US equities slipped on Tuesday as September began under pressure from renewed tariff disputes and a surge in bond yields, while gold surged to a fresh all-time high above $3,500. A federal appeals court struck down most of former President Trump’s global tariffs, raising the prospect that Washington may have to refund billions already collected, intensifying concerns about fiscal strains. At the same time, the 30-year Treasury yield climbed close to 5%, unsettling equity markets trading at elevated valuations. Investors also booked profits in major technology names after a strong summer, with the market now turning its focus toward Friday’s jobs report for clues on the Federal Reserve’s next policy steps.

Key Takeaways:

- Dow Falls as Yields and Tariff Risks Weigh: The Dow Jones Industrial Average dropped 0.55%, closing down 249 points to 45,295.81, after renewed trade uncertainty and surging Treasury yields unsettled blue chips. The decline marked a weak start to September, with fiscal concerns prompting rotation out of industrial leaders.

- S&P 500 Slips on Tech Profit-Taking: The index pulled back and fell 0.69% to 6,415.54 after five August record highs, closing lower as traders booked profits in Big Tech names. Nvidia lost 2%, while Amazon and Apple shed about 1%, reflecting stretched valuations under pressure from rising yields.

- Nasdaq Drops Amid Megacap Retreat: The Nasdaq Composite dropped 177 points, or 0.82%, to 21,279.63 as selling hit leading technology stocks, with profit-taking accelerating at the unofficial end of the summer season. The decline underscored concerns that higher rates could weigh on growth-sensitive sectors.

- European Shares Slide to One-Month Low on Fiscal Worries: The Stoxx 600 fell 1.5% in its steepest loss since early August, with travel and technology leading declines. The DAX dropped 2.29% in Frankfurt, the FTSE MIB slid 1.61% in Milan, and the CAC 40 fell 0.69% in Paris. London’s FTSE 100 shed 0.87% as 30-year UK borrowing costs hit their highest since 1998 and sterling fell over 1%. Eurozone inflation edged up to 2.1% in August, with core steady at 2.3%. Spain’s jobless claims rose 0.91% to 2.43 million, though net formal jobs still grew, while France faced political pressure ahead of a 8 September no-confidence vote.

- Asia-Pacific Markets End Mixed as Tariff Uncertainty Lingers: Japan’s Nikkei 225 gained 0.29% to 42,310.49 and Topix rose 0.61%, with Suntory Beverage & Food up 2.94% on leadership changes. India’s Sensex advanced 0.48% and Nifty 50 added 0.31% after reports of potential tariff cuts on US imports. South Korea’s Kospi rose 0.94% and Kosdaq 1.15% as inflation slowed to 1.7%. By contrast, Hong Kong’s Hang Seng fell 0.5% and China’s CSI 300 slipped 0.74%. Australia’s ASX 200 lost 0.3% as regulators fined a SocGen unit AU$3.88m and the current account deficit narrowed to AU$13.7bn. Indonesia’s CPI eased to 2.3%, showing weak demand.

- Oil Prices Gain as Supply Risks Mount: Brent settled 1.45% higher at $69.14 per barrel, while WTI rose 2.47% to $65.59. Escalating Russia-Ukraine hostilities disrupted facilities handling an estimated 17% of Russia’s oil processing capacity. Traders also looked ahead to an OPEC+ subset meeting on 7 September, though major policy changes appear unlikely.

- Treasury Yields Surge on Fiscal Concerns: The 10-year Treasury yield rose 5 basis points to 4.27%, while the 30-year climbed over 5 basis points to 4.97%, its highest since late July. The 2-year yield added 3 basis points to 3.66%. The sharp rise reflected fears that the US government may need to refund billions in tariff revenues, stretching fiscal balances, while 30-year German yields hit their highest since 2011 and French long bonds reached levels last seen in 2009.

- US Manufacturing Contracts Again as ISM Stays Below 50 for Sixth Month: The ISM manufacturing index rose to 48.7 in August from 48.0 in July, slightly above the 48.5 forecast but still marking a sixth consecutive month of contraction. Spending on factory construction fell 6.7% year-on-year in July, highlighting persistent weakness in capital outlays. Out of 18 industries surveyed, 7 reported growth. Manufacturing accounts for 10.2% of the US economy, and the weakness underscores the pressure from tariff-related uncertainty and softer demand.

FX Today:

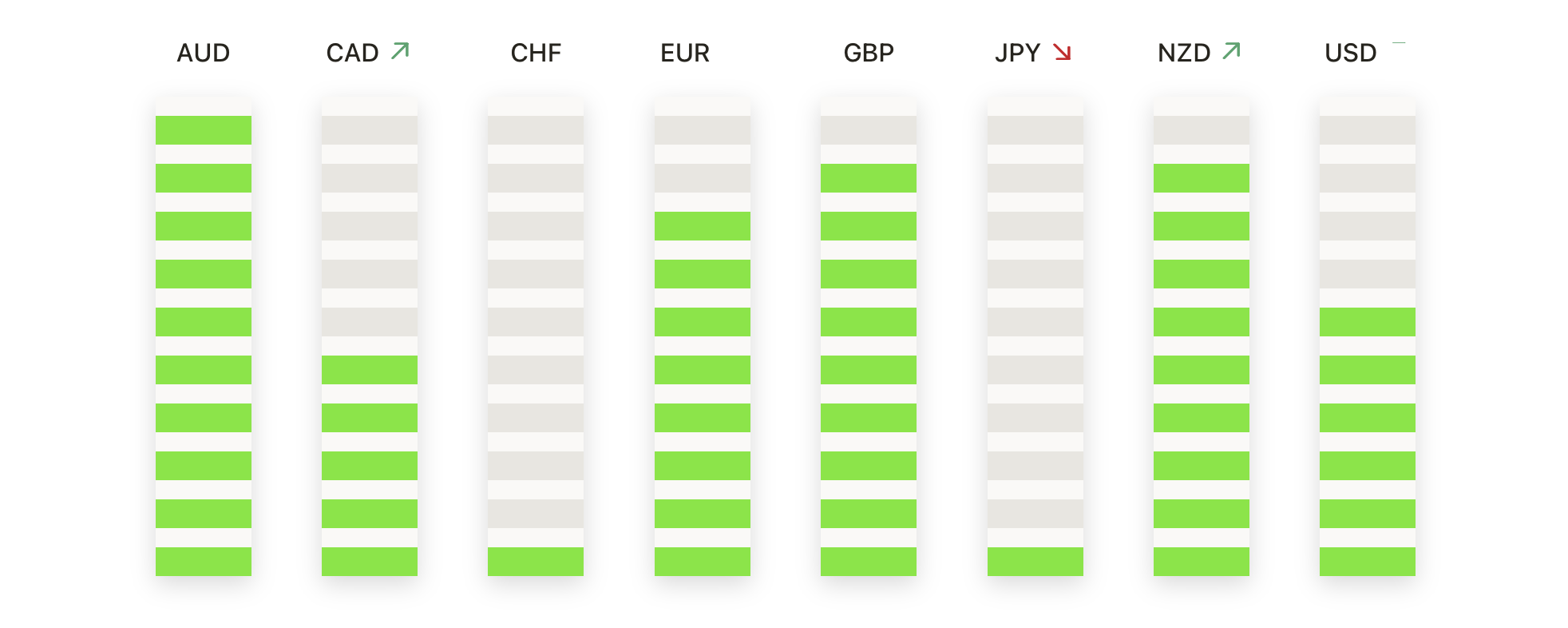

- EUR/USD Falls Back as Sellers Regain Control: The pair closed at 1.1639 with a 0.61% decline after swinging between 1.1783 and 1.1613. The move erased much of the prior week’s progress and confirmed a reversal from recent highs, leaving price back under the 50-day SMA at 1.1666. Despite the setback, EUR/USD remains supported above the 100-day SMA at 1.1519 and the 200-day at 1.1047, both of which continue to rise. The pair has been consolidating within a wide 1.1600–1.1800 band, though momentum has shifted toward the lower boundary. A decisive break beneath 1.1600 would expose the 1.1520 region near the 100-day average, while on the upside, 1.1700 has turned into resistance that must be cleared to reassert bullish momentum.

- GBP/USD Drops Sharply as Sellers Take Control Below Key Averages: The pair slid 1.14% to settle at 1.3390 after trading between 1.3549 and 1.3340 in one of its steepest daily declines in weeks. The fall dragged price under both the 50-day SMA at 1.3492 and the 100-day at 1.3452, a shift that reinstates downside pressure. Immediate support lies at 1.3340, the day’s low, with a break pointing to 1.3300 and potentially the 200-day SMA at 1.3053. Resistance is now concentrated in the 1.3450–1.3500 zone where the moving averages converge, and only a clear recovery above this area would alleviate selling pressure and re-open the path toward 1.3550.

- USD/CHF Rebounds as Buyers Defend 0.8000 Pivot: The pair advanced 0.55% to close at 0.8046 after rebounding from a low of 0.7998 to reach 0.8060. The recovery above the 0.8000 handle highlights continued demand at this key level, though price remains capped beneath the 50-day SMA at 0.8051 and the 100-day at 0.8122, both pointing lower. The broader downtrend remains intact under the 200-day SMA at 0.8514. A sustained move above 0.8050 would improve momentum and allow for a test of 0.8120, while a return below 0.8000 would shift focus back to 0.7950 as the next support level.

- USD/JPY Climbs to 148.35 as Buyers Challenge 200-Day Average: The pair gained 0.80% on the day to finish at 148.35 after rallying from 147.05 to 148.94, its strongest daily rise in over a week. The close lifted the market above the 50-day SMA at 147.07 and the 100-day at 145.61, placing it back into the upper portion of its August range. The 200-day SMA at 148.82 capped the intraday high, leaving the 149.00 region as a critical barrier. A clear break above 149.00 would strengthen momentum and target 150.00, while initial support lies at 147.00 followed by 146.50 and 145.60 if pullbacks develop.

- AUD/USD Slips as Rejection Near 0.6560 Caps Recovery: The pair closed 0.48% lower at 0.6520 after failing to hold a rally to 0.6559 and retreating to a low of 0.6483. The decline left the market hovering around the 50-day SMA at 0.6518, with additional support from the 100-day at 0.6481 and the 200-day at 0.6385. Repeated failures to clear resistance at 0.6560 have reinforced the cap on upside momentum. A break beneath 0.6480 would expose the 0.6400 base, while only a push above 0.6560 would re-open the path toward 0.6600.

- Gold Breaks Out to $3,536 as Record High Extends Rally: The metal surged 2.6% to settle at $3,536 after climbing from $3,470 to a new all-time high at $3,540. The move produced a powerful breakout above the August consolidation range and lifted price decisively through the 50-day SMA at $3,353, the 100-day at $3,331, and the 200-day at $3,065. The former resistance zone around $3,420 now acts as support, reinforcing the strength of the breakout. Holding above $3,500 keeps the focus on $3,550–$3,600 as the next upside objectives, while a pullback toward $3,470 would represent initial profit-taking risk.

Market Movers:

- Megacap Technology Stocks Weigh on Indexes as Nvidia and Apple Slide: Nvidia fell nearly 2% while Amazon and Apple each lost around 1%, with Meta and Microsoft also edging lower, pressuring the broader benchmarks.

- Chipmakers Retreat on Renewed Sector Weakness: ARM Holdings dropped more than 4% while Lam Research and KLA fell over 3%, joined by declines of more than 2% in ASML and Microchip Technology.

- Kraft Heinz Slumps After Announcing Breakup Plan: Shares tumbled over 6% after the company unveiled plans to split into two units, one focused on condiments and boxed meals and the other on grocery staples.

- Block Declines on Analyst Downgrade: Shares of Block lost more than 4% after BNP Paribas Exane cut its rating to neutral from outperform, citing a less favourable outlook.

- Cytokinetics Surges on Positive Trial Results: Shares soared more than 40% after its late-stage heart disease therapy delivered results that exceeded analyst expectations.

- Ionis Pharmaceuticals Jumps on Strong Phase 3 Data: The stock climbed over 35% after announcing its Olezarsen drug significantly reduced triglycerides and acute pancreatitis events in late-stage studies.

- United Therapeutics Rallies on Lung Disease Treatment Success: Shares surged more than 33% after revealing its Tyvaso Inhalation Solution met its primary efficacy goal in a late-stage trial.

September opened with caution as equities retreated under the weight of renewed tariff uncertainty and a sharp rise in bond yields, while gold’s record high underscored demand for havens. The pullback followed a strong August for Wall Street, leaving investors focused on whether upcoming labour market data can steady sentiment and guide expectations for the Federal Reserve’s next policy move. With fiscal pressures intensifying and yields testing fresh highs, the balance between stretched equity valuations and safe-haven demand is set to shape market direction in the weeks ahead.