US stocks ended mixed on Monday, but optimism over earnings helped the Nasdaq and S&P 500 notch fresh milestones. The S&P 500 closed above the 6,300 level for the first time, while the Nasdaq Composite finished at a new record high, fuelled by strength in major technology shares. Alphabet and Meta led the gains as investors bet on strong results from the “Magnificent Seven” in the days ahead. While the Dow edged slightly lower, broader sentiment remained upbeat with more than 85% of companies beating forecasts so far this season.

Key Takeaways:

- S&P 500 Breaks 6,300 Barrier for First Time: The S&P 500 rose 0.14%to close at 6,305.60, marking its first ever finish above the 6,300 level. The index also touched a fresh intraday high earlier in the session, signalling sustained upward momentum as investors looked ahead to results from Alphabet and Tesla.

- Nasdaq Closes at New Record as Tech Leads Gains: The Nasdaq Composite jumped 0.38% to end at a record 20,974.17, supported by strong performances from Alphabet, Meta and Amazon. Optimism surrounding the Magnificent Seven outweighed caution around trade tensions, with Alphabet climbing over 2% ahead of its results due Wednesday.

- Dow Slips Slightly as Broader Market Holds Steady: The Dow Jones Industrial Average dipped 19.12 points or 0.04% to finish at 44,323.07 as weakness in select names offset strength in Verizon and chip stocks. Despite the modest decline, the underlying sentiment remained constructive with early earnings reports showing strong beats and upward guidance.

- European Stocks Mixed as UK Data Disappoints and Tariff Fears Linger: European markets traded cautiously on Monday, weighed by ongoing uncertainty over US tariffs on the EU and soft macro data from the UK. The Stoxx Europe 600 edged down 0.1% to 546.59 while Germany’s DAX closed just above the flatline at 24,310. France’s CAC 40 fell 0.3% and Italy’s FTSE MIB shed 0.4%. The FTSE 100 bucked the trend, gaining 0.23% to 9,012.99, though gains were capped by rising domestic worries. UK consumer sentiment recorded its sharpest monthly fall in nearly three years amid stubborn inflation and a slowing labour market. Unemployment rose to 4.7%, the highest since 2021, adding pressure ahead of the Bank of England’s next decision. Meanwhile, a European Central Bank survey noted resilient business confidence but falling profitability as trade tensions mount. Markets now await the ECB’s meeting later this week, with rates expected to be held steady at 2.0 %.

- Asia Ends Mostly Higher as China Holds Rates and Japan Extends Gains After Election:

Asia-Pacific markets close mostly higher on Monday, with Japan leading gains following a weekend election outcome that boosts investor expectations for economic support. The Nikkei 225 rises 0.35% to 39,958.24, extending its recovery as traders position for potential fiscal easing after Prime Minister Ishiba’s ruling coalition loses ground in the upper house. While the result falls short of a political crisis, it raises pressure on the government to accelerate growth measures. In China, the PBOC keeps its 1- and 5-year loan prime rates unchanged, helping the CSI 300 advance 0.67%. Hong Kong’s Hang Seng Index climbs 0.68%, supported by a softer inflation reading, as June CPI slows to 1.4% from 1.9% in May. South Korea’s Kospi gains 0.71%, while the Kosdaq adds 0.12% despite weaker trade data. India’s Nifty 50 and Sensex both close higher by 0.43% and 0.37%, respectively. Singapore’s Straits Times Index continues its winning streak, reaching a new all-time high at 4,225.79. - Oil Little Changed Despite EU Sanctions and US Tariff Risks: Oil prices were marginally lower, with Brent slipping 0.4% to 69.00 dollars and WTI falling 0.49% to 67.01 dollars. The EU’s eighteenth sanctions package on Russia targeted refined products processed in third countries, though analysts warned enforcement would be difficult. US threats to penalise Russian oil buyers added to demand concerns, while the number of active US rigs dropped to the lowest since 2021, suggesting possible supply softening.

- US Treasury Yields Fall as Growth Concerns Return: The 10-year Treasury yield dropped over 4 basis points to 4.384% while the 2-year fell to 3.861% and the 30-year declined to 4.95%. A 0.3% fall in the Leading Economic Index, more than expected, signalled weaker momentum. The Conference Board now expects GDP to slow to 1.6% in 2025 with higher tariffs weighing on consumption in the second half.

FX Today:

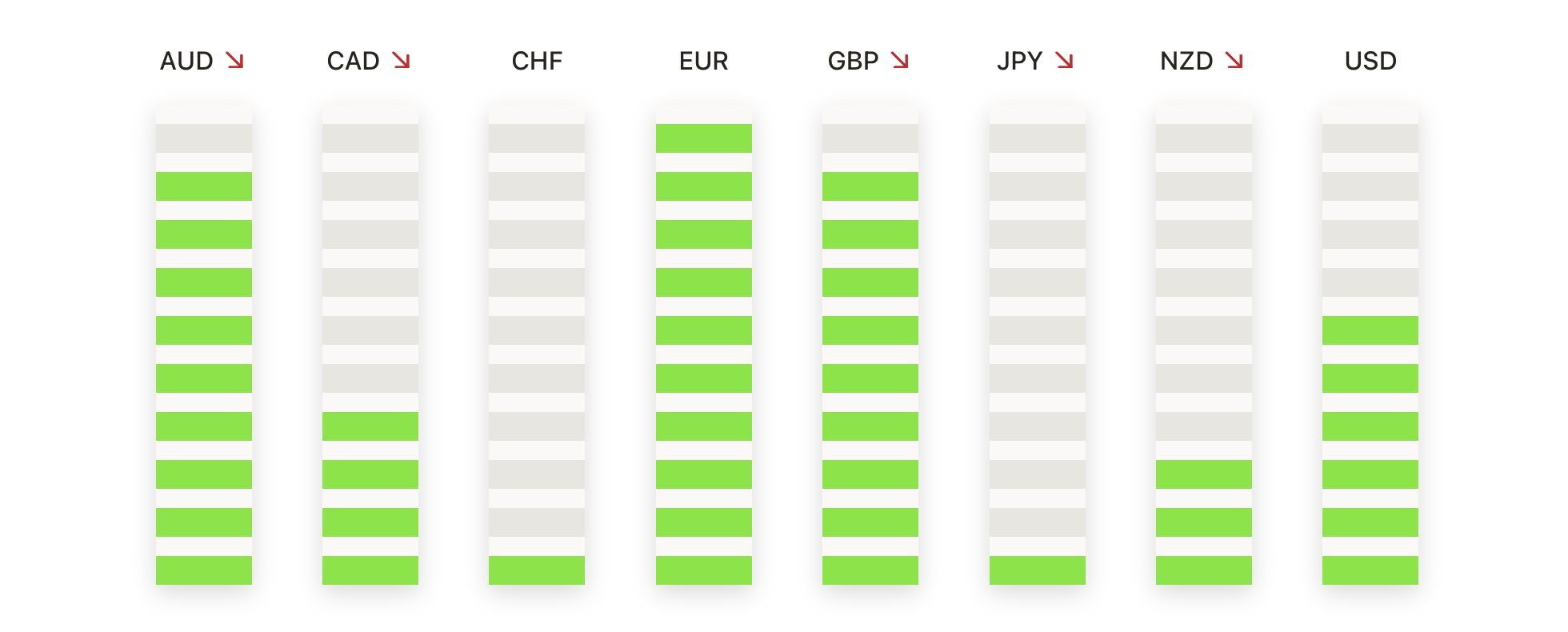

- EUR/USD Edges Toward 1.1700 as Buyers Regain Upper Hand: The euro rebounded on Monday, lifting EUR/USD by 0.59% to 1.1691 as bullish momentum returned following last week’s dip. The pair carved out a decisive move away from the 1.1600 area and is now challenging overhead resistance near 1.1720. Price action has turned constructive once more, supported by a series of higher lows and strong demand at the 50-day SMA around 1.1510. Both the 100-day and 200-day moving averages sit well below current levels, confirming that the broader trend remains positive. Technical signals show improving momentum with no signs of exhaustion. A sustained break above 1.1750 would reinforce the rally and put the late-June high of 1.1870 in sight. On the downside, the 1.1620 zone offers initial support, followed by stronger interest near 1.1500 if any deeper pullback unfolds.

- GBP/USD Breaks Above 1.3450 as Uptrend Reasserts: Sterling gained ground for a second session, with GBP/USD finished at 1.3487, rising 0.59% as dip-buyers stepped back in above the 100-day moving average. The pair bounced confidently from last week’s lows and is now pushing up against the 50-day SMA near 1.3513, which has acted as a ceiling this month. If buyers can clear that hurdle, the next test will likely be the 1.3600 region. Momentum indicators have shifted higher, reflecting a change in tone after the recent pullback from 1.3800. Support is layered between 1.3400 and 1.3330. The broader structure remains bullish with rising long-term averages and upward momentum returning.

- USD/JPY Falls Below 148.00 as Sellers Take Control: The dollar slipped sharply against the yen, with USD/JPY closed at 147.33, sliding 0.98% after failing to sustain gains above 149.00. Price was trading below the 100-day SMA and edging closer to the 50-day average near 145.15, which may offer the next layer of support. The recent rally from 145.00 to nearly 150.00 appears to have stalled, and the inability to reclaim the 200-day average around 149.60 reinforces the short-term bearish shift. If pressure builds, sellers could drive the pair toward 144.20 or even 143.00. Recovery attempts are likely to be capped at 148.00 and 149.00.

- Gold Rallies Toward 3,400 as Buyers Drive Breakout Attempt: Gold surged on Monday, gaining 1.47% to settle at 3,398 after breaking decisively above a cluster of resistance near 3,350. The move followed several sessions of sideways action and confirmed that demand remains strong above the 50-day SMA, currently rising from 3,324. Monday’s close landed just beneath the session high of 3,401, placing the 3,400 level within reach for a potential breakout. A daily close above 3,400 would likely trigger a run toward the record high near 3,431. In the near term, support is expected around 3,375 and the 50-day SMA. Any pullback into this region is likely to attract dip buyers given the strong technical bias.

- Silver Pushes Above 39.00 as Momentum Builds: Silver advanced 1.95% to 38.89 on Monday, notching its best close in over six weeks after clearing a key ceiling at 38.50. The move confirmed a bullish breakout and extended the metal’s July rally, which has now lifted price by more than 10% from early-month lows. Silver briefly touched 39.05 intraday before easing slightly into the close, leaving 39.80 and 40.00 as the next upside targets. All major moving averages continue to rise, with the 50-day currently offering a dynamic base near 35.40. Technical structure remains constructive, and former resistance zones at 38.00 and 37.40 are now likely to act as support. While some profit-taking may emerge near 40.00, the underlying bias stays firmly positive unless the price drops back below 38.50.

Market Movers:

- Block Jumps After S&P 500 Inclusion Announcement: Block (XYZ) surged more than 7% after S&P Dow Jones Indices said the company will replace Hess Corp in the S&P 500 before Wednesday’s open, driving strong institutional buying.

- Verizon Rallies on Raised Earnings Forecast: Verizon Communications (VZ) climbed over 4% to lead gains in both the Dow and S&P 500 after the firm lifted the lower end of its full-year profit outlook from 0 to 1 percent, citing stronger than expected performance in Q2.

- ARM Holdings Leads Chip Rally: ARM Holdings (ARM) rose more than 3% as strength in semiconductor names lifted the broader tech sector. Qualcomm, NXP Semiconductors, Broadcom, Lam Research and Applied Materials all gained over 1 percent.

- Natural Gas Stocks Slide with Futures: EQT Corp (EQT) plunged more than 9% as natural gas futures dropped over 6% to a one-week low. Antero Resources, Expand Energy, Cheniere Energy and Coterra Energy all posted losses of more than 5 percent.

- Sarepta Falls on Safety Concerns: Sarepta Therapeutics (SRPT) declined over 5% after reports linked three patient deaths to its Elevidys gene therapy treatment, prompting questions about the company’s risk disclosures.

Equity markets showed resilience on Monday as optimism surrounding tech earnings helped offset trade worries and disappointing UK data. The Nasdaq surged to a record close while the S&P 500 broke above 6,300 for the first time, reflecting strong investor confidence in the earnings season. Though the Dow edged slightly lower, sector breadth remained positive, led by chipmakers and consumer names. In Europe, tariff uncertainty and soft economic figures weighed on sentiment, while Asia saw widespread gains on policy stability and solid regional data.