US stocks climbed on Thursday, lifted by encouraging signs from the labour market and consumer spending, alongside another wave of stronger-than-expected corporate earnings. The S&P 500 and Nasdaq both registered new all-time closing highs, continuing this year’s upward momentum. Investors were reassured by fresh retail sales and jobless claims data, which painted a picture of a resilient economy. Meanwhile, corporate results from major names exceeded expectations, helping to lift sentiment across sectors. The broader mood was further stabilised following Wednesday’s political drama surrounding Federal Reserve leadership.

Key Takeaways:

- S&P 500 Posts Ninth Record Close: The index climbed 0.54% to 6,297.36, marking its ninth all-time closing high of 2025. Optimism around earnings and macro data helped offset recent political nerves, with over 88% of companies reporting so far beating estimates.

- Nasdaq Scores Tenth Record of the Year: The Nasdaq Composite advanced 0.74% to 20,884.27, logging its tenth record close of 2025. Tech shares led the rally amid upbeat earnings reports and signs of solid consumer activity.

- Dow Climbs as Broader Market Gains Traction: The Dow Jones Industrial Average rose 229.71 points, or 0.52%, to close at 44,484.49. The blue-chip index rebounded from earlier volatility, supported by strong performances from names like Travelers and PepsiCo.

- European Markets Rally on Earnings and Inflation Data: European indices closed sharply higher, erasing losses from earlier in the week after a flurry of earnings boosted sentiment. The STOXX 50 jumped 1.6% to 5,370 while the STOXX 600 rose 1% to 547.22. France’s CAC 40 gained 1.29%, Germany’s DAX rose 1.51%, and Italy’s FTSE MIB climbed 0.92%. The UK’s FTSE 100 added 0.52% to 8,972.64. The euro area’s annual core inflation held steady at 2.3% in June, while headline inflation ticked up to 2%. Meanwhile, UK employment data painted a weaker picture as payrolled jobs fell by 41,000 in June and unemployment rose to 4.7%. Wage growth slowed slightly to 5% amid pressure from higher labour costs and minimum wage increases.

- Asia-Pacific Markets Mostly Advance Despite Japan Trade Slump: Asian equities ended broadly higher as investors weighed disappointing trade figures from Japan against stabilising global sentiment. Japan’s Nikkei 225 rose 0.6% to 39,901.19, and the Topix added 0.72%, despite a 0.5% fall in June exports. Shipments to the US and China continued to decline, reflecting weak external demand. South Korea’s Kospi added 0.19%, while the Kosdaq rose 0.74%. Australia’s ASX 200 gained 0.9%, even as unemployment rose to 4.3%, its highest since 2021. Net employment increased by just 2,000, well below forecasts. China’s CSI 300 rose 0.68%, while Hong Kong’s Hang Seng closed flat. India’s Nifty 50 and Sensex edged lower, while Singapore’s STI extended its winning streak to a ninth session, touching a record high of 4,154.13 intraday.

- Oil Prices Rise on Middle East Risk and Tight Supply: Brent crude rose $1.03 to $69.55, while WTI climbed $1.22 to $67.60. US stockpiles dropped by 3.9 million barrels last week, far exceeding forecasts, while renewed tensions in northern Iraq disrupted production by up to 150,000 barrels per day. The combination of geopolitical risk and tighter inventories supported the rally, while expectations for improved US-China trade relations also contributed to bullish sentiment.

- US Retail and Labour Data Reinforce Growth Outlook: Fresh data on Thursday indicated solid economic momentum in the United States. Initial jobless claims fell to 221,000, down 7,000 from the prior week, pointing to continued labour market strength. Meanwhile, retail sales in June rose 0.6%, triple the expected gain. Core retail sales rose 0.5%, supporting estimates for stronger second-quarter GDP. Auto, clothing and building material sales led the gains, while online and hobby-related spending also increased. The figures suggest consumers remain engaged, providing a solid base for growth despite mixed signals earlier this year.

FX Today:

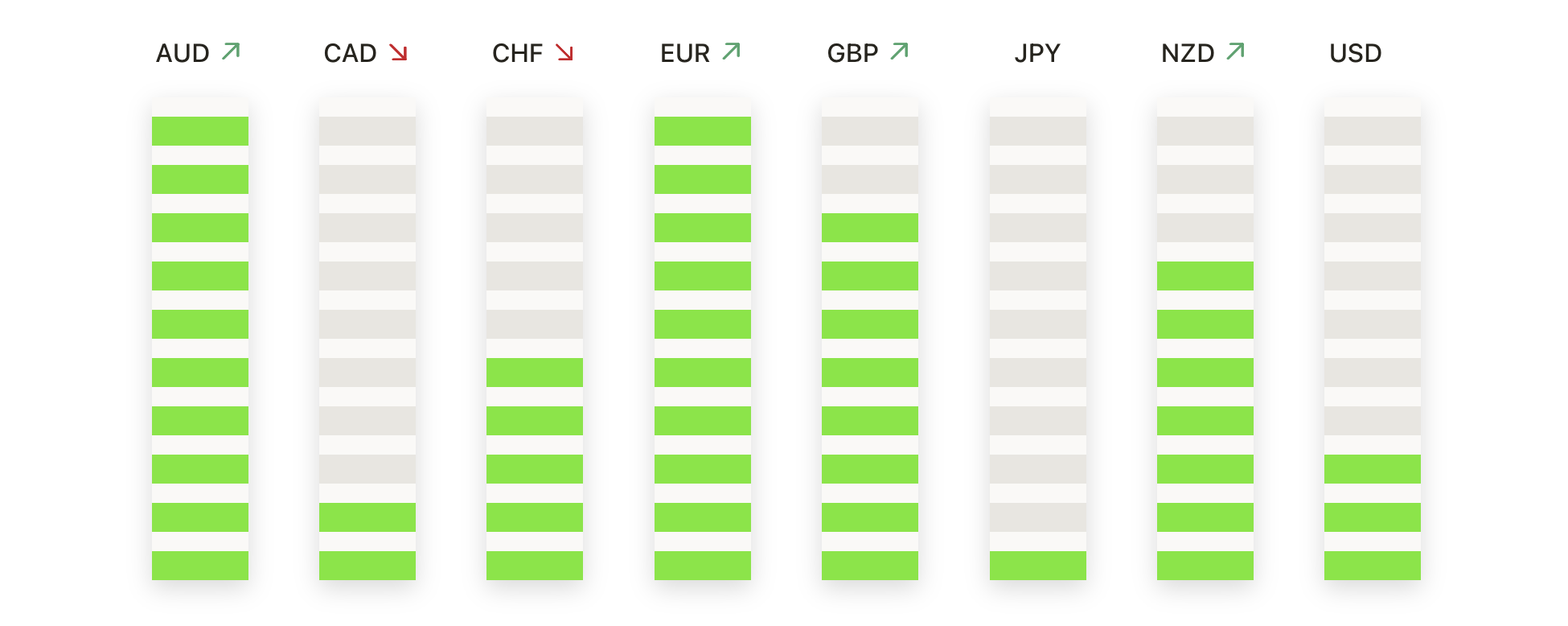

- EUR/USD Slides as Bearish Pressure Builds: The EUR/USD pair closed at 1.1599, falling 0.37% after reaching a high of 1.1643 and a low of 1.1557. This marked the fourth straight daily decline, with the candle forming a firm-bodied red bar near the session low. The drop extended the pair’s retreat from the July high near 1.1880, where bulls lost momentum. Price is approaching 1.1492, which marks a key support level. A break beneath this zone could expose the 100-day SMA near 1.1267. Resistance remains at 1.1650, with stronger barriers around 1.1750. For now, the downside remains in focus unless buyers can regain control above 1.1500.

- GBP/USD Holds Above Key Support After Sharp Pullback: The GBP/USD pair settled at 1.3418, slipping just 0.02% after printing a high of 1.3428 and a low of 1.3374. The session’s small-bodied candle reflected consolidation following the recent pullback from the multi-month high near 1.3850. Price held above the 100-day SMA, while the 50-day SMA overhead at 1.3505 capped further upside. The zone between 1.3370 and 1.3400 has emerged as near-term support, and bulls will look to defend this region to retain structure. A break below would shift attention to the 100-day average at 1.3282.

- USD/JPY Rally Continues as Price Eyes 200-Day SMA: USD/JPY rose 0.47% to close at 148.57 after touching a high of 149.09 and a low of 147.73. The pair extended its winning streak to six sessions, decisively reclaiming the 100-day SMA at 145.76 and pushing towards the 200-day SMA near 149.60. The rebound from April’s low near 139.00 remains intact, and the pair continues to post higher highs and higher lows. A confirmed breakout above 149.60–150.00 could set the stage for a test of 151.00. Initial support is now seen at 147.30, with further backing from the 100-day SMA.

- USD/CHF Clears Resistance at 0.8000 as Bulls Regain Control: USD/CHF closed at 0.8039, rising 0.51% after posting a high of 0.8064 and a low of 0.7993. The pair broke decisively above the 0.8000 psychological barrier, ending a multi-week consolidation phase. The move confirmed a bullish breakout and suggested a reversal from the July low near 0.7850. Price has reclaimed the 20-day moving average and is forming higher lows, although the falling 50-day SMA at 0.8143 remains a hurdle. Immediate resistance is seen at 0.8100, while support lies at 0.7990 and 0.7930. As long as the pair holds above 0.8000, the path of least resistance remains upward.

- AUD/USD Breaks Lower with Bearish Reversal Signal: The AUD/USD pair dropped 0.58% to finish at 0.6489, retreating from a high of 0.6530 and hitting a low of 0.6454. The inability to sustain levels above 0.6550 earlier this week adds to the negative tone. Momentum has clearly shifted, with the 20-day average flattening and suggesting downside pressure. If weakness extends, support levels come in at 0.6403 (100-day SMA) and then 0.6350. Bulls need to reclaim 0.6525 and 0.6563 to revive the uptrend.

- Gold Holds Near $3,340 Amid Directionless Trade: Gold closed slightly lower at $3,339, down 0.26%, after moving between $3,352 and $3,310. Price is consolidating above the 50-day SMA at $3,325, which has provided reliable support in recent sessions. The 100-day SMA at $3,210 remains the next major floor. On the upside, resistance continues at $3,360, with broader range highs near $3,445 acting as a cap. While the long-term trend remains upward, gold has lacked bullish momentum since peaking near $3,480 in June. A breakout above $3,360 or below $3,310 will be needed to establish fresh direction.

Market Movers:

- United Airlines Rises as Outlook Improves: Shares of United Airlines gained more than 3% after CEO Scott Kirby said the second half of the year had become more predictable, citing upside potential to beat earnings targets as consumer travel demand remained strong. The positive commentary lifted the broader airline sector, with Alaska Air and American Airlines both rising over 3%, while Delta added more than 1%.

- PepsiCo Jumps on Strong Earnings Beat: PepsiCo surged more than 7% to lead gains in the Nasdaq 100 after reporting second-quarter net revenue of $22.73 billion, beating analyst expectations of $22.32 billion.

- Snap-on Advances on Sales Surprise: Snap-on climbed more than 7% after posting second-quarter net sales of $1.18 billion, exceeding consensus estimates of $1.16 billion.

- Elevance Health Sinks on Guidance Cut: Elevance Health dropped 12% to lead S&P 500 decliners after slashing its full-year earnings outlook to around $30 per share, well below its previous range of $34.15 to $34.85.

- Sonic Automotive Slides on JPMorgan Downgrade: Sonic Automotive tumbled 10% after JPMorgan downgraded the stock to ‘underweight’ from ‘overweight’, setting a price target of $72. Analysts flagged margin pressure and sector rotation as headwinds.

- Abbott Laboratories Drops on Soft Guidance: Abbott fell more than 8% after reporting Q2 organic sales growth of 6.9%, below the 7.03% consensus. The company also issued full-year guidance below analyst forecasts, prompting a wave of downgrades.

Equities extended their rally on Thursday, with record closes for both the S&P 500 and Nasdaq underscoring renewed investor confidence. Strong earnings results and a solid batch of economic data, particularly on retail sales and the labour market, reinforced optimism about the consumer-led expansion. European and Asian markets also reflected improved sentiment, while oil prices climbed on geopolitical risk and tighter inventories. As earnings season continues and macro signals remain broadly supportive, attention now shifts to upcoming guidance from major corporates and fresh inflation data in the weeks ahead.