices lower. Gold was a standout, reaching fresh all-time highs above $3,600, while Treasury yields fell to multi-month lows. Attention now turns to the Fed’s decision later this month as investors look for policy support to steady confidence.