US equities delivered a mixed performance as the new month began, with the Nasdaq rising while the Dow lagged, reflecting an increasingly concentrated market driven by large-cap AI and cloud leaders. Strong gains in Amazon and chipmakers helped lift sentiment around artificial intelligence infrastructure demand, following new multi-billion-dollar partnership announcements across the sector. However, the broader market showed signs of strain, with weak internal breadth and limited participation outside technology, highlighting the ongoing divergence between megacap AI beneficiaries and the rest of the equity market landscape.

Key Takeaways:

- Nasdaq Advances as AI Leaders Drive Gains: The Nasdaq Composite rose 0.46% to 23,834.72, supported by renewed strength across large-cap tech and AI-linked names. Amazon led the move after confirming a $38 billion cloud partnership with OpenAI.

- S&P 500 Edges Higher While Dow Declines: The S&P 500 added 0.17% to 6,851.97, while the Dow Jones Industrial Average fell 0.48% to 47,336.68. More than 300 S&P 500 stocks finished in the red, highlighting narrow leadership concentrated in just a handful of large tech companies.

- Dow Slips on Weak Breadth: The Dow underperformed, dropping 226 points or 0.48% to 47,336.68 as decliners outpaced gainers and pressure from index heavyweights weighed on performance. Losses included Merck down 4.1% and Nike off 3.0%, while 3M, Chevron and UnitedHealth fell 2%, underscoring the day’s defensive drag outside of technology leadership.

- European Markets Mixed as Manufacturing Shows Little Momentum: European markets began the new month with a generally positive performance. The pan-European Stoxx 600 edged up by 0.07%, while Germany’s DAX Index gained 0.73%, and Italy’s FTSE MIB advanced 0.1%. Conversely, the UK’s FTSE 100 Index declined by 15.88 points, closing at 9701.37, and France’s CAC 40 also saw a modest decrease of over 0.14%. Economic data from the Eurozone indicated manufacturing activity stagnated in October, with the HCOB Eurozone Manufacturing PMI registering 50.0, precisely at the growth threshold. New orders stayed subdued, and export orders declined, although production saw slight expansion. Performance varied regionally, with Greece and Spain showing improvements, while Germany and France remained in contraction. British factories experienced their strongest month in a year, with the S&P Global PMI rising to 49.7, largely attributed to a one-off bounce from Jaguar Land Rover’s production restart.

- Asia-Pacific Markets Mostly Higher Despite Weaker China PMI: Most Asia-Pacific markets recorded gains, building on Wall Street’s positive close from the prior session, although investor sentiment was tempered by Chinese manufacturing data. China’s RatingDog Purchasing Managers’ Index for October registered 50.6, falling short of economists’ expectations of 50.9 and lower than September’s 51.2. This followed official figures released earlier that showed Chinese manufacturing activity contracting to a six-month low of 49.0. Despite this, Hong Kong’s Hang Seng index rose 0.97% to 26,158.36, breaking a three-day losing streak, and mainland China’s CSI 300 reversed earlier losses to climb 0.27%, closing at 4,653.4. South Korea’s Kospi surged 2.78% to a new record high of 4,221.87, marking its largest single-day gain since June, with the small-cap Kosdaq also up 1.57%. India’s Nifty 50 saw a 0.14% increase, while the Sensex traded near the flatline. Australia’s S&P/ASX 200 advanced 0.15% to 8,894.8, with Westpac Banking Corporation climbing 2.8% despite reporting a decline in annual profit. Mixed economic data in Australia, including a fall in ANZ-Indeed Job Ads and a rise in the Monthly Inflation Gauge, preceded the central bank’s monetary policy decision. Japanese markets remained closed for a public holiday.

- Oil Holds Steady as OPEC+ Pauses Output Increases: Oil prices recorded slight gains as OPEC+ announced plans to halt supply increases. Brent crude futures rose by 7 cents, or 0.11%, to settle at $64.84 per barrel, while US West Texas Intermediate crude also gained 7 cents, or 0.11%, closing at $61.05. The alliance agreed to lift output by a modest 137,000 barrels per day in December before pausing further increases in the first quarter of next year, signalling recognition of the expected surplus early next year. Both Brent and WTI fell more than 2% in October, marking a third consecutive monthly decline and briefly touching five-month lows.

- US Manufacturing Weakness Persists: The US manufacturing sector continued to show signs of weakness, contracting for the eighth consecutive month in October. The Institute for Supply Management (ISM) reported that its manufacturing Purchasing Managers’ Index (PMI) declined to 48.7, down from 49.1 in September, indicating a persistent contraction as any reading below 50 signifies a downturn. While the PMI stayed above 42.3, a level historically associated with overall economic expansion, the sector faces headwinds.

- Treasury Yields Little Changed as Shutdown Drags On: The 10-year Treasury yield was near flat at 4.107%, with the 2-year at 3.598% and the 30-year at 4.683% as the US government shutdown reached 34 days, one short of the 35-day record. With several federal data releases delayed, investors are looking to ADP private payrolls midweek for labour-market clues ahead of Friday’s jobs report.

FX Today:

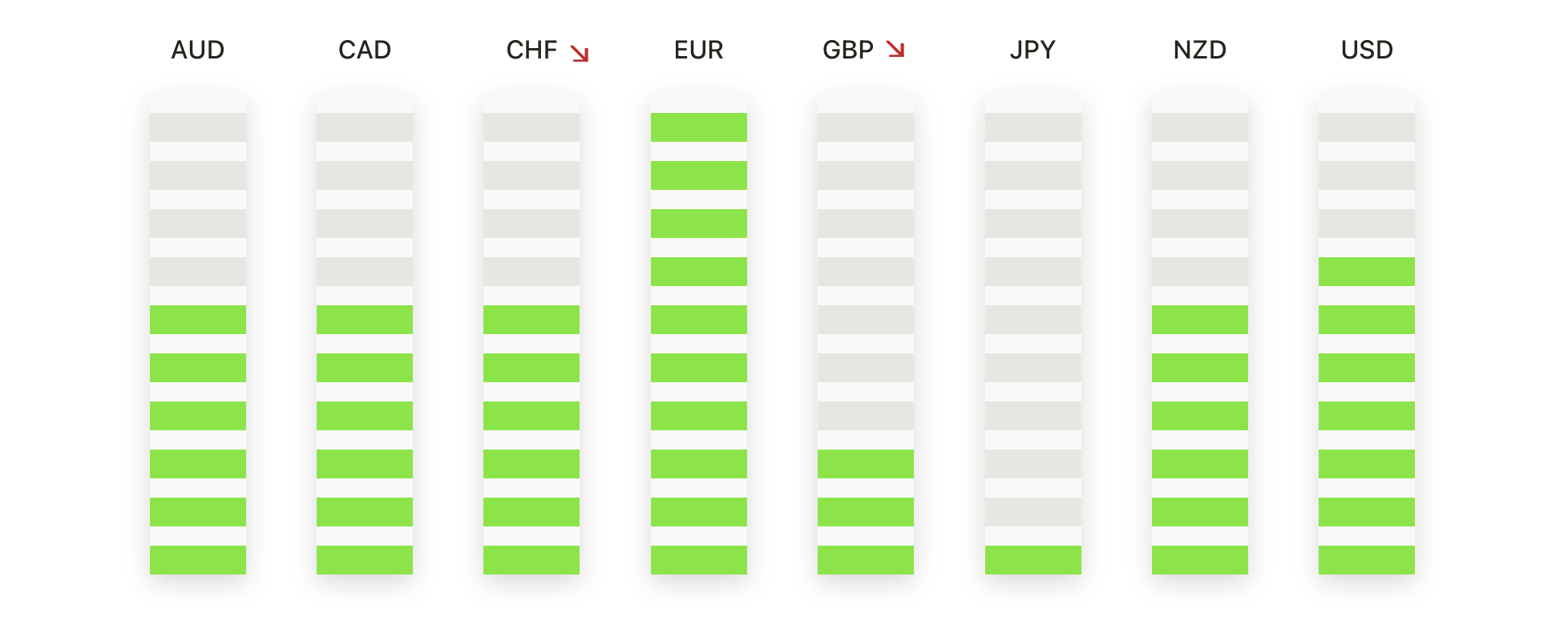

- EUR/USD Slips Toward Mid-August Floor: EUR/USD closed at 1.1519, down 0.15%, after trading between 1.1541 and 1.1505. The pair remains below the 50-day SMA at 1.1680 and the 100-day SMA at 1.1664, reinforcing a bearish near-term bias, although it continues to hold above the 200-day SMA at 1.1323. The structure has been defined by lower highs and lower lows since mid-October, pointing to persistent selling pressure. The 1.1506 level marks immediate support, with the psychological 1.1500 area just below. Resistance sits at 1.1541, followed by the confluence of the 50-day and 100-day SMAs.

- GBP/USD Fades Below Long-Term Averages: GBP/USD closed at 1.3138, down 0.10%, after moving between 1.3162 and 1.3108. The pair is trading below the 200-day SMA at 1.3252, as well as the 50-day SMA at 1.3427 and the 100-day SMA at 1.3460, confirming a firmly bearish alignment across all timeframes. The short-term and medium-term trends are clearly bearish, marked by a sequence of lower highs and lower lows since the peak in July. Immediate resistance is now found at 1.3162, followed by the significant overhead barrier posed by the broken 200-day SMA at 1.3252. Initial support is at 1.3108, with further support seen around the 1.3050 region. If the pair can reclaim and hold above 1.3162, it could signal a temporary pause in the downtrend, allowing for consolidation.

- USD/CAD Pushes Higher After 200-Day Break: USD/CAD closed at 1.4052, up 0.36%, after trading between 1.4076 and 1.3991. The pair is now trading above all three key moving averages, having recently crossed above the 200-day SMA at 1.3944, positioning it above the 50-day SMA at 1.3904 and the 100-day SMA at 1.3815. Immediate resistance is observed at 1.4076, representing the recent high, with the next potential target around the 1.4100 psychological level. Initial support is found at 1.3991, followed by the 200-day SMA at 1.3944. If the pair maintains its position above 1.3991, further momentum to 1.4100 and beyond is plausible.

- USD/JPY Stretches Rally Into New Highs: USD/JPY closed at 154.19, up 0.12%, after trading between 154.30 and 153.88. The candle displays a solid bullish session, pushing to new multi-year highs and closing near the upper end of its daily range, indicating strong underlying buying pressure. The pair is trading significantly above all three key moving averages: the 50-day SMA at 148.58, the 100-day SMA at 148.21, and the 200-day SMA at 147.72, which confirms a robust and well-established uptrend across all timeframes. The continuous advance indicates strong bullish momentum. Immediate support is identified at 153.88, with following support at 153.00.

- Gold Holds Above $4,000 After Brief Dip: Gold closed at $4,010, up 0.19%, after trading between $4,031 and $3,962. The price remains comfortably above the 50-day SMA at $3,831, the 100-day SMA at $3,590, and the 200-day SMA at $3,338, maintaining a strong longer-term bullish trend. The defence of the $3,960 area suggests renewed buy-side interest following recent corrective pressure. Immediate resistance lies at $4,031, with further upside interest near $4,060. Initial support is seen at $3,962 and then around $3,900. Holding above $3,962 keeps the near-term recovery outlook intact ahead of key US employment data.

Market Movers:

- Amazon Rallies on OpenAI Cloud Agreement: Amazon shares rose 4.0% after the company announced a $38 billion deal to provide AI cloud capacity to OpenAI through AWS.

- Nvidia Advances as Outlook Strengthens: Nvidia gained 2.2% after receiving a Street-high price target upgrade, supported by expectations of sustained growth in data centre GPU demand.

- Crypto-Linked Stocks Slide on Bitcoin Pullback: Coinbase fell 3.9%, Marathon Holdings eased 2.5%, and MicroStrategy slipped 1.8% as Bitcoin retreated, although Riot Platforms diverged from the trend and closed higher by 4.8%.

- Iren Surges on Microsoft AI Data Centre Deal: IREN LTD rallied over 11% after securing a multi-year agreement with Microsoft valued at nearly $10 billion to supply AI data centre capacity.

- Kenvue Jumps Following Takeover Announcement: Kenvue rose 12% after Kimberly-Clark agreed to acquire the consumer-health company for nearly $50 billion.

US markets opened November with a continuation of the year’s defining theme: meaningful leadership concentrated within the largest AI and cloud infrastructure names while broader participation remains limited. Strength in Amazon, Nvidia and related semiconductor names underscored ongoing demand for computing capacity and next-generation data centre build-outs, even as weakness in the Dow and mixed sector performance highlighted the market’s narrowing breadth.