Wall Street fell sharply on Monday as renewed tariff tensions sparked a broad-based sell-off, following President Donald Trump’s announcement of new levies on imports from multiple nations. All three major indices logged their worst daily performances since mid-June, as investors digested the latest escalation in trade tensions. The Dow Jones Industrial Average plunged 422 points, while the S&P 500 and Nasdaq also posted steep losses. Trump’s social media posts revealed tariff letters to leaders of seven countries, with duties as high as 40% set to begin on August 1. Technology, autos, and politically exposed sectors led the decline.

Key Takeaways:

- Dow Drops Over 400 Points on Fresh Tariff Escalation: The Dow Jones Industrial Average fell 422.17 points, or 0.94%, to 44,406.36 in its sharpest decline since mid-June. Markets turned lower after President Trump announced new tariffs on imports from seven nations. Japan, South Korea, Kazakhstan, and Malaysia will face 25% tariffs. South Africa will face a 30% tariff, while Myanmar and Laos will be hit with 40% duties.

- S&P 500 Falls as Broad Sell-Off Accelerates: The S&P 500 declined 0.79% to 6,229.98, dragged down by weakness in technology, autos, and consumer stocks. Apple, AMD, and Alphabet all lost ground as the market priced in the potential economic impact of sweeping new trade measures.

- Nasdaq Declines Nearly 1% as Big Tech Retreats: The Nasdaq Composite dropped 0.92% to close at 20,412.52. Alphabet fell over 1% while Nvidia and AMD also declined. Tech shares led the decline, pressured by rising geopolitical risks and investor caution over Trump’s statement targeting BRICS-aligned countries for future tariffs.

- European Markets Advance Despite Tariff Uncertainty: European equity markets finished mostly higher on Monday, lifted by signals of progress in EU–US trade talks. Germany’s DAX rallied 1.20%, lifted by strong industrial production data showing a 1.2% monthly rise in May, driven by gains in the automotive and energy sectors. Italy’s FTSE MIB added 0.74%, while France’s CAC 40 rose 0.2%. However, the UK’s FTSE 100 slipped 0.19%, with housebuilders under pressure after Halifax reported flat house prices for June. Swedish CPI surged 0.5% month-on-month and 2.9% year-on-year. Meanwhile, eurozone retail sales dropped 0.7% in May, reversing April’s 0.3% gain and suggesting consumers are pulling back.

- Asia Mixed Ahead of Tariff Reveal, Japan Leads Declines: Asian markets ended mixed on Monday, with trading concluding before the US tariff announcement was made public. Japan’s Nikkei 225 fell 0.56% amid a 2.9% annual drop in real wages, the sharpest decline in 20 months. The Topix also declined 0.57%. South Korea’s Kospi edged up 0.17%, supported by selective buying in energy and industrials, while the Kosdaq rose 0.34%. Australia’s ASX 200 slipped 0.16% ahead of the Reserve Bank of Australia’s policy meeting, where a 25 basis point rate cut is widely expected. China’s CSI 300 fell 0.43% and Hong Kong’s Hang Seng dropped 0.61% as sentiment remained cautious. Thailand’s CPI declined 0.25% year-on-year, remaining below the central bank’s 1–3% target range for a fourth month.

- Oil Climbs Despite OPEC+ Output Increase: Brent crude gained $1.34 to close at $69.64, while WTI added $1.02 to settle at $68.02. Prices rose even as OPEC+ agreed to boost August production by 548,000 barrels per day, more than expected. Analysts say nearly 80% of prior voluntary cuts will be reversed. The group is expected to announce another increase of 550,000 bpd at its 3 August meeting. Market support held despite growing concern over US trade actions potentially curbing global growth.

- Treasury Yields Rise as Deadline Extended to August: The 10-year Treasury yield rose 5 basis points to 4.387%. The 30-year yield climbed to 4.921% and the 2-year moved up to 3.899%. President Trump postponed the tariff enforcement deadline to 1 August, extending trade-related uncertainty.

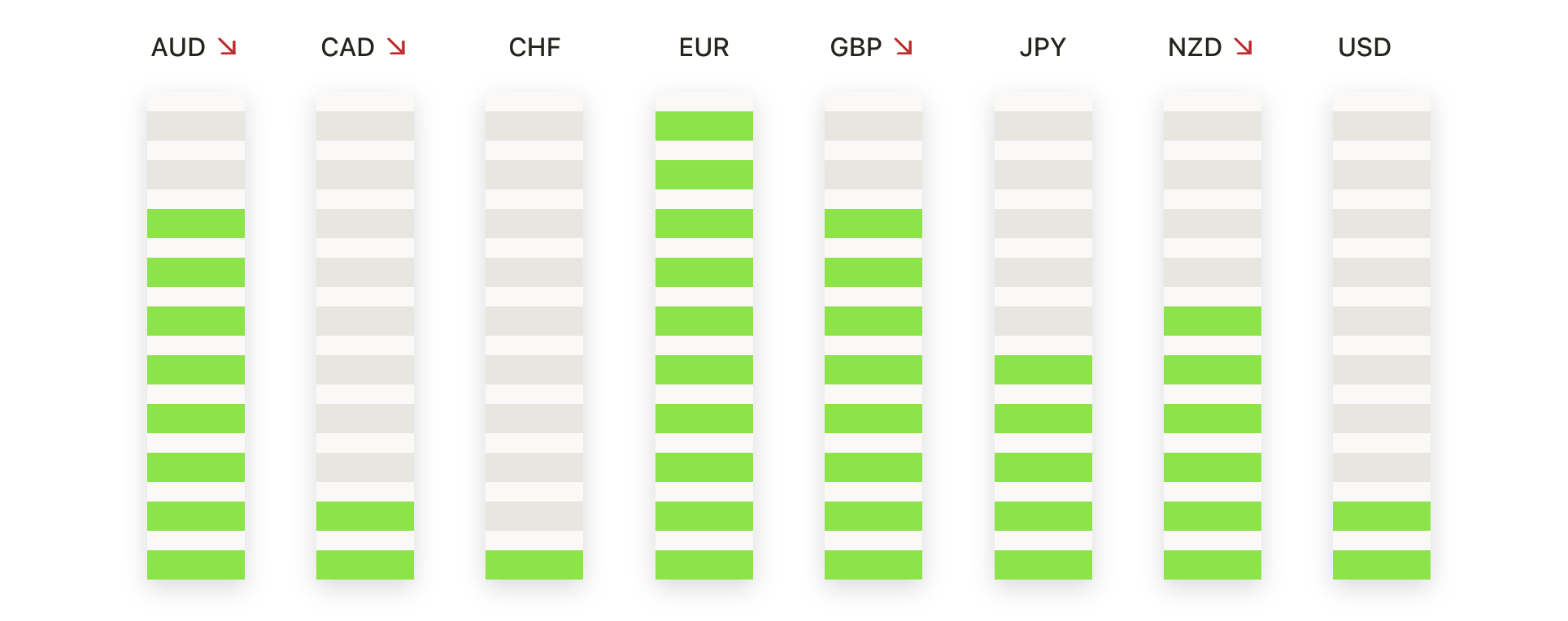

FX Today:

- EUR/USD Fades From Highs but Holds Above Key Support: EUR/USD closed at 1.1722 on Monday, falling 0.41% after reaching a session high of 1.1789 and a low of 1.1686. Despite the drop, the euro held above near-term support at 1.1680, maintaining the broader ascending trend in place since mid-June. The 50-day SMA, rising at 1.1434, remains well below market price and continues to support the bullish structure. Immediate resistance is seen at 1.1800, while a move above that level could retest the 1.1900 zone. If selling pressure intensifies, a break below 1.1680 could expose further downside toward 1.1550 and 1.1500. The pair remains above the 100-day and 200-day SMAs, now positioned at 1.1170 and 1.0874 respectively.

- GBP/USD Slips After Rejection Near June Highs: GBP/USD closed at 1.3611, declining 0.27% after touching a high of 1.3661 and dipping to a low of 1.3580. The rejection near 1.3660 marks a third attempt to break the June highs near 1.3750. Support remains firm at the rising 50-day SMA at 1.3477, which has guided the trend higher since mid-May. Resistance stands at 1.3700 and 1.3750, while initial support is seen at 1.3550. A break below this level could test 1.3500 and challenge the lower boundary of the rising channel. The 100-day and 200-day SMAs, at 1.3214 and 1.2952 respectively are well below current price.

- USD/CAD Extends Rebound Toward 50-Day SMA: USD/CAD closed at 1.3665, rising 0.51% after trading between 1.3586 and 1.3668. The pair posted a strong bullish candle, confirming follow-through from last week’s bounce at 1.3560. Price now approaches the 50-day SMA, located at 1.3757, which marks the next technical target in the short-term recovery. Despite recent gains, the pair remains below the 100-day and 200-day SMAs at 1.3974 and 1.4036 respectively, indicating the broader structure is still bearish. Key resistance is seen at 1.3720 and the 1.3800 psychological barrier. On the downside, 1.3600 is initial support, followed by 1.3550.

- USD/CHF Continues Recovery Within Bearish Structure: USD/CHF closed at 0.7979, advancing 0.57% after reaching a high of 0.7986 and a low of 0.7911. The USD/CHF remains below the 50-day SMA at 0.8186 and deep within a longer-term downtrend. Resistance is seen at 0.8050, a key level that capped multiple rallies over the past month. Further upside could test 0.8180, but failure to break this area would likely keep the pair confined. On the downside, 0.7900 and 0.7820 serve as major support levels. With the 100-day and 200-day SMAs well above current price at 0.8426 and 0.8647 respectively.

- USD/JPY Climbed on New Tariff Announcement Against Japan: USD/JPY closed at 146.02, rising 1.06% after rebounding from a low of 144.22 and touching a high of 146.15. Monday’s rally followed President Trump’s letter imposing a 25% tariff on Japanese imports, lifting the US dollar sharply against the yen. The breakout cleared the 50-day SMA at 144.55 and challenged the 100-day SMA at 145.97. Next resistance is located at 147.50 and 150.00, while initial support lies at 145.00 and 144.50. A sustained move above the 100-day average could shift momentum firmly back to bulls, though the 200-day SMA at 149.55 remains a key longer-term barrier.

- Gold Holds Above Support as Consolidation Persists: Gold closed at $3,337, rising 0.35% after hitting a low of $3,296 and a high of $3,343. The metal formed a modest bullish candle, holding above short-term support at $3,300 and continuing a multi-week consolidation phase below record highs. The 50-day SMA at $3,321 and 100-day SMA at $3,176 both remain upward sloping, confirming underlying strength in the trend. Immediate resistance lies at $3,375 and $3,400, while support is firm at $3,290 and $3,250. The structure remains a sideways range between $3,290 and $3,400, with the bias still tilted upward as long as price stays above key moving averages. A decisive breakout above $3,400 would be needed to resume the broader rally, while a break below $3,290 could signal short-term exhaustion and target the 200-day SMA at $2,928.

Market Movers:

- Tesla Drops Over 6% After Musk Political Move: Tesla (TSLA) closed down more than 6% after CEO Elon Musk announced the formation of a new political party called the “America Party,” drawing backlash from President Trump and raising concerns about damage to Tesla’s brand and consumer demand.

- Chip Stocks Slide on Trade Concerns: ARM Holdings (ARM) fell over 5%, while Marvell Technology (MRVL) dropped more than 4%. Other notable decliners included AMD, NXP Semiconductors, Microchip, Intel, GlobalFoundries, ON Semiconductor, and Qualcomm, all down more than 2% on renewed trade tension.

- Webull Plunges on Equity Purchase Agreement: Webull (BULL) sank more than 10% after entering a standby equity purchase agreement with a Yorkville Partners fund.

- WNS Holdings Surges on Capgemini Buyout Deal: WNS Holdings Ltd (WNS) jumped more than 15% after Capgemini SE agreed to acquire the company for $3.3 billion, valuing WNS at $76.50 per share in an all-cash transaction.

- Phibro Animal Health Jumps on JPMorgan Upgrade: Phibro Animal Health Corp (PAHC) gained over 7% after JPMorgan Chase upgraded the stock to overweight from neutral and set a price target of $35, citing improving fundamentals.

Markets began the week under pressure as investors responded sharply to President Trump’s sweeping tariff announcement targeting key US trading partners. Equities fell across major US indices, with risk sentiment dented by the potential for further retaliation and uncertainty surrounding BRICS-aligned nations. European stocks outperformed amid hopes of a US–EU deal, while Asian markets were spared the immediate impact due to timing. Oil prices rose despite OPEC+ output increases, and Treasury yields climbed as the August 1 deadline loomed.