US equities ended slightly higher on Monday as investors balanced renewed tariff threats from President Trump against optimism for upcoming corporate earnings. Despite the weekend announcement of fresh 30% tariffs on the EU and Mexico starting in August, markets largely shrugged off the risk, expecting room for negotiation. The S&P 500 posted a modest gain, while the Dow and Nasdaq also advanced, helped by strength in financials ahead of key bank earnings. Traders are also bracing for this week’s inflation data, which may shed light on the broader economic impact of ongoing trade tensions. Meanwhile, developments between the White House and the Federal Reserve added an extra layer of uncertainty, fuelling concerns over political interference in monetary policy.

Key Takeaways:

- S&P 500 Posts Modest Gain as Earnings Season Kicks Off: The S&P 500 rose 0.14% to 6,268.56 on Monday, helped by investor expectations that newly announced tariffs will be negotiated down ahead of the 1 August deadline.

- Dow Rises Slightly as Financials Provide Support: The Dow Jones Industrial Average advanced 88.14 points, or 0.20%, to end at 44,459.65. Financial stocks helped lift the index as investors positioned ahead of key bank earnings.

- Nasdaq Climbs Ahead of Tech Results and Crypto Momentum: The Nasdaq Composite gained 0.27% to 20,640.33 as traders awaited earnings from major tech firms and digested Bitcoin’s latest rally. The index recovered from early losses despite geopolitical noise, with sentiment supported by hopes of strong corporate results.

- Europe Mixed as FTSE Hits Record While Others Sink: Europe’s Stoxx 600 ended marginally lower by 0.06% at 546.99, clawing back intraday losses as investors assessed whether Trump’s tariff threats would be softened through negotiation. The UK’s FTSE 100 stood out, gaining 0.64% to a record 8,998.06, supported by a weaker pound and London’s separate tariff deal with Washington. Germany’s DAX fell 0.4% to 24,165.7, while France’s CAC 40 dropped 0.3% to 7,808. Italy’s FTSE MIB plunged 9% to 39,720 amid trade tensions and sector-specific pressures. In Sweden, June headline inflation rose 0.5% from May and 2.8% year-on-year, while core inflation stood at 3.3%.

- Asia Trades Mixed as Growth Signals Offset Tariff Worries: Asia-Pacific markets showed no clear direction on Monday as investors responded to Trump’s 30% tariff threats and mixed macro signals. Japan’s Nikkei 225 slipped 0.28% to 39,459.62, while the broader Topix was flat. Economic data was mixed, with machinery orders rising but core components slipping. China’s CSI 300 was flat at 4,017.67, while Hong Kong’s Hang Seng added 0.26% after Chinese exports rose 5.8% in June. South Korea’s Kospi climbed 0.83% on strong ICT trade surplus, but the Kosdaq edged down. India’s Nifty 50 declined 0.53% as inflation slid to 2.1%, a six-year low, while Singapore avoided recession with 1.4% quarterly growth.

- Oil Falls Over 1% as Russia Faces Sanction Deadline: Oil prices tumbled on Monday amid new threats from President Trump targeting buyers of Russian crude. Brent crude dropped $1.15, or 1.63%, to settle at $69.21 a barrel, while WTI slid $1.47, or 2.15%, to $66.98. Prices had rallied early in anticipation of tighter sanctions but reversed course as markets digested the 50-day deadline. Russia’s product exports fell 3.4% in June, and the EU is poised to introduce its 18th sanctions package, adding further downside pressure to energy markets.

- Treasury Yields Steady as Investors Await Inflation Data: The 10-year US Treasury yield was little changed at 4.429% on Monday, while the 30-year rose to 4.973% and the 2-year yield dipped slightly to 3.904%. Markets appeared to stabilise following Trump’s tariff announcement, focusing instead on upcoming inflation readings.

- Bitcoin Hits Record Above $120,000 as Crypto Week Begins: Bitcoin surged to a new all-time high on Monday, briefly topping $123,000 before pulling back to end lower. The rally was driven by anticipation of favourable US regulatory developments, including the GENIUS Act now under discussion in Congress. Institutional inflows into Bitcoin ETFs also supported sentiment, with Thursday’s $1.18 billion intake marking the strongest day of 2025.

FX Today:

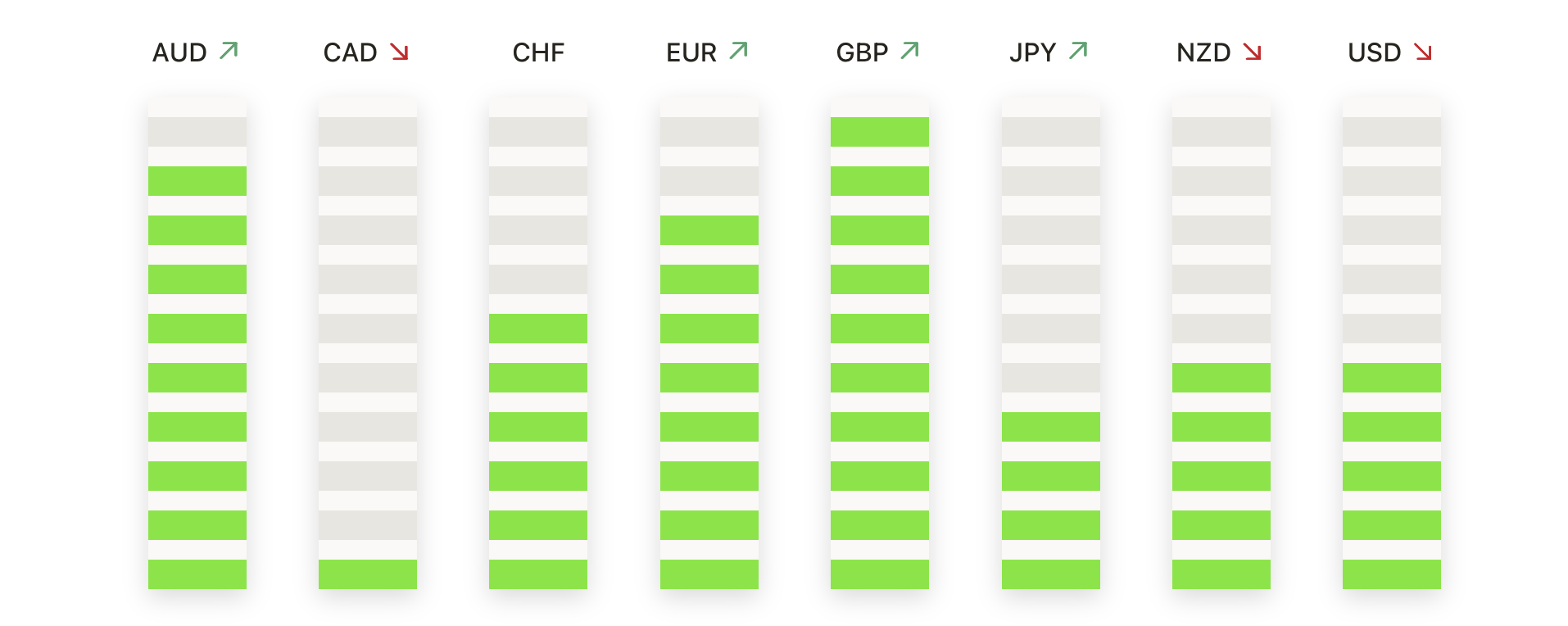

- EUR/USD Retreats as 1.1700 Barrier Halts Recovery Attempt: The pair closed at 1.1667 on Monday, slipping 0.18% after briefly reaching 1.1697 intraday. This marked the third consecutive daily loss and confirmed rejection at the key 1.1700 region. The failure to sustain above this level signals persistent selling pressure, with momentum turning lower as the recent bullish leg loses steam. While the broader trend remains supported above the rising 50-day SMA at 1.1473, bears may now target 1.1600 and 1.1530. For bulls to regain traction, a decisive push beyond 1.1730 is needed to reopen the path towards the July high near 1.1880.

- GBP/USD Sinks to Six-Week Low After Breaching Key Support: GBP/USD ended the session at 1.3427, falling 0.47% as it erased early gains and extended its losing streak to four days. The pair produced a strong bearish candlestick that closed below the 50-day SMA at 1.3499 for the first time since late May. After failing to stay above 1.3600 last week and rejecting the 1.3800 region in June, downside momentum is accelerating. Immediate support sits at 1.3400, with the 100-day SMA at 1.3259 offering deeper protection. A bounce above 1.3500 is needed to neutralise the current weakness and revive buying interest toward 1.3650.

- USD/JPY Presses Toward 148.00 as Bulls Eye Breakout: USD/JPY closed at 147.75, advancing 0.23%. The pair briefly touched 147.77, edging into a critical resistance zone just under 148.00 where the 100-day SMA currently sits. The structure remains bullish, supported by a rising 50-day SMA at 144.86 and a series of higher lows. A confirmed breakout above 148.00 would expose the longer-term 200-day SMA at 149.60 and open the door to a broader trend reversal. Failure here may lead to a short-term pullback toward 145.50.

- EUR/GBP Rally Extends to Three-Month High on Breakout Strength: EUR/GBP finished at 0.8689, rising 0.35% in its third consecutive daily gain. The pair reached an intraday high of 0.8693, marking its strongest level since mid-April as the bullish breakout from the June range gathers pace. Price now trades comfortably above the 50-day SMA at 0.8495, with both the 100- and 200-day averages climbing steadily. Resistance awaits at 0.8715–0.8750, followed by the March spike near 0.8810. Support rests at 0.8635 and the former breakout zone at 0.8600.

- Gold Remains Subdued Below $3,360 as Buyers Await Breakout: Gold settled at $3,345, slipping 0.28% after another session of tight-range trading. The price fluctuated between $3,374 and $3,341, forming a neutral candlestick with upper and lower shadows that highlighted market indecision. Repeated failures to break through the $3,380–$3,400 resistance zone have capped momentum since mid-May, with price coiling in a high-level consolidation. The 50-day SMA at $3,321 is flattening, while the broader trend remains underpinned by rising 100- and 200-day averages. Key support stays intact near $3,300–$3,310. A daily close above $3,400 is needed to spark renewed upside towards fresh highs.

Market Movers:

- Waters Tumbles on Becton Deal and Debt Load Concerns: The stock fell nearly 14% after announcing plans to merge with Becton Dickinson’s diagnostics unit. Waters will issue 39.2% of its stock and take on $4 billion in debt, while Becton shareholders will also receive a $4 billion payout. Becton edged slightly higher.

- SolarEdge Pops on Barclays Upgrade Despite Sector Challenges: The stock rose 4.3% after Barclays upgraded it to equal weight from underweight. The bank noted that SolarEdge is still poised to grow in 2024 and 2025, even as the overall solar market may contract in 2026.

- Coinbase and MARA Edge Higher as Bitcoin Hits New Record: Crypto-linked stocks rose after Bitcoin topped $123,000 before easing slightly. Coinbase climbed 1.8% while MARA Holdings added 0.4%, lifted by strong ETF inflows and anticipation around regulatory clarity from ‘Crypto Week’.

- Autodesk Rises as Takeover Plans for PTC Are Scrapped: Shares of Autodesk climbed 5% after Bloomberg reported the company will no longer pursue a potential acquisition of PTC.

- Fastenal Jumps After Beating Second-Quarter Profit Forecasts: The industrial supply firm rose 4% after posting Q2 earnings of 29 cents per share, ahead of analysts’ estimates of 28 cents.

- PayPal Gains as Analysts Downplay JPMorgan Data Fees: The stock advanced more than 3% following a Bloomberg report about new fees for bank data access.

- Nebius Group Surges on Goldman Buy Rating and AI Optimism: Shares jumped 17% after Goldman Sachs began coverage with a buy rating.

- nCino Rallies on Baird Upgrade Citing Strong Management Outlook: The fintech company gained over 3% after Baird upgraded the stock to outperform.

With trade tensions lingering and inflation data on deck, markets now enter a pivotal stretch where policy risks and corporate fundamentals will compete for investor attention. The start of earnings season will test the durability of recent gains, particularly as companies face pressure from tariffs, rates, and shifting global demand. Traders will also be watching the Federal Reserve’s response to political criticism, as questions around independence and rate policy resurface. Outside equities, moves in commodities and crypto are signalling diverging sentiment across asset classes. This week’s developments could prove decisive in determining whether markets can build on their summer momentum or face renewed volatility.