US equities closed mixed as renewed pressure in chip stocks weighed on the Nasdaq, while broader earnings strength supported gains in the Dow and S&P 500. Semiconductor shares fell sharply following reports of delays in a high-profile AI initiative, dragging major tech names lower and ending the Nasdaq’s winning streak. In contrast, healthcare stocks rallied after strong results from IQVIA, helping to offset disappointing updates from defence and consumer names. Broader market sentiment remained cautious ahead of key earnings from major tech firms, with investors also monitoring trade developments and central bank expectations.

Key Takeaways:

- S&P 500 Marks 11th Record as Broader Market Rotates: The S&P 500 edged up 0.06% to 6,309.62, supported by gains in healthcare and small caps. A broad rotation out of technology helped keep the index in positive territory despite fading momentum ahead of major earnings releases later this week.

- Dow Rises on Strong Earnings from Health and Defence: The Dow climbed 0.40% to 44,502.44, boosted by a rally in healthcare names and defence contractors. IQVIA surged nearly 18% following an earnings beat, while Northrop Grumman gained over 9% after raising its full-year profit outlook.

- Nasdaq Falls as Chip Stocks Drag Index Lower: The Nasdaq dropped 0.39% to 20,892.69, ending a six-session winning streak. Chipmakers sold off after reports that a $500 billion AI initiative by SoftBank and OpenAI had been scaled back, pulling down Nvidia, Broadcom, and Taiwan Semiconductor.

- Europe Extends Losses Amid Earnings and Trade Anxiety: The Stoxx 600 declined 0.41% for a third consecutive session, led by a 1% fall in Germany’s DAX to 24,050. France’s CAC 40 dropped 0.7% to 7,744, while the FTSE 100 edged up 0.12% to 9,023.81. UK borrowing rose to £20.7 billion in June as inflation drove interest costs to their third-highest monthly level since records began. Food price inflation accelerated to 5.2%, putting pressure on consumers and adding to speculation over future tax changes.

- Asia-Pacific Markets Close Mixed on Policy and Political Risk: Asian equities delivered mixed results as markets weighed global earnings sentiment, central bank guidance, and local political developments. Hong Kong’s Hang Seng rose 0.54% and China’s CSI 300 climbed 0.82%, while Japan’s Nikkei slipped 0.11% following election uncertainty. South Korea’s Kospi dropped 1.27% as producer prices rose 0.5% year-on-year, and Australia’s ASX 200 added 0.1% after RBA minutes confirmed a split vote on rate policy.

- Oil Declines for Third Session on Trade Tensions: Brent crude fell 0.9% to settle at $68.59 per barrel, while WTI lost 1.47% to close at $66.21. Concerns over slowing demand due to US-EU tariff tensions pressured prices for a third consecutive day, with the September WTI contract also slipping 0.7% to $65.48.

- Bond Yields Ease Ahead of Key Fed Meeting: The 10-year US Treasury yield declined to 4.342% as investors positioned ahead of next week’s Fed decision. The 2-year yield fell to 3.833% and the 30-year dropped to 4.911%, with futures pricing in a near-certainty that rates will remain on hold.

FX Today:

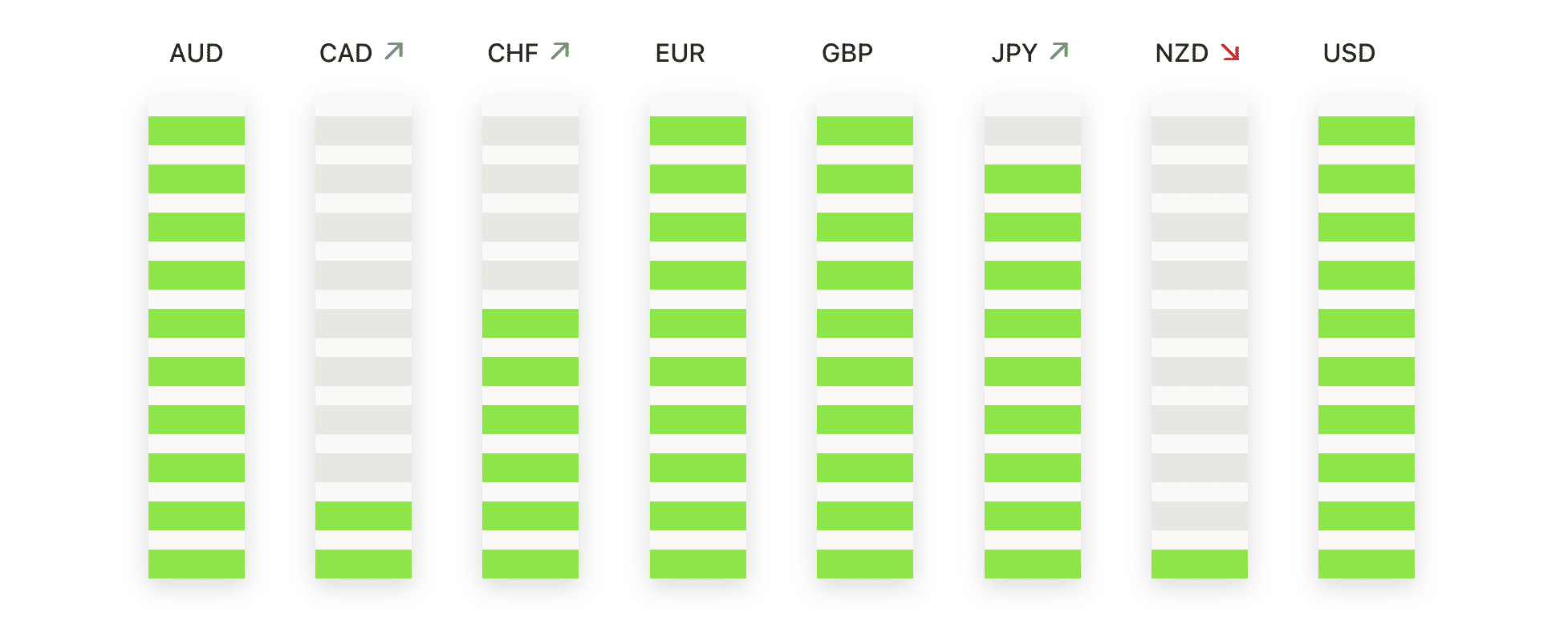

- EUR/USD Builds Momentum With Five-Day Winning Run: EUR/USD advanced to 1.1754, up 0.52% on the day, after briefly touching 1.1761. The pair has now rallied for five sessions in a row, pushing beyond short-term resistance and resuming the broader uptrend that’s been in place since February. Technical positioning remains strong, with price above the 50-day SMA at 1.1523 and climbing steadily since bouncing off 1.1600 mid-month. A break through the July high just below 1.1800 would likely trigger follow-through buying toward 1.1850 and 1.1900. Near-term support sits at 1.1700 and 1.1650, with deeper protection at 1.1600.

- GBP/USD Firms Near Recent Highs as Bulls Test 1.3400 Zone: GBP/USD closed at 1.3369, rising 0.41% after reaching a high of 1.3379 and a low of 1.3288. The pair extended its bounce from last week’s dip and is now trading just beneath the recent peak near 1.3400, a level that has capped multiple rallies since mid-June. The short-term structure remains bullish, with price above the 50-day SMA at 1.3234 and supported by a series of higher lows. A daily close above 1.3400 would signal a potential breakout and open the way toward 1.3455 and 1.3510. On the downside, minor support is seen at 1.3320 followed by 1.3280, and a drop below 1.3230 would weaken near-term momentum.

- USD/JPY Slips as Reversal Extends Into Key Support Area: USD/JPY settled at 146.59, falling 0.53% after reaching a high of 147.37 and dipping to 146.31. The pair has now fallen for three straight sessions, reinforcing signs of fading bullish momentum following last week’s rejection near 149. Price action has rotated below the 200-day SMA at 149.58 and is now hovering inside a support cluster defined by the 100-day average at 145.70 and the 50-day at 145.15. This area has previously triggered rebounds, so reaction here will be crucial. The broader trend remains mixed, though the pattern of lower highs is building. A clean break beneath 145.00 would open the way toward 144.30, while a move back above 147.50 is needed to re-establish upside traction.

- USD/CHF Drops Below Psychological Floor to Hit Fresh Lows: USD/CHF closed at 0.7918, down 0.73%, after trading between 0.7992 and 0.7918 intraday. The pair breached the 0.8000 level for the first time in months, confirming the dominance of the long-standing bearish trend. Price is now pressing against the lowest levels seen this year, with no support of significance until the March trough near 0.7850. Technical momentum remains firmly negative, with price action stuck below all major SMAs and each recovery attempt failing to reclaim even the 50-day average. Sellers remain in full control while the pair remains beneath the 0.8000–0.8050 resistance band. If 0.7900 fails to hold, the next leg lower could unfold quickly.

- AUD/USD Holds Range as Buyers Step In Near Support: AUD/USD rose to 0.6553, gaining 0.45% after bouncing from a low of 0.6504. The pair continues to consolidate in a broad range, with resistance near 0.6650 and support anchored around 0.6450. Tuesday’s rebound off the 100-day SMA suggests buying interest remains active on dips, while price continues to hover just above the 50-day average. The broader trend remains sideways, but short-term price action shows higher lows and some resilience at the lower end of the range. A close above 0.6575 would improve near-term momentum and increase the odds of a retest of the July highs. For now, the outlook remains neutral-to-bullish while price holds above 0.6500.

- Gold Breaks Out With Conviction as Bulls Eye Fresh Highs: Gold climbed to $3,431, gaining 1.00% after reaching a high of $3,433 and low of $3,383. The metal posted its strongest session in weeks, clearing resistance around $3,400 and extending above its recent consolidation range. Momentum is clearly back in favour of buyers, with price now trading well above the 50-day SMA at $3,327 and distant from the 100- and 200-day averages. The upward trend that began in February has reasserted itself, driven by a solid structure of higher lows and repeated rejections of downside. Immediate resistance now stands at $3,450, with secondary targets near $3,470. Should price retest $3,400 or $3,380 in coming sessions, those levels are expected to act as support zones within a broader bullish setup.

Market Movers:

- IQVIA Holdings Jumps on Strong Earnings Beat: IQVIA shares surged near 18% after the company reported second-quarter revenue of $4.02 billion, topping expectations of $3.96 billion and leading gains in the S&P 500.

- D.R. Horton Rallies After Raising Revenue Forecast: D.R. Horton rose over 16% after reporting stronger-than-expected Q3 net sales of 23,071 units and lifting its full-year revenue outlook to $33.7–$34.2 billion.

- Northrop Grumman Gains on Upgraded Profit Outlook: Shares of Northrop Grumman climbed more than 9% after the defence contractor raised its full-year EPS forecast to $25.00–$25.40, exceeding consensus.

- Lockheed Martin Sinks on Weak Sales and Lower Guidance: Lockheed Martin fell nearly 11% after reporting Q2 revenue of $18.16 billion, missing forecasts, and cutting its full-year EPS outlook to as low as $21.70.

- Philip Morris Slides on Revenue Miss and Soft Outlook: Shares of Philip Morris dropped more than 8% after the company’s Q2 revenue came in below estimates and its full-year organic sales growth guidance underwhelmed.

- General Motors Falls on Lower EBIT Guidance: GM shares declined more than 8% after the company forecasted full-year adjusted EBIT between $10.00 and $11.37 billion, with the midpoint below consensus.

- MSCI Declines on Weaker Recurring Revenue: MSCI lost over 8% after posting Q2 net new subscription sales of $43.8 million, coming in below the analyst forecast of $46.6 million.

Earnings continued to dominate market sentiment, with a sharp divide between sectors highlighting the shift away from technology and into healthcare and industrial names. While the S&P 500 held at record levels, weaker chip stocks weighed on the Nasdaq, and caution persisted ahead of results from major tech firms. In Europe, trade and fiscal pressures added to a subdued tone across the region, while Asia delivered a fragmented performance as inflation and political factors came back into focus. With bond yields easing and oil prices under pressure, markets now turn their attention to upcoming central bank decisions and whether corporate strength can maintain the current equity momentum.