Markets closed lower on Friday, marking the third consecutive decline for the S&P 500 as investors remained cautious amid escalating geopolitical tensions. The week-long conflict between Israel and Iran reached a critical turning point on Sunday, with the US joining hostilities by launching strikes against three Iranian nuclear facilities. Prior to the weekend escalation, investors were already wary, especially after a report suggested potential revocation of waivers for semiconductor manufacturers, pressuring major tech stocks. Uncertainty surrounding the conflict’s impact on global stability and economic growth overshadowed comments from Federal Reserve officials hinting at potential interest rate cuts as early as July. Markets now brace for heightened volatility as the geopolitical crisis deepens.

Key Takeaways:

- Dow Ends Slightly Higher Amid Geopolitical Uncertainty: The Dow Jones Industrial Average rose 35.16 points, or 0.08%, to close at 42,206.82 on Friday. Despite ongoing tensions in the Middle East and a muted broader market, the index managed a modest weekly gain of 0.02%.

- S&P 500 Declines for Third Consecutive Session: The S&P 500 fell 0.22% to finish at 5,967.84, its third straight daily decline, and ended the week down 0.2%.

- Nasdaq Slides as Semiconductor Stocks Drag: The Nasdaq Composite lost 0.51% to settle at 19,447.41, with chipmakers leading the decline after reports suggested the US may revoke export waivers for some semiconductor manufacturers.

- European Stocks Rebound Friday but End the Week Lower: European equity markets edged higher to close the week but were broadly negative overall, as investor focus remained fixed on escalating hostilities between Israel and Iran. The pan-European Stoxx 600 index rose 0.1% on Friday yet posted a 1.5% weekly decline. In the UK, the FTSE 100 dipped 0.86% on the week to 8,774.65, as a sharp 2.7% fall in May retail sales underlined growing concerns about consumer demand. German markets rallied, with the DAX jumping 1.27% on Friday, helped by stabilising producer prices which fell 1.2% year-on-year in May, matching expectations. France’s CAC 40 added 0.5%, bouncing off a one-month low and snapping a three-day losing streak. Italy’s FTSE MIB rose 0.74%. Investor caution remains elevated as the regional conflict risks further escalation following the weekend’s developments.

- Asia-Pacific Markets Mixed Amid Rising Tensions and Rate Holds: Asia-Pacific indices delivered a mixed performance on Friday, with markets responding to stable Chinese rates and rising geopolitical uncertainty. Japan’s Nikkei 225 fell 0.22% to 38,403.23, while the broader Topix shed 0.75% amid concerns over rising core inflation, which reached 3.7% in May. South Korea’s Kospi surged 1.48% to 3,021.84, its highest level in over 42 months, as investor sentiment strengthened. The Kosdaq also gained 1.15%. In China, the CSI 300 ended flat at 3,846.64, with the People’s Bank of China leaving key lending rates unchanged. Hong Kong’s Hang Seng outperformed with a 1.26% gain. In Australia, the S&P/ASX 200 fell 0.21%, pressured by commodity-linked stocks. India’s Nifty 50 advanced 1.05% and the Sensex climbed 1.13%, supported by domestic institutional buying.

- Oil Spikes as US Strikes Escalate Middle East Conflict: Crude oil prices are set to open sharply higher after the US launched airstrikes on three Iranian nuclear sites over the weekend, joining Israel in its ongoing military campaign. Brent crude, which fell 2.13% to $77.17 on Friday as traders hoped for diplomacy, is now expected to rebound strongly amid renewed fears of regional supply disruption. The strikes mark a major escalation in the conflict, raising the risk of retaliatory actions against energy infrastructure across the Gulf. With Iran being a key OPEC producer, the involvement of the US adds a fresh layer of geopolitical risk to oil markets.

- Treasury Yields Dip as Fed Signals Possible July Cut: The US 10-year Treasury yield eased to 4.379%, down just over 1 basis point, while the 2-year yield dropped more than 3 basis points to 3.908%. Fed Governor Christopher Waller indicated a July rate cut is on the table, citing cooling inflation. Bond markets also remained sensitive to headlines surrounding the Middle East conflict, adding to the flight-to-safety momentum.

FX Today:

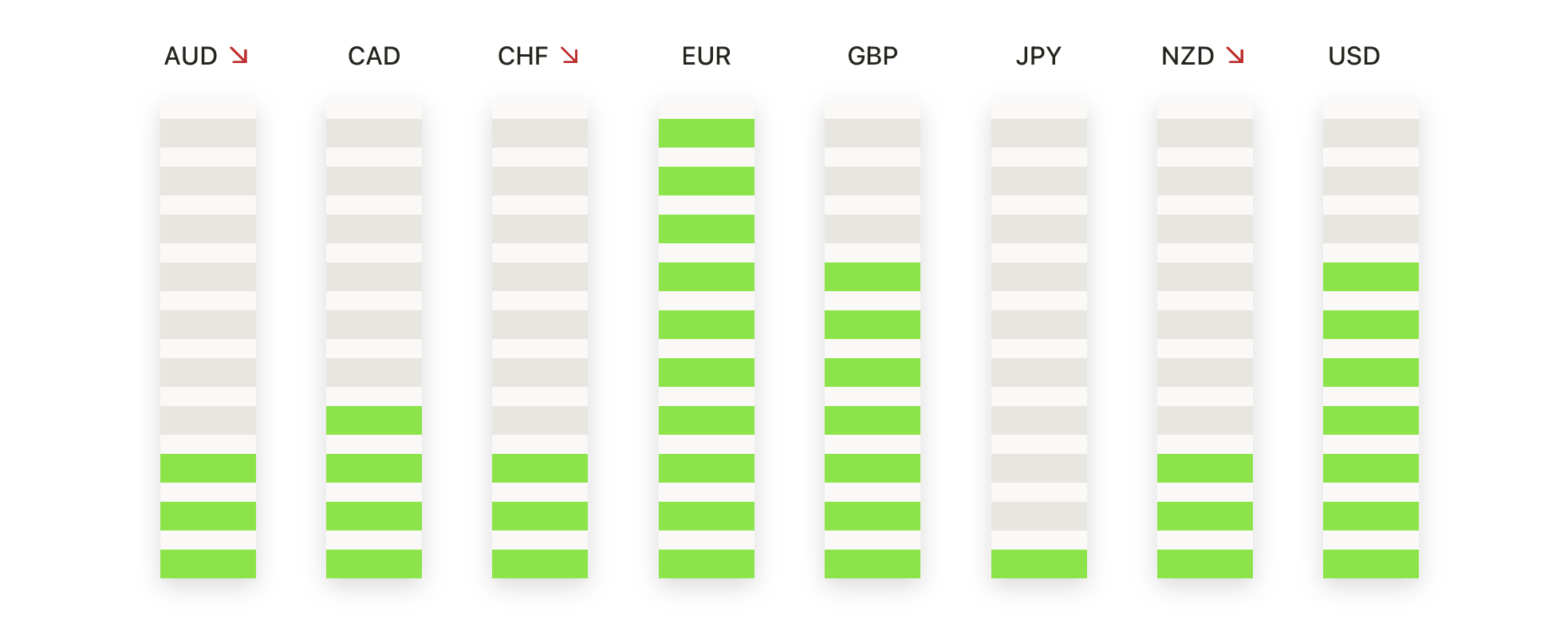

- EUR/USD Builds on Gains as Bullish Structure Holds: The EUR/USD pair closed Friday at 1.1517, up 0.20% on the day, maintaining its advance above the 1.1500 breakout zone. After reaching a session high of 1.1543 and dipping to 1.1489, the euro showed resilience and held firmly within its recent bullish trend. The pair continues to benefit from momentum carried over from its June breakout above 1.1450. All major SMAs remain aligned in favour of further upside, with the 50-day at 1.1359 and the 200-day far below at 1.0842. As long as the pair holds above the 1.1450–1.1500 region, buyers retain control. Immediate resistance lies near 1.1600, while a close below 1.1450 would suggest the rally is losing steam.

- GBP/USD Softens but Holds 50-Day SMA Support: GBP/USD ended the week at 1.3449, easing 0.15% on Friday after failing to break through resistance at 1.3511. The session’s narrow-bodied candle signalled hesitation as momentum faded near the upper end of its recent range. Despite the dip, the pair held above the 50-day SMA at 1.3397, a key level tested several times in recent months. The trend remains broadly bullish, supported by rising 100-day and 200-day SMAs at 1.3084 and 1.2930. However, the inability to reclaim 1.3550 points to a potential consolidation phase. A sustained drop below 1.3400 would open the door to 1.3300. On the upside, a breakout above 1.3550 could trigger a renewed push toward 1.3700.

- USD/JPY Breaks Higher, Clears 146.00 Barrier: USD/JPY rose 0.49% on Friday to close at 146.15, marking a six-day winning streak and its strongest finish in nearly two months. The pair pushed through resistance at 146.00, reaching an intraday high of 146.17 before settling near the top of the range. The daily structure confirmed bullish control, supported by a close above the 50-day SMA at 144.06. With the 100-day SMA at 146.85 now within reach, further upside may target 147.00 and 148.50. Key support now rests near 145.50, with any break below that level suggesting a false breakout. The trend structure has clearly shifted upward, and the current momentum favours continuation unless price slips back under 144.00.

- USD/CAD Extends Recovery Toward Key Resistance: The USD/CAD pair closed at 1.3735 on Friday, advancing 0.27% after reaching a high of 1.3746. This marked a fourth consecutive daily gain and the highest close since late May. Price action remained bullish throughout the session, staying well above short-term support at 1.3680. The 50-day SMA at 1.3801 looms just overhead, creating a critical test zone for bulls. A breakout could accelerate gains toward 1.4043, the 100-day SMA. However, the broader trend remains bearish, and a rejection here could signal a temporary top. A drop below 1.3680 would weaken the near-term structure and expose 1.3600 once again.

- AUD/USD Slips Toward 50-Day Average After Rejection: AUD/USD declined 0.49% to end the week at 0.6449, reversing early gains and closing near the session low of 0.6448. The pair has now dropped for three straight sessions and is testing support at the 50-day SMA, which sits at 0.6438. The rejection earlier this week at 0.6550 reinforced a broader consolidation pattern. Below 0.6435, further losses could target the 200-day SMA at 0.6428 and possibly 0.6370. Bulls must reclaim 0.6500 to regain control, though the current structure favours a range-bound or corrective bias in the near term.

- Gold Holds Firm Near Multi-Week Highs Ahead of Escalation: Gold settled at $3,371 on Friday, gaining just $1 on the day after trading between $3,340 and $3,374. The metal’s tight range signalled consolidation near key resistance at $3,375, with bulls retaining control after a sharp rise earlier in the week. Technical momentum remains bullish, with the 50-day SMA at $3,309 and price comfortably holding above $3,300. A breakout above $3,375 could send gold back toward record highs near $3,450. Key downside levels include $3,340 and the 50-day average.

Market Movers:

- Chipmakers Weigh on Broader Market: Semiconductor stocks dragged the major indices lower on Friday following a report that the US may revoke waivers for certain chip manufacturers. Lam Research and KLA Corp both fell more than 2%, while Applied Materials, Intel, Qualcomm, NXP Semiconductors, Broadcom, and Marvell Technology each declined over 1%.

- Accenture Drops on Margin Outlook Cut: Accenture shares tumbled more than 6%, making it the biggest loser in the S&P 500, after the company lowered its full-year operating margin forecast to 15.6% from a prior range of 15.6%–15.7%, disappointing investors.

- Smith & Wesson Slides After Earnings Miss: Smith & Wesson Brands plunged over 19% after reporting fourth-quarter adjusted earnings per share of 20 cents, missing consensus estimates of 23 cents and raising concerns about declining firearms demand.

- GMS Soars on Home Depot Acquisition Interest: GMS Inc surged over 24% following a report by The Wall Street Journal that Home Depot has made an offer for the company, potentially sparking a bidding war with QXO Inc, which had previously made a $5 billion bid earlier.

- Circle Internet Extends Rally on Stablecoin Legislation: Circle Internet Group added over 20% on Friday, building on Wednesday’s 34% rally, after the US Senate passed legislation establishing regulatory guidelines for stablecoins tied to the US dollar.

Markets face a tense start to the week after the US launched airstrikes on Iranian nuclear facilities over the weekend, deepening the Israel-Iran conflict and raising fears of wider regional instability. Last week ended with a cautious tone, as investors wrestled with rate cut signals from the Federal Reserve and growing geopolitical risks. With oil poised to rebound and gold near recent highs, safe haven demand may intensify if the conflict escalates further. Traders will closely watch incoming economic data and central bank commentary for clues on the Fed’s July policy stance, but near-term sentiment is likely to be dominated by developments in the Middle East.