European and Asian markets slid on Thursday as intensifying conflict between Israel and Iran and a series of central bank decisions unsettled investor sentiment. The Bank of England kept interest rates unchanged at 4.25%, while Norway and Switzerland surprised markets with rate cuts. Travel and leisure stocks led declines in Europe, while Hong Kong’s Hang Seng posted the sharpest losses in Asia. Oil prices surged as geopolitical tensions escalated further. With US markets closed for the Juneteenth holiday, global investors had no lead from Wall Street, adding to the day’s cautious tone.

Key Takeaways:

- Europe Drops Sharply on BoE Decision and Conflict Fears: European stocks fell across the board Thursday, with the Stoxx 600 closing down 0.8% and most major bourses in the red. The FTSE 100 slipped 0.58% to 8,791.80, while France’s CAC 40 dropped 1.29% and Germany’s DAX declined 1.12%. In Milan, the FTSE MIB fell 1.21%. Travel and leisure stocks were the biggest laggards, down 2.4%, while oil and gas shares gained 0.7% as crude prices rose. The Bank of England held its key interest rate at 4.25%, with three of nine members voting for a cut. Markets now anticipate a rate reduction in August.

- Asia-Pacific Indices Slide as Middle East Tensions Weigh: Asian markets ended mostly lower, led by a 2% drop in Hong Kong’s Hang Seng as investors weighed geopolitical risks and the Fed’s latest stance. Japan’s Nikkei lost 1.02% despite news of trimmed bond issuance for the fiscal year. Mainland China’s CSI 300 slipped 0.82%, while the Topix declined 0.58%. Australia’s ASX 200 closed flat at 8,523.7, with unemployment holding steady at 4.1%. South Korea’s Kospi was a rare gainer, up 0.19% as regional sentiment remained fragile. The worsening Israel-Iran conflict remained the dominant risk factor.

- Oil Jumps Nearly 3% on Escalating Conflict: Oil prices rallied as Israel bombed nuclear targets in Iran and Tehran responded with drone and missile attacks. West Texas Intermediate crude rose $2.06, or 2.7%, to settle at $77.20. Trading was thin due to the US holiday, but volatility was high amid fears of broader military escalation. Analysts warned that US involvement or disruption to the Strait of Hormuz could push prices sharply higher. JP Morgan sees oil surging to $120–$130 in an extreme scenario, while Goldman Sachs has lifted its risk premium estimate by $10.

- BoE Holds Rates at 4.25%, Eyes August Cut: The Bank of England left its benchmark rate unchanged at 4.25% on Thursday, as expected by most economists. However, three out of nine members voted for a 25-bps cut, signalling growing internal support for easing. The central bank cited weak UK GDP and loosening labour markets as reasons for staying cautious. Markets now widely expect a quarter-point reduction in August, with another cut seen likely in Q4. The decision came as inflation pressures ease, though rate-setters remain alert to geopolitical risks.

- Swiss National Bank Surprises with Cut to 0%: Switzerland’s central bank cut rates by 25 basis points to 0%, a widely expected move that nonetheless raised concerns about a return to negative rates. Consumer prices in Switzerland fell 0.1% year-on-year in May, fuelling deflationary fears. Traders had priced in an 81% chance of a 25-bps cut and a 19% chance of a larger 50-bps move. The franc’s persistent strength and ultra-low inflation remain key challenges for policymakers.

- Norway Cuts Rates Unexpectedly, Krone Slides: Norges Bank delivered a surprise rate cut to 4.25%, its first since 2020. The move defied expectations from 23 of 26 economists in a Reuters poll, who had forecast no change. Core inflation eased more than expected in May, but still exceeds the 2% target. The decision sent the Norwegian krone lower, with markets now pricing in at least one more cut before year-end.

- Turkey Holds Rates at 46% Amid Geopolitical Tensions: Turkey’s central bank kept its policy rate unchanged at 46%, opting for stability amid high inflation and regional conflict risks. The decision came despite cooling domestic price pressures, with the bank citing external threats to inflation expectations.

FX Today:

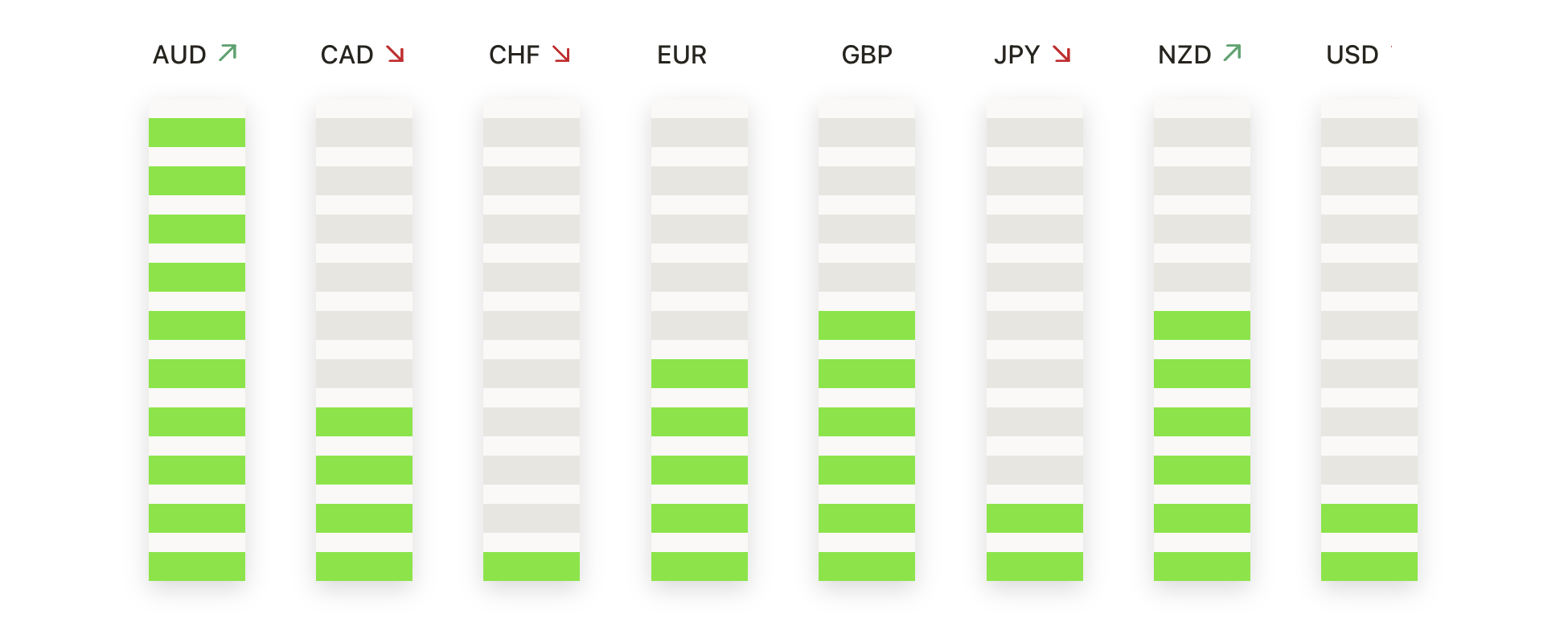

- EUR/USD Holds Above 1.1450 as Bulls Consolidate Gains: EUR/USD closed at 1.1498 on Thursday, rising 0.16% after a modest rebound from a session low of 1.1445. The pair printed a narrow-bodied bullish candle, with the session high touching 1.1499, just under the key psychological level of 1.1500. Buyers defended support near the midweek low, and price remains firmly above the 50-day SMA at 1.1356. The broader trend stays bullish with the 100-day and 200-day SMAs at 1.1013 and 1.0839 both trending upward. However, failure to retest 1.1600 this week may signal short-term exhaustion. A move below 1.1440 could expose 1.1350 and potentially 1.1300, while a daily close above 1.1600 is needed to push toward 1.1720.

- GBP/USD Rebounds Toward 1.3500 After BoE Hold: GBP/USD ended Thursday at 1.3469, up 0.36%, after recovering from an intraday dip to 1.3382. The pair posted a strong bullish candle, closing at the high of the day and reclaiming the 1.3400 handle. The 50-day SMA at 1.3389 provided clear support, cushioning the downside for the second time this week. GBP/USD continues to trade inside a rising channel, with all major moving averages pointing upward. Price remains well above the 100-day and 200-day SMAs at 1.3073 and 1.2928, reinforcing medium-term bullish momentum. A sustained break above 1.3550 would target 1.3700, while failure to hold 1.3380 could lead to tests of deeper support near 1.3300.

- AUD/USD Slides Below 0.6500 as Upside Momentum Fades: AUD/USD closed at 0.6478 on Thursday, declining 0.46% after failing to sustain a move above 0.6500. The pair traded in a range of 0.6446 to 0.6511 and formed a small-bodied bearish candle with an upper wick. Despite remaining above the 50-day SMA at 0.6435, price has failed multiple times to break above the 0.6550 zone. The broader trend since April remains upward, but recent daily closes suggest weakening momentum. A clear drop below 0.6435 would expose support near 0.6400 and 0.6350. To reassert bullish control, the pair must close above 0.6550 and target the 0.6620 area next.

- NZD/USD Pulls Back After Failing to Hold 0.6100: NZD/USD ended the session at 0.6046, falling 0.33%, after struggling to sustain strength above 0.6100 earlier this week. The daily candle formed a small bearish body, with the range confined between 0.6019 and 0.6054. Despite the drop, the pair remains inside a broader ascending structure from early May and trades above its 50-day SMA at 0.5990. The 100-day and 200-day SMAs at 0.5908 and 0.5866 continue to rise, reinforcing a supportive backdrop. Price action is compressing between support and resistance, with a break below 0.5990 opening the path to 0.5950. A daily close above 0.6100 would be needed to resume upside toward 0.6170.

- USD/CAD Rebounds Above 1.3700 in Thin Holiday Trade: USD/CAD rose 0.42% to finish at 1.3718 on Thursday, reversing a two-day slide after bouncing from an intraday low of 1.3651. The session produced a strong bullish candle as the pair reclaimed the 1.3700 handle, closing near the high of 1.3719. Price found support just below the 50-day SMA at 1.3671, which has held firm throughout June. Resistance remains at 1.3765, the monthly high. A break above that level could target 1.3840 next, while a move back below 1.3670 risks a retest of the 1.3600 zone.

- USD/JPY Extends Losses After Breaking Below 157.00: USD/JPY fell 0.48% on Thursday to close at 156.84, marking its sharpest one-day decline of the week. The pair traded between 156.32 and 157.66. Thursday’s close below the 157.00 level broke near-term trendline support, confirming growing downside momentum. Despite the retreat, the 50-day SMA at 155.78 still provides key support, with the 100-day and 200-day SMAs at 153.74 and 150.91 trending higher. If 155.70 breaks, price could slide toward 154.30 next. A recovery above 157.70 is needed to reestablish bullish control.

Market Movers:

- Nucor Surges on Strong Earnings Forecast: Shares of steelmaker Nucor rose more than 3% after the company issued upbeat second-quarter guidance of $2.55–$2.65 per share.

- Steel Dynamics Slips After Missing Estimates: Steel Dynamics dropped 2.29% after forecasting Q2 EPS between $2.00 and $2.04, falling short of the $2.73 analysts were expecting.

- Scholar Rock Jumps on Obesity Drug Update: Scholar Rock shares gained over 16% following trial data showing its experimental drug helps preserve muscle mass in patients using Eli Lilly’s weight-loss treatment.

- Bausch Health Rises on Insider Buying: Bausch Health surged 7.8% after chair John Paulson disclosed the purchase of 3.6 million shares. Combined with last week’s $14.7 million acquisition, Paulson now owns about 9% of the company’s stock.

- Regencell Plummets After Parabolic Surge: Regencell Bioscience tumbled 19% after gaining over 59,000% this year. The Hong Kong-based biotech recently underwent a 38-for-1 stock split and claims to treat ADHD and autism with herbal therapy.

- Circle Internet Group Soars on Senate Bill: Circle, the company behind stablecoin USDC, surged nearly 34% after the US Senate passed the GENIUS bill, creating federal guidelines for digital dollars pegged to the US currency.

With US markets shut for the Juneteenth holiday, global investors focused on central bank moves and rising geopolitical tensions. Rate decisions from the Bank of England, Norway, and Switzerland added monetary uncertainty, while the Israel-Iran conflict drove oil higher and kept risk sentiment subdued. European and Asian markets both posted broad losses, particularly in sectors sensitive to travel and energy. In FX, major pairs reflected cautious consolidation with resistance levels holding firm. As traders look ahead to Friday, attention will likely remain fixed on Middle East developments and signs of whether central banks are nearing a coordinated easing cycle.