US stocks ended mixed on Tuesday as pressure in the technology sector weighed on broader indices, even as the Dow Jones briefly touched a record high. Nvidia and other chipmakers slumped, dragging the S&P 500 lower and pulling the Nasdaq into its steepest decline in weeks. By contrast, the Dow was supported by a sharp rise in Home Depot, with investors rotating into more defensive plays. Market participants also looked ahead to Federal Reserve Chair Jerome Powell’s highly anticipated speech at Jackson Hole, which many see as pivotal in shaping expectations for September’s policy decision. Alongside central bank uncertainty, geopolitical developments continued to influence sentiment, with renewed talks over Ukraine raising questions for energy markets and defence stocks.

Key Takeaways:

- Dow Edges Higher as Home Depot Lifts Index: The Dow Jones Industrial Average closed up 10.45 points, or 0.02%, at 44,922.27 after briefly touching a fresh record high earlier in the session. Gains were driven by Home Depot, which climbed 3% after maintaining its full-year outlook despite weaker-than-expected second-quarter results.

- S&P 500 Declines as Nvidia Leads Tech Selloff: The S&P 500 fell 0.59% to finish at 6,411.37, pressured by broad declines across technology shares. Nvidia dropped 3.5%, Advanced Micro Devices slid 5.4%, and Broadcom shed 3.6%. Software name Palantir was the weakest performer in the index, plunging more than 9%. The moves underscored fatigue in the AI-driven rally, with analysts suggesting that after the Nasdaq’s 40% run since April, a consolidation phase is natural.

- Nasdaq Pulls Back as Growth Shares Lose Momentum: The Nasdaq Composite lost 1.46% to 21,314.95, marking one of its sharpest daily drops in weeks. Selling pressure was concentrated in megacap tech names, with the so-called Magnificent Seven all finishing in the red.

- European Markets Rise but Defence Stocks Sink: Europe’s Stoxx 600 gained 0.73%, with broad strength across major bourses. London’s FTSE 100 advanced 0.34% to a record close of 9,189.22, while Paris’s CAC 40 climbed 1.21% and Milan’s FTSE MIB rose 0.89%. Frankfurt’s DAX added 0.45% to 24,423. However, the Stoxx Europe Aerospace and Defence index slumped 2.58% following White House talks between President Trump, President Zelenskyy and European leaders, raising hopes of a peace settlement in Ukraine. Italy’s Leonardo dropped 10.1%, Germany’s Hensoldt fell 9.5%, and Renk slid 8.2%, reflecting concerns that reduced conflict risk could weigh on future contracts.

- Asia-Pacific Markets Weaken as SoftBank Slides: Asian equities mirrored Wall Street’s pullback, with Japan’s Nikkei 225 down 0.38% to 43,546.29 and the Topix 0.14% lower at 3,116.63. South Korea’s Kospi fell 0.81% while the Kosdaq dropped 1.26%. Mainland China’s CSI 300 lost 0.38% to 4,223.37, and Hong Kong’s Hang Seng slipped 0.2% to 25,123, its lowest close in almost three weeks, amid data showing China’s youth unemployment surged to 17.8% in July. Australia’s S&P/ASX 200 dropped 0.7% to 8,896.2, while Indian markets diverged, with the Nifty 50 up 0.44% and the Sensex up 0.48%. SoftBank weighed heavily, plunging over 5% after announcing a $2 billion investment in Intel, snapping a nine-day winning streak.

- Oil Prices Retreat on Hopes of Russia–Ukraine Talks: Brent crude fell 1.22% to $65.79 a barrel, while US West Texas Intermediate for September delivery dropped 1.69% to $62.35. The more active October WTI contract slipped 0.73% to $62.24. The declines followed speculation that talks involving the US, Ukraine and Russia could lead to progress on sanctions relief, boosting supply prospects. Oil had settled around 1% higher in the previous session, but optimism over negotiations outweighed earlier gains.

- US Yields Ease Ahead of Powell’s Jackson Hole Speech: The 2-year Treasury yield fell 2 basis points to 3.752%, while the benchmark 10-year note dipped 3.5 basis points to 4.304%. Investors braced for Federal Reserve Chair Jerome Powell’s speech later this week, which many see as a potential signal for a September rate cut. Fed funds futures now price an 85% chance of a quarter-point reduction.

- Housing Starts Rebound but Permits Decline: US housing starts rose 5.2% in July to an annualised 1.428 million units, well above forecasts of 1.29 million, driven by a surge in new apartment projects. Multi-family starts climbed 11.6% to 470,000 units, the highest since May 2023, with apartment construction up more than 50% in two months. However, permit issuance dropped 2.8% to 1.354 million, a five-year low.

FX Today:

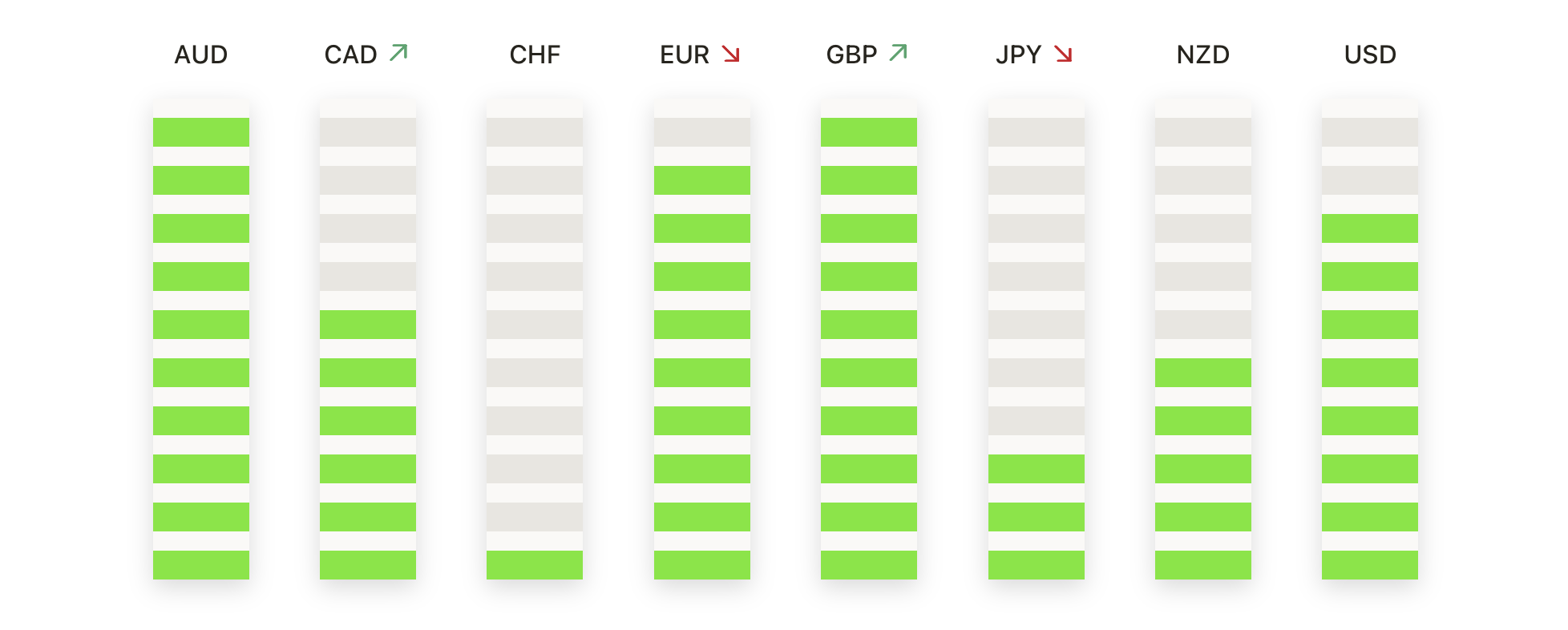

- EUR/USD Slips as Buyers Struggle to Extend Gains: EUR/USD closed at 1.1647, down 0.12% after trading between 1.1639 and 1.1692, with sellers once again capping momentum near the 1.1700 mark. The daily candle printed a modest red body just above the 50-day SMA at 1.1640, reflecting hesitation after last week’s rebound. While the broader backdrop remains constructive, underpinned by the 100-day SMA at 1.1462 and the 200-day at 1.0992, the repeated inability to push through resistance highlights fading momentum. Structurally, the pair continues to hold higher lows since bouncing off 1.1500 in early August, but the consolidation beneath resistance points to a neutral bias in the near term.

- GBP/USD Holds Above Support but Momentum Stalls: GBP/USD settled at 1.3489, down 0.10% after ranging between 1.3478 and 1.3531, with price closing just under the 50-day SMA at 1.3501. The daily action formed a small red candle, reflecting a pause in momentum following the sharp recovery from early August lows. Broader conditions remain mixed, with the 100-day SMA at 1.3402 providing support but upside limited by resistance near 1.3600, the mid-July breakdown zone. The pair has shifted into consolidation as rallies continue to stall, leaving the bias neutral to slightly bearish. Key support rests at 1.3450–1.3420, where the 100-day average is clustered, while a break beneath 1.3420 would re-expose 1.3350 and 1.3300. On the topside, recovery above 1.3600 would clear the way toward 1.3700.

- USD/CAD Extends Higher as Breakout Strengthens Bullish Tone: USD/CAD closed at 1.3866, up 0.46% after trading between 1.3796 and 1.3869, with the session producing a strong green candle that confirmed a clear break above the 100-day SMA at 1.3791. The move built on a base of higher lows from mid-July and shifted momentum firmly back in favour of buyers. The breakout above clustered resistance has tilted bias bullish, though the descending 200-day SMA at 1.4031 now represents the next major hurdle. Immediate support sits at 1.3800–1.3780, with the 50-day average also reinforcing the broader floor at 1.3700. Sustained trade above 1.3870 would maintain upside momentum and target 1.3950 before the 1.4030–1.4050 zone, while a rejection near the 200-day barrier could prompt a retest of broken resistance at 1.3790.

- USD/JPY Consolidates as Resistance Caps Advances: USD/JPY ended at 147.55, down 0.21% after moving between 147.44 and 148.12, with price once again contained beneath the 148.50–149.00 resistance zone. The pair printed a small red candle, signalling continued hesitation as it trades above the 50-day SMA at 146.57 but struggles to extend gains toward the 200-day at 149.19. USD/JPY has been oscillating in a tightening range since early August, with repeated failures to clear overhead barriers highlighting fatigue among buyers. Support is at 147.00–146.50, where the 50-day and rising trendline converge, while resistance remains firm at 148.50–149.20. A breakout above 149.20 would re-energise bulls and expose 150.50, whereas a close beneath 146.50 could trigger a deeper pullback toward 145.00.

- Gold Pulls Back as Sellers Test $3,300 Support Zone: Gold settled at $3,315, down 0.52% after trading between $3,314 and $3,345, with the session closing just above the 100-day SMA at $3,301. The daily candle formed a firm red body, highlighting renewed selling pressure after the failure to sustain above $3,400 in late July. While the longer-term trend remains constructive with the 200-day average at $3,033 still rising, price action in August has carved a series of lower highs, reflecting a corrective phase. The $3,300–$3,285 region is now pivotal as first support, while resistance is capped at $3,345–$3,365. A breakdown beneath $3,285 would risk acceleration lower toward $3,250 and potentially the 200-day base near $3,030, whereas a rebound above $3,365 is needed to reassert bullish momentum.

Market Movers:

- Chipmakers Under Pressure After Downgrade: Advanced Micro Devices slumped more than 5% after GF Securities cut its rating to hold, with Marvell Technology also down more than 5%. ARM Holdings fell over 4%, while Broadcom dropped more than 3% and other semiconductor names including Qualcomm, NXP and Micron all closed lower.

- Biotech Stock Collapses on Trial Concerns: Viking Therapeutics tumbled more than 42% after a Phase 2 trial of its oral weight-loss drug showed high discontinuation rates, with 28% of patients halting treatment due to tolerability issues.

- Fabrinet Warns on Revenue Outlook: Fabrinet plunged over 12% after guiding for a sequential decline in datacom revenues in fiscal Q1, citing supply constraints for critical components.

- Vertiv Sinks on Bearish Initiation: Vertiv Holdings fell more than 4% after GLJ Research began coverage with a sell rating and a $112 price target, sparking profit-taking in the stock.

- Intel Jumps on $2 Billion SoftBank Stake: Intel surged more than 6% to lead S&P 500 and Nasdaq gainers after SoftBank Group agreed to purchase $2 billion of the company’s stock at $23 per share.

Markets ended the day mixed as weakness in technology offset gains in select sectors, with the Dow briefly reaching record territory while the S&P 500 and Nasdaq retreated. Investor focus is now shifting firmly to Jerome Powell’s upcoming remarks at Jackson Hole, seen as pivotal for the outlook on September’s rate decision. European equities advanced but defence shares slid on hopes of progress in Ukraine talks, while Asian markets mirrored Wall Street’s pullback amid fresh signs of pressure in China. With oil prices softening and yields edging lower, positioning across risk assets remains cautious, leaving upcoming economic data and central bank signals as the key drivers for direction in the sessions ahead.