Rising global trade tensions set the backdrop for Monday’s session but investors remained focused on potential progress in upcoming US-China talks. Steel tariffs, EU trade strains, and fresh economic data shaped sentiment, while notable gains in commodities and technology stocks lifted confidence. A jump in oil and gold prices highlighted safe-haven demand, even as US Treasury yields edged higher. Meanwhile, European and Asian markets digested the latest PMI readings and tariff headlines, leaving investors to navigate a complex macro environment as June trading begins.

Key Takeaways:

- Dow Inches Higher Amid Trade Tensions: The Dow Jones Industrial Average edged up 35.41 points, or 0.08%, to close at 42,305.48. Gains were muted as investors weighed conflicting signals on US-China trade relations and looming tariff increases.

- S&P 500 Climbs as Steel Stocks Surge: The S&P 500 rose 0.41% to 5,935.94, supported by a strong rally in steel and energy shares. The index extended its positive momentum from May despite renewed geopolitical uncertainty.

- Nasdaq Advances on Tech Strength: The Nasdaq Composite gained 0.67%, finishing at 19,242.61. Chip stocks led the advance, with robust performances from Micron, AMD, and Nvidia helping offset trade-related jitters.

- Europe Slips as Steel Tariffs Stir Trade Frictions: European stock markets closed mixed on Monday, as fresh US tariff moves reignited transatlantic tensions. The Stoxx Europe 600 index dipped 0.1%, with autos stocks falling 2% after Trump pledged to double steel tariffs to 50%. Germany’s DAX declined 0.3% to 23,496, weighed by tariff concerns and a softer manufacturing PMI, which slipped to 48.3. France’s CAC 40 dropped 0.20%, despite a stronger-than-expected PMI at 49.8. Italy’s FTSE MIB eased 0.2% after its PMI missed forecasts at 49.2, while Spain’s PMI climbed to a four-month high of 50.5, helping temper losses. The UK’s FTSE 100 was flat, up just 0.02%, though its manufacturing PMI rose to a three-month high of 46.4. Meanwhile, Danish energy giant Orsted highlighted the cost risks from higher US tariffs on steel for wind projects, underscoring broader concerns for European exporters.

- Asia Mostly Lower as Tariff Concerns Weigh: Asia-Pacific markets mostly declined after President Trump’s steel tariff pledge fuelled trade fears. Japan’s Nikkei 225 fell 1.30% to 37,470.67, despite a modest improvement in factory activity, with the manufacturing PMI rising to 49.4 but still in contraction. The Topix slipped 0.87%. South Korea’s Kospi closed nearly flat at 2,698.97, while the small-cap Kosdaq advanced 0.81% ahead of the June 3 presidential election. South Korea’s manufacturing PMI held below 50 at 47.7, signalling continued contraction. Australia’s ASX 200 edged down 0.24% as its manufacturing PMI slipped to 51.0, marking the first production contraction in three months. Hong Kong’s Hang Seng shed 1.2%, while India’s Nifty 50 lost 0.10%. Markets in China, Malaysia, and New Zealand were closed for holidays, leaving regional sentiment largely focused on tariff risks and soft manufacturing trends.

- Oil Jumps Nearly 4% as OPEC+ Maintains Steady Output: US crude futures surged $2.36, or 3.88%, to $63.15 per barrel, while Brent climbed 3.92% to $65.24. A steady production hike by OPEC+ and falling US rig counts supported prices. Supply concerns and US demand outlooks remain in sharp focus.

- Treasury Yields Tick Higher Amid Trade Disputes: Yields rose modestly as US-China trade tensions intensified. The 10-year yield added over 2 basis points to 4.446%, while the 2-year yield rose to 3.937%. The 30-year yield climbed 4 basis points to 4.973%, reflecting cautious sentiment.

- US Manufacturing and Construction Data Show Weakness: The ISM manufacturing index stayed in contraction at 48.5%, with inventories and new export orders declining. Construction spending unexpectedly fell, signalling softness in key sectors despite strong market performance.

FX Today:

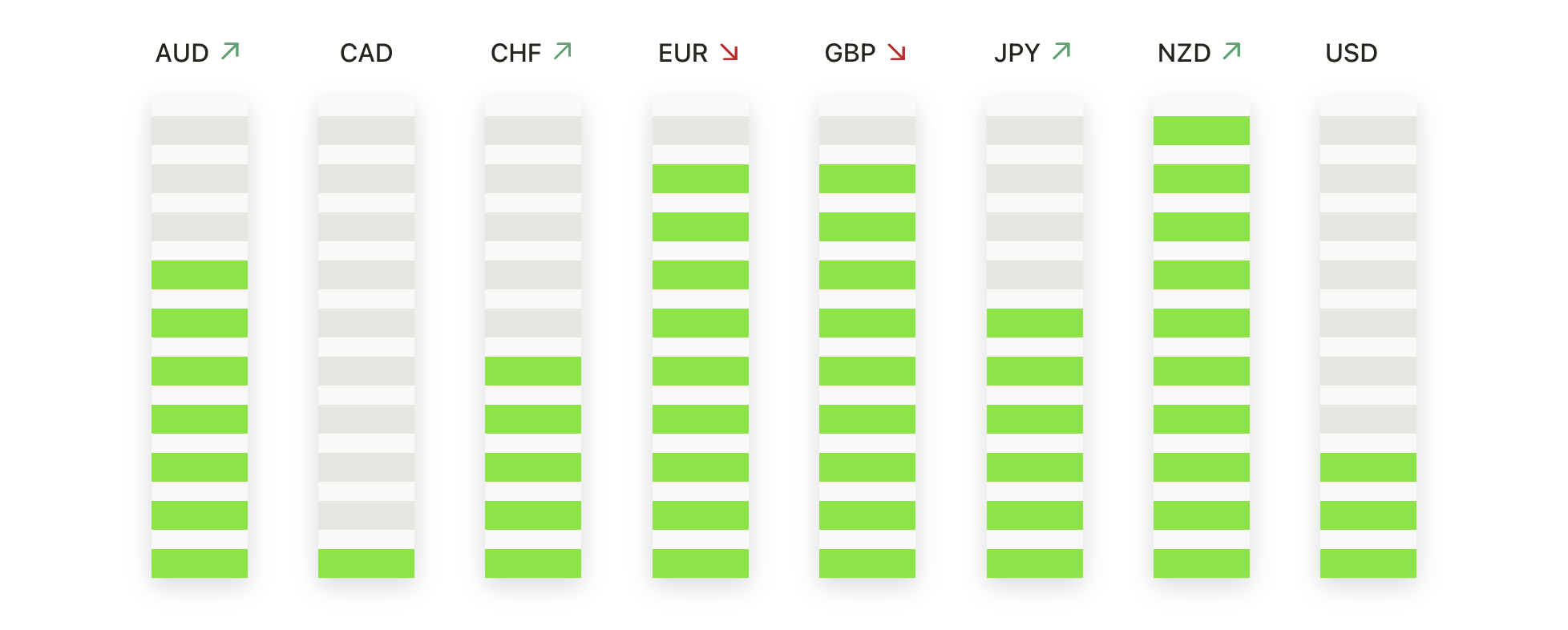

- EUR/USD Extends Breakout as Bulls Reclaim 1.1400: EUR/USD rallied firmly on Monday, closing at 1.1444 with a 0.86% gain as bullish momentum accelerated. The pair surged to an intraday high of 1.1449, its best level in more than two years, fuelled by broad US dollar softness and rising European yields. A sustained series of higher lows has kept buyers in control, supported by the 50-day SMA climbing at 1.1207. The 100-day and 200-day SMAs provide a solid base at 1.0872 and 1.0815. Short-term dips have attracted strong buying interest, with initial support now at 1.1350 and deeper demand near 1.1200. If EUR/USD holds above 1.1400, bulls may soon target the 1.1600 zone, with the broader trend outlook remaining firmly positive.

- GBP/USD Resumes Climb, Eyes Fresh Multi-Year Highs: GBP/USD extended its advance on Monday, finishing at 1.3546 after gaining 0.67%. The pair hit an intraday peak of 1.3559, approaching highs not seen since early 2022. Stronger-than-expected UK manufacturing PMI data provided a fresh catalyst, while the broader uptrend remains intact. The 50-day SMA continues to rise at 1.3229, with the 100-day and 200-day SMAs offering added support at 1.2919 and 1.2903. Price action continues to respect a bullish structure of higher highs and higher lows. A break above 1.3550 would open the path toward 1.3700, with potential for further gains to 1.3850. Key support rests at 1.3450 and below at 1.3300.

- USD/JPY Slides Toward Key Support Below 143.00: USD/JPY dropped sharply on Monday, closing at 142.68 with a 0.94% decline. The pair extended its pullback from recent highs near 146.00, pressured by safe-haven flows into the yen amid rising trade tensions. The 50-day SMA has turned lower at 145.04, reinforcing a more bearish near-term outlook. The pair has now posted a series of lower highs since late April. If the key support zone around 142.50 breaks, further downside targets could emerge near 141.00 and 140.00. On the upside, initial resistance stands at 144.00, followed by stronger resistance near the 50-day SMA at 145.00.

- Gold Surges Toward $3,400 as Bullish Trend Resumes: Gold rallied sharply on Monday, gaining 2.84% to close at $3,381. Renewed safe-haven demand, driven by escalating trade tensions and a weaker US dollar, propelled the metal higher. An intraday high of $3,382 leaves gold poised to challenge key resistance at $3,400. The 50-day SMA at $3,228 is trending higher, while the 100-day and 200-day SMAs remain strongly supportive at $3,041 and $2,833. The bullish structure remains intact, with buyers defending recent dips near $3,250. A breakout above $3,400 could open the door for a move toward all-time highs near $3,500. Immediate support is seen at $3,300 and around the 50-day moving average.

- Silver Spikes Above $34 as Bulls Seize Control: Silver soared 5.31% on Monday to close at $34.73, staging a decisive breakout above key resistance near $34. The rally was driven by strong safe-haven demand and supportive technical momentum. The 50-day SMA continues to rise at $32.71, while the 100-day and 200-day SMAs at $32.26 and $31.51 provide a firm technical base. If silver sustains gains above $34.50, the next resistance zone lies near $35.50, with potential to target fresh multi-year highs. On the downside, initial support is now at the breakout area of $34.00, with deeper backing around the 50-day SMA.

Market Movers:

- Steel Producers Surge on Tariff Hike: Cleveland-Cliffs and Century Aluminium each rose more than 20% after President Trump announced tariffs on US steel and aluminium imports would double to 50%. Steel Dynamics and Nucor gained over 10%, while Commercial Metals advanced more than 5%.

- Gold Miners Rally with Precious Metals Surge: Gold Fields climbed more than 9%, Anglogold Ashanti rose over 7%, and Newmont gained more than 5% as gold prices approached $3,400. Freeport McMoRan advanced more than 4% on renewed strength in precious metals.

- Zscaler Jumps After Price Target Boost: Zscaler gained more than 6% after UBS raised its price target to $315 from $260, citing strong cloud security demand and improved growth prospects.

- Vera Therapeutics Soars on Positive Trial: Vera Therapeutics surged 66% after reporting its Phase 3 trial for atacicept met the primary endpoint in treating immunoglobulin A nephropathy.

- Automakers Retreat on Tariff Fears: Stellantis, General Motors, and Ford each fell more than 3% as investors grew concerned about potential margin pressures from higher US steel and aluminium tariffs.

- Science Applications International Tumbles on Earnings: Science Applications International declined more than 13% after reporting Q1 earnings per share of $1.92, missing analysts’ expectations of $2.13.

- Tesla Slips on French Sales Decline: Tesla slipped more than 1% after May new-vehicle registrations in France dropped 57% year on year to nearly a three-year low, raising concerns over European sales.

The month starts with markets balancing renewed trade tensions against sector-specific strength. Steel tariffs and shifting global trade dynamics remain in sharp focus, while gains in commodities and technology stocks supported the broader tone. European and Asian markets reacted to fresh manufacturing data and tariff headlines, adding to cross-market volatility. In FX and commodities, strong directional trends persisted, with gold and silver attracting renewed flows. Traders now look ahead to U.S.-China discussions and key economic data that could drive the next market moves.