Wall Street fell sharply on Friday as traders absorbed a wave of disappointing economic data and an escalation in trade tensions that jolted markets across the globe. A much weaker-than-expected US labour report reignited recession fears and sent rate-cut expectations surging, while President Trump’s rollout of higher tariffs on dozens of countries unnerved investors already bracing for seasonal volatility. Technology shares extended losses following downbeat earnings guidance from major firms, while financials retreated on concerns over slowing growth. The combined pressure left global indices deep in the red, with sentiment deteriorating across Europe and Asia as traders braced for more policy uncertainty and supply chain disruption.

Key Takeaways:

- Dow Suffers Steepest Drop Since June: The Dow Jones Industrial Average fell 542.40 points, or 1.23%, to 43,588.58 on Friday, marking its worst daily decline since mid-June and a weekly drop of 2.9%. Financial stocks dragged the index lower as slowing job growth and fresh tariff shocks stoked recession concerns.

- S&P 500 Tumbles as Market Breadth Weakens Further: The S&P 500 shed 1.60% to close at 6,238.01, posting its worst single-day performance since May 21 and a 2.4% weekly decline. Defensive positioning grew as traders rotated out of high-valuation sectors following weak economic data.

- Nasdaq Leads Weekly Decline as Amazon Sinks Over 8%: The Nasdaq Composite dropped 2.24% to 20,650.13 and lost 2.2% for the week, weighed down by a selloff in technology stocks. Amazon’s disappointing Q3 outlook triggered a sharp decline, while weakness in chipmakers including Marvell, Micron and Nvidia added to the pressure.

- European Markets Extend Declines Amid Tariff Shock and Mixed Data: Equity markets across Europe fell sharply as investors reacted to Washington’s sweeping new tariffs and a flurry of downbeat earnings. The Euro Stoxx Bank index tumbled 3.6%, logging its worst day since April, while industrial and tech shares also underperformed. France’s CAC 40 plunged 2.9% to a one-month low and fell 4.1% for the week. Germany’s DAX lost 2.66%, Milan’s FTSE MIB dropped 2.55%, and the FTSE 100 slipped 0.57%. Regional data was mixed, Eurozone inflation held steady at 2%, supporting a hold stance from the ECB, while French manufacturing orders declined sharply and UK factory activity remained in contraction despite improved sentiment. Switzerland was officially on holiday Friday for the country’s national day, but many market watchers were dragged back to their desks by news that the White House imposed a 39% US import tariff effective 7 August, one of the highest rates in the world.

- Asian Stocks Retreat as Revised Tariffs Raise Growth Concerns: Asian markets ended the week broadly lower as President Trump’s updated tariff schedule, ranging from 10% to 41%, %, raised fresh concerns about the impact on global trade. South Korea’s Kospi index slumped 3.88% and the Kosdaq plunged 4.03% amid uncertainty over trade talks. Japan’s Nikkei 225 lost 0.66%, while Hong Kong’s Hang Seng declined 1.07% and China’s CSI 300 shed 0.51%. Australia’s ASX 200 dropped 0.92% to 8,662.70, weighed down by energy and tech names, while India’s Nifty 50 and BSE Sensex fell 0.48% and 0.34% respectively. Traders noted limited progress in US trade deals with key economies like India, Canada and Brazil, while Taiwan and Switzerland were hit with aggressive new duties.

- Oil Drops Over 2% on OPEC+ Output Rumours and Risk Aversion: Oil prices tumbled Friday as talk of a possible OPEC+ production hike intersected with global demand concerns. Brent crude slid 2.83% to $69.67 a barrel, while US WTI dropped 2.79% to $67.33. Sources indicated OPEC and its allies may boost output by over 500,000 barrels per day in September.

- Yields Tumble as Jobs Data Miss Sparks Rate Cut Bets: US Treasury yields dropped after a weak July jobs report boosted expectations for a Fed rate cut. The 2-year yield plunged 28 basis points to 3.67%, while the 10-year fell 14 basis points to 4.21% and the 30-year eased to 4.809%. Political risk added to volatility after Fed Governor Kugler resigned and President Trump dismissed the head of the Bureau of Labour Statistics.

- US Job Growth and Manufacturing Weaken Further as Revisions Deepen: July nonfarm payrolls rose by just 73,000, far below the forecast of 100,000 and the weakest reading since 2020. The Bureau of Labour Statistics revised June’s total down to 14,000 from 147,000 and May’s figure to 19,000 from 125,000, slashing a combined 258,000 jobs from prior estimates. Manufacturing activity also weakened, with the ISM PMI falling to 48.0 in July from 49.0 in June, marking the fifth straight month of contraction. Factory employment dropped to its lowest level in five years, while the new orders index remained in negative territory for a sixth consecutive month at 47.1.

FX Today:

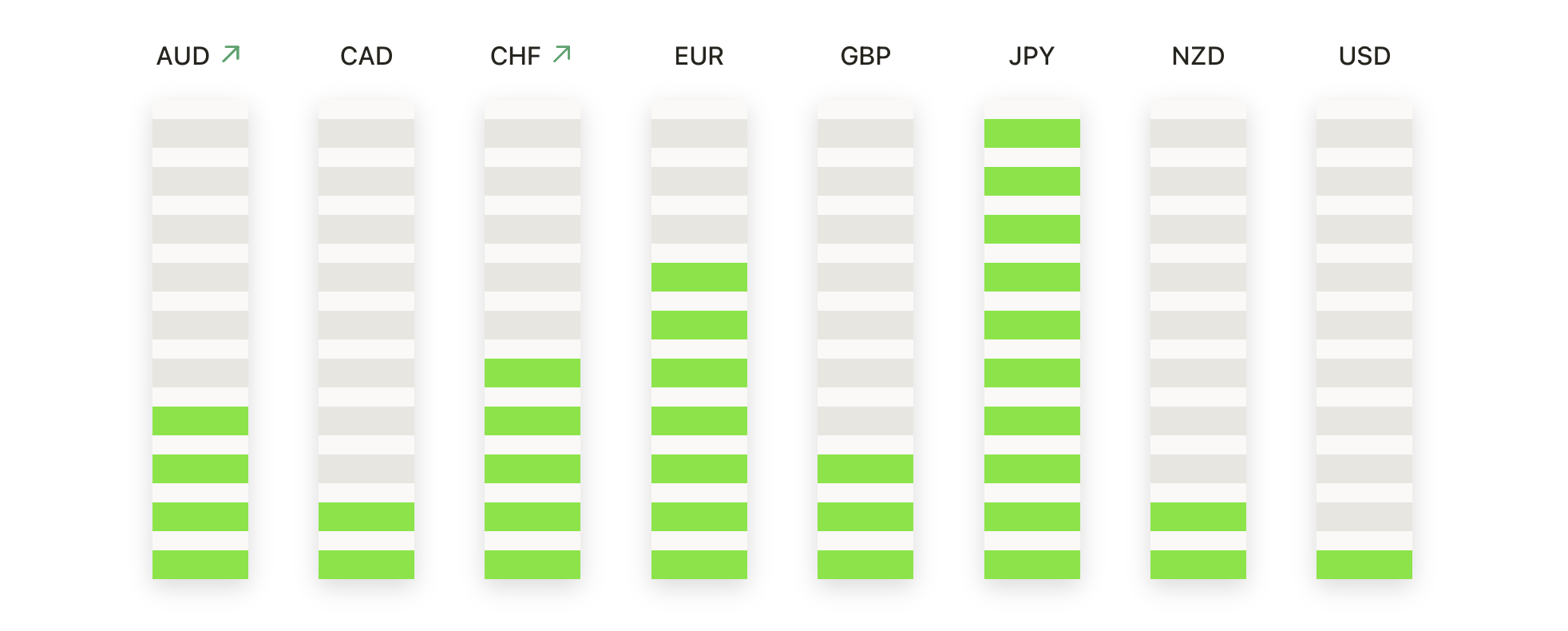

- EUR/USD Reclaims Support as Bullish Momentum Returns: EUR/USD surged 1.43% on Friday to settle at 1.1578, recovering strongly from a low of 1.1392 and closing near the session high of 1.1588. The move followed a sharp rebound off the 100-day moving average, with price reclaiming the 50-day average and invalidating the prior breakdown seen earlier in the week. The broader trend remains constructive, supported by upward-sloping major moving averages and a rising channel in place since March. With the pair closing firmly above the 1.1500 mark, short-term momentum has shifted back to the upside. Buyers now eye resistance at 1.1700, with scope to push towards 1.1800 if momentum persists. On the downside, support is seen at 1.1360 and 1.1310, with a break below those levels needed to reassert bearish pressure.

- GBP/USD Attempts Recovery But Remains Below Key Resistance: GBP/USD rose 0.49% to close at 1.3270, rebounding modestly from a low of 1.3142 after a sharp multi-session decline. The pair bounced from a key demand zone near 1.3100, but remains capped below the 100-day moving average at 1.3342, which continues to limit upside momentum. Although price has regained the 1.3200 handle, with lower highs and lower lows evident since mid-July. Buyers will need to push through the 1.3340–1.3400 region to neutralise bearish control and open the door toward 1.3500. Failure to do so may see renewed selling pressure, with downside levels at 1.3140 and the 200-day average at 1.2988 providing the next support.

- USD/CHF Slumps After Rejection From 50-Day Resistance: USD/CHF declined 0.93% on Friday to close at 0.8047, reversing sharply from a high of 0.8171 and ending near the session low of 0.8026. The pair was rejected from the 50-day moving average at 0.8072 early in the session, triggering a swift selloff that erased gains from earlier in the week. Friday’s reversal reinforces the role of former support as new resistance and suggests sellers remain in control. Key support sits at 0.7950, just above July’s low, while any attempt to rebound will need a sustained break above 0.8170 to ease downward pressure. Unless that occurs, downside risks persist, with 0.7900 the next likely target on a breakdown below 0.8000.

- USD/JPY Reverses Sharply From 200-Day Average: USD/JPY tumbled 2.22% to close at 147.38, retreating from an intraday high of 150.92 after failing to hold above the psychologically important 150.00 level. The pair was firmly rejected from the 200-day moving average near 149.50, marking the end of a brief rally and signalling a return of bearish momentum. The selloff cut through several short-term support zones, briefly dipping below the 100-day average at 145.71 before stabilising. Support is now seen at 145.70 and 144.00, while resistance remains capped at 149.50–151.00. If price fails to defend current levels, a deeper retracement could follow. A close back above 149.50 would be needed to reassert the longer-term uptrend.

- Gold Surges as Bulls Defend 100-Day Average and Retest Resistance: Gold rallied 2.13% to settle at $3,359 after rebounding from a low of $3,281 and closing near the session high of $3,361. Price reclaimed the 50-day moving average at $3,340 following a three-day pullback and successfully defended the 100-day average near $3,258. The bullish reversal preserved the broader uptrend and confirmed renewed demand at dynamic support, with buyers stepping in strongly near the previous swing low at $3,230. All major moving averages remain aligned upward, supporting continuation. Attention now turns to resistance at $3,420, which capped recent advances.

Market Movers:

- Fluor Drops as Outlook Slashed: Fluor Corporation tumbled over 27% after reporting weaker-than-expected Q2 earnings and cutting its full-year EPS forecast well below estimates.

- Eastman Chemical Plunges on EPS Miss: Eastman Chemical declined more than 19% after posting Q2 earnings of $1.60, missing forecasts and prompting concerns over margin pressure.

- Coinbase Falls as Revenue Disappoints: Coinbase dropped over 16% following Q2 revenue of $1.50 billion, missing consensus estimates of $1.59 billion.

- WW Grainger Sheds 10% on Earnings Cut: WW Grainger fell more than 10% after Q2 EPS came in at $9.97 and the company lowered its full-year profit guidance below prior projections.

- Moderna Declines After Revenue Forecast Narrows: Moderna lost over 6% after narrowing its full-year revenue range, with the midpoint falling below analyst expectations.

- Reddit Jumps on Strong Revenue: Reddit rose more than 17% after posting Q2 revenue of $499.6 million, well above forecasts, and projecting Q3 revenue of up to $545 million.

Markets began August under heavy pressure as investors responded to deepening concerns over economic growth, policy uncertainty and shifting trade dynamics. A sharply weaker US labour report and ongoing manufacturing weakness reignited fears of a slowdown while sweeping new tariffs from the White House added to global instability. Disappointing corporate guidance, particularly in technology, further weighed on sentiment and contributed to broad selling across regions and sectors.