US Markets rose sharply on Monday after Iran’s retaliatory strike against a US base in Qatar caused no casualties, calming fears of a broader Middle East escalation. The Dow jumped nearly 375 points, while the S&P 500 and Nasdaq each gained close to 1%, as investors took the restrained response as a sign of potential de-escalation. Crude oil prices plunged over 7%, erasing weekend gains that had followed US airstrikes on Iranian nuclear sites. US bond yields fell as traders priced in less inflationary pressure from oil and anticipated a possible Fed rate cut in July. European markets ended mixed amid regional PMI data and geopolitical uncertainty, while Asia mostly declined.

Key Takeaways:

- Dow Climbs as Tensions Ease: The Dow Jones Industrial Average rose 375 points, or 0.89%, to end at 42,581.78 on Monday. The index surged after Iran’s strike on a US base caused no casualties, lowering the risk of oil supply disruption.

- S&P 500 Gains Nearly 1% on Oil Drop and Fed Hopes: The S&P 500 advanced 0.96% to close at 6,025.17, supported by a fall in oil prices and renewed optimism for a potential Fed rate cut in July. Broader market breadth was positive with gains across defensive and growth sectors alike.

- Nasdaq Rises on Tech and Tesla Surge: The Nasdaq Composite climbed 0.94% to settle at 19,630.97, helped by strength in large-cap tech stocks and an 8% surge in Tesla shares after its autonomous taxi rollout in Texas. Sentiment also benefited from easing energy inflation fears.

- European Markets Mixed Amid Geopolitics and PMI Disappointment: European markets ended broadly lower on Monday as investors balanced geopolitical worries with disappointing economic data. The Stoxx 600 slipped 0.25%, dragged down by banks, chemicals, and insurers, each down around 1%, while utilities and tech gained. Germany’s flash composite PMI rose to 50.4, returning to growth territory for the first time since April, led by a rebound in manufacturing. However, the euro zone as a whole flatlined, with the services PMI barely above 50 and manufacturing still in contraction. France’s CAC 40 fell 0.68%, Milan’s FTSE MIB dropped 1.00%, and Frankfurt’s DAX declined 0.4%. The FTSE 100 edged down 0.19% to 8,758.04 as cautious sentiment persisted. Spain’s trade deficit widened sharply, adding to the region’s economic uncertainty.

- Asia Mostly Lower Despite Japanese and Chinese Resilience: Asian markets mostly declined on Monday amid renewed geopolitical tension following the US airstrikes on Iran. Japan’s Nikkei 225 slipped 0.13% to 38,354.09 despite upbeat PMI data showing the strongest manufacturing new orders in three years. The Topix fell 0.36% as services strength was offset by softer export demand. South Korea’s Kospi lost 0.24% and the Kosdaq fell 0.85%. Australia’s ASX 200 shed 0.36% as mining stocks declined. Meanwhile, China’s CSI 300 rose 0.29% and Hong Kong’s Hang Seng added 0.67%, with investors encouraged by relative calm in crude prices. India’s Nifty 50 dropped 0.33% and the Sensex fell 0.44% as risk appetite remained constrained.

- Oil Plunges Over 7% as Supply Fears Fade: West Texas Intermediate crude fell $5.33, or 7.22%, to $68.51 per barrel, while Brent dropped $5.53 to $71.48. The pullback came after Iran’s missile strike on a US base in Qatar caused no casualties, easing concerns of an imminent supply shock. Traders also reacted to President Trump’s push for lower oil prices and the apparent failure of Iran to escalate by closing the Strait of Hormuz.

- US Activity Softens While Housing Beats Forecasts: US business activity slowed modestly in June as S&P Global’s composite PMI slipped to 52.8 from 53.0. Price pressures increased, with tariffs blamed for rising input and output costs. At the same time, existing home sales unexpectedly rose 0.8% in May to a 4.03 million annual rate, defying expectations for a decline. Despite the uptick, the sales pace remains the weakest for May since 2009, with high mortgage rates still constraining broader momentum.

- Treasury Yields Fall as Fed Cut Bets Grow: Bond yields fell Monday, with the 10-year note down 3.9 basis points to 4.336%, and the 2-year dropping 6 basis points to 3.848%. Comments from Fed Governor Bowman backing a potential July rate cut, alongside falling oil prices, boosted Treasuries. Bowman joined Waller in suggesting that inflationary effects of tariffs may be limited, supporting easing in the near term.

FX Today:

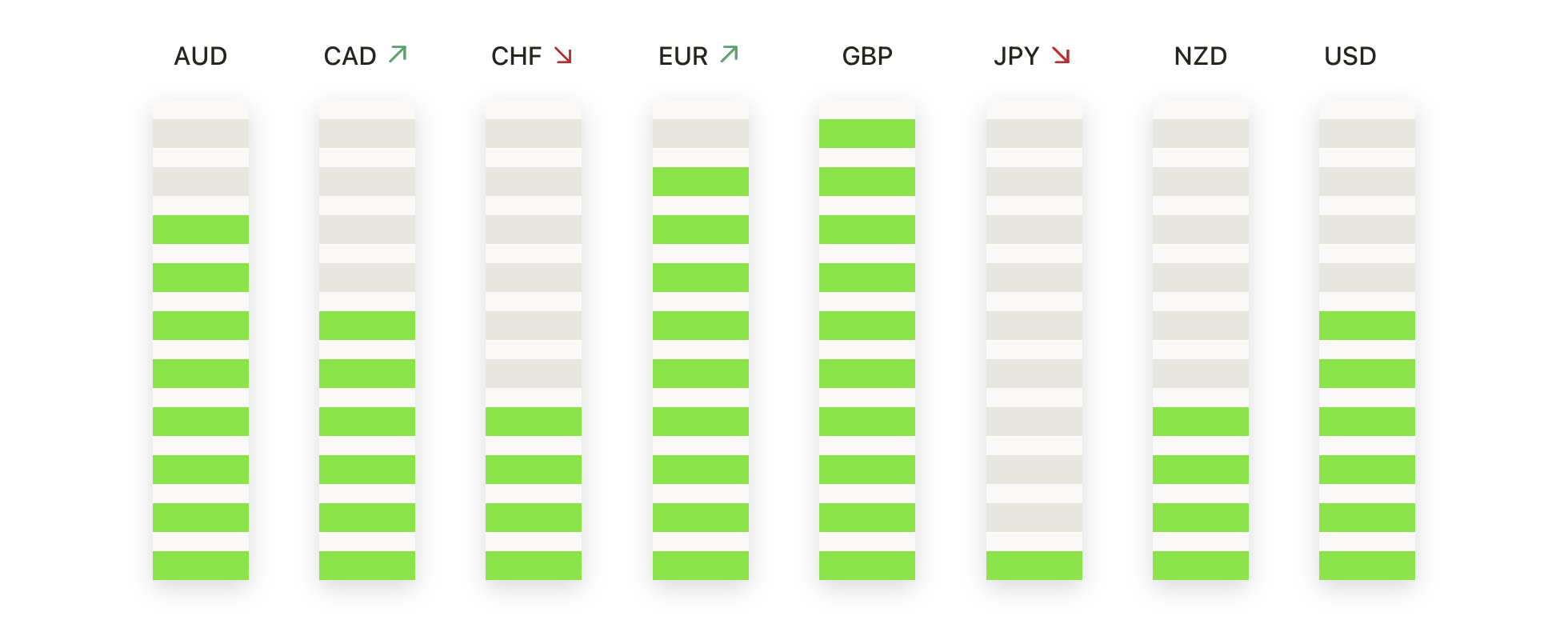

- EUR/USD Holds Firm Above 1.1500 as Bulls Regain Control: EUR/USD closed at 1.1571 on Monday, rising 0.44% after trading between 1.1452 and 1.1577. The pair posted a solid bullish candle after Friday’s mild retracement, with renewed buying emerging above 1.1450. Price continued to consolidate just under key resistance at 1.1600, where several prior rallies have stalled. The move was supported by euro zone PMI data that signalled stabilisation despite underwhelming growth. The pair remains in a well-defined uptrend with support at 1.1450 and 1.1370. EUR/USD is above its 50-day SMA at 1.1364, while the 100-day and 200-day SMAs at 1.1037 and 1.0845 are also sloping upwards, reinforcing bullish structure. A break above the 1.1600–1.1630 resistance zone could open the way to 1.1750. Downside risks remain limited as long as price holds above the 50-day moving average.

- GBP/USD Climbs Toward June Highs as Momentum Builds: GBP/USD settled at 1.3527 on Monday, gaining 0.58% after ranging between 1.3372 and 1.3531. The pair rebounded strongly from support at 1.3400, posting a full-bodied green candle and closing near its session high. Monday’s performance confirmed the continuation of the broader uptrend that has lifted the pound over 10% since February, supported by strong risk appetite and declining oil prices. Technically, the structure remains bullish with higher highs and higher lows. GBP/USD is comfortably above all major SMAs, with the 50-day at 1.3404 providing near-term support. The 100-day and 200-day SMAs at 1.3095 and 1.2933 continue to ascend. Resistance is firm at 1.3625, the June peak, and a breakout could trigger a run toward 1.3700. Holding above 1.3500 is key for preserving the short-term uptrend, while a drop below 1.3400 would signal a possible corrective pullback.

- USD/CHF Slides Below 0.8150 as Downtrend Deepens: USD/CHF ended Monday at 0.8121, falling 0.63% on the day after trading between 0.8115 and 0.8195. The pair extended last week’s decline with a full-bodied red candle closing near the session low, reflecting persistent bearish pressure. Monday’s move breached minor support at 0.8150 and confirmed another lower low in the ongoing channel. Price action remains consistently weak with each bounce capped by falling moving averages. The pair trades below its 50-day SMA at 0.8233, while the 100-day and 200-day SMAs at 0.8535 and 0.8672 continue to trend lower, reinforcing the dominant downtrend. Immediate support lies at 0.8100, followed by 0.8050. A sustained drop below these levels could extend the slide toward 0.8000. Bulls would need to recapture 0.8200 and hold above the 50-day line to shift the tone.

- Gold Holds Steady Below $3,400 After Failing to Break Resistance: Gold closed at $3,376 on Monday, slipping just $2 or 0.08% after trading between $3,347 and $3,398. The precious metal showed signs of consolidation after recent volatility, forming a narrow-bodied candle with wicks on both ends. Traders appeared cautious as geopolitical risks remained elevated yet seemingly contained following the non-lethal Iran strike. The broader trend remains bullish, with gold repeatedly finding support above $3,300. Price continues to hold above its rising 50-day SMA at $3,319, which aligns with a short-term ascending trendline from March. The 100-day and 200-day SMAs, now at $3,139 and $2,897, respectively, further confirm the medium-term uptrend. Resistance remains stiff at $3,400, followed by $3,420, and a break above this band would likely trigger a move toward record highs. On the downside, a firm break below $3,340 could threaten the trend, but so long as price remains above $3,300, bulls retain the upper hand.

Market Movers:

- Tesla Surges on Driverless Taxi Launch: Tesla (TSLA) jumped more than 8% on Monday to lead gains in the S&P 500 and Nasdaq 100 after launching its driverless taxi service to selected riders in Austin, Texas, marking a key milestone in its autonomous vehicle ambitions.

- Northern Trust Rallies on Merger Interest: Northern Trust (NTRS) soared over 8% after the Wall Street Journal reported that Bank of New York Mellon had approached the company to discuss a potential merger, sparking speculation of further consolidation in the financial sector.

- Estee Lauder Upgraded by Deutsche Bank: Shares of Estee Lauder (EL) climbed more than 5% after Deutsche Bank upgraded the stock to “buy” from “hold” and raised its price target to $95, citing improving fundamentals and better valuation outlook.

- Circle Internet Group Extends Crypto Gains: Circle Internet Group (CRCL) advanced over 9%, building on last week’s 65% surge after the US Senate passed legislation establishing a regulatory framework for stablecoins pegged to the US dollar.

- Oil Majors Slide as Crude Plunges: Energy names slumped following a 7% drop in oil prices. APA Corp (APA) fell over 7%, Halliburton (HAL) shed more than 6%, and Diamondback Energy (FANG) and Schlumberger (SLB) declined over 5%. Devon Energy (DVN), Occidental Petroleum (OXY), ConocoPhillips (COP), Baker Hughes (BKR), and Phillips 66 (PSX) lost over 3%, while Exxon Mobil (XOM) and Valero Energy (VLO) dropped more than 2%.

Markets began the week on a strong footing as geopolitical fears subsided following Iran’s restrained missile strike, which caused no casualties. The Dow posted a near-375-point gain, while oil prices plunged over 7%, easing inflation worries and boosting risk sentiment. Treasury yields retreated further after dovish comments from Fed officials suggested a rate cut could come as early as July. While tensions in the Middle East remain a key risk, investors appear reassured by the limited fallout so far. Upcoming economic data, central bank signals, and any escalation around the Strait of Hormuz will now take centre stage in determining the next direction for equities and commodities.