US stocks ended Friday mixed, with the S&P 500 and Nasdaq slipping after setting fresh records earlier in the session as investors locked in profits from a strong week. Weakness in chipmakers and a drop in consumer sentiment weighed on the broader market, though the Dow managed to close modestly higher. Retail sales data came in line with expectations, showing resilience among US consumers, while import prices edged higher. After the closing bell, focus shifted to Saturday’s high-stakes summit in Alaska between President Donald Trump and Russia’s Vladimir Putin. The talks ended without a breakthrough on Ukraine, though Trump described them as “productive” and Putin proposed another meeting in Moscow. The White House called the summit a listening exercise, but Ukraine’s exclusion from the discussions drew concern over sovereignty. Despite geopolitical uncertainty, Wall Street ended the week higher, with easing inflation data raising hopes of a Federal Reserve rate cut next month.

Key Takeaways:

- Dow Holds Firm With Weekly Outperformance: The Dow Jones Industrial Average inched higher by 34.86 points, or 0.08%, to 44,946.12 on Friday, lifted by a 12% surge in UnitedHealth and a 3.9% rise in Salesforce. Despite closing well below its intraday high, the index outperformed its peers, posting a weekly gain of 1.74%.

- S&P 500 Slips After Record Run: The S&P 500 fell 0.29% to finish at 6,449.80, snapping its upward momentum after hitting a record high earlier in the session. Semiconductor weakness, including a 14% slide in Applied Materials, pressured the index, though it still gained 0.94% for the week.

- Nasdaq Retreats on Chip Stock Selloff: The Nasdaq Composite dropped 0.40% to 21,622.98 on Friday, weighed down by losses in major chipmakers such as Nvidia and Applied Materials. The sector pullback overshadowed broader tech strength, with Alphabet and Meta edging higher. Despite the daily decline, the index still advanced 0.81% for the week.

- Europe Ends Flat Ahead of Trump–Putin Talks: European equities closed flat on Friday as investors awaited the outcome of the Alaska summit. The Stoxx Europe 600 slipped just 0.01%, dragged by a 0.6% fall in technology stocks. London’s FTSE 100 advanced 0.47% on the week to 9,138.90, its best performance in three weeks. France’s CAC 40 climbed 0.7% on Friday, marking its fourth straight gain and a 2.2% weekly advance, the strongest in nearly three months. Italy’s FTSE MIB jumped 1.1% on Thursday to 42,654, the highest in 18 years, supported by optimism over EU–US trade negotiations. Frankfurt’s DAX ended marginally lower at 24,374.9, though it held near one-month highs thanks to a strong earnings season. In Switzerland, GDP growth slowed sharply to 0.1% in Q2 from 0.8% in Q1, with weaker exports tied to new US tariffs.

- Asia Gains on Japan GDP and China Rally: Asia-Pacific markets ended the week broadly higher, led by Japan where the Nikkei 225 surged 1.7% on Friday to a record 43,378.31 as Q2 GDP growth of 0.3% beat forecasts and the yen’s weakness boosted exporters. The broader Topix also closed at a record 3,107.68. China’s CSI300 rose 0.7% and the Shanghai Composite gained 0.8% on Friday, logging their best weekly performance in nine months with a 2.4% weekly gain, even as economic data disappointed. Hong Kong’s Hang Seng fell 1% on the day but still advanced 1.7% over the week. In India, the Sensex edged up 0.07% to 80,597.66 and the Nifty 50 added 0.05% to 24,631.30, as investors stayed cautious before the Trump–Putin summit. South Korea’s markets were closed for a public holiday.

- US Data Mixed as Retail Sales Stay Solid: July retail sales rose 0.5% month-on-month, meeting forecasts, while core sales excluding autos gained 0.3%, highlighting continued consumer resilience despite tariff concerns. Import prices also rebounded 0.4% in July after a 0.1% dip in June, driven by higher consumer goods costs. However, consumer sentiment dropped sharply, with the University of Michigan index falling to 58.6 from 61.7, its first decline in four months.

- Oil Declines on Geopolitical Uncertainty: Oil prices slipped as traders positioned ahead of the Trump-Putin summit and weighed weak Chinese economic data. Brent crude fell 0.99%, while US WTI dropped 1.27%. Analysts projected a supply surplus averaging 890,000 barrels per day through mid-2026, reinforcing concerns of an oversupplied market after OPEC+ increases.

- Yields Rise After Retail and Sentiment Reports: US Treasury yields edged higher Friday following the latest consumer and spending data. The 2-year yield rose 2 basis points to 3.757%, while the 10-year climbed 3 basis points to 4.324%. The divergence between steady retail demand and weakening sentiment underscored uncertainty over the trajectory of the US consumer heading into autumn.

FX Today:

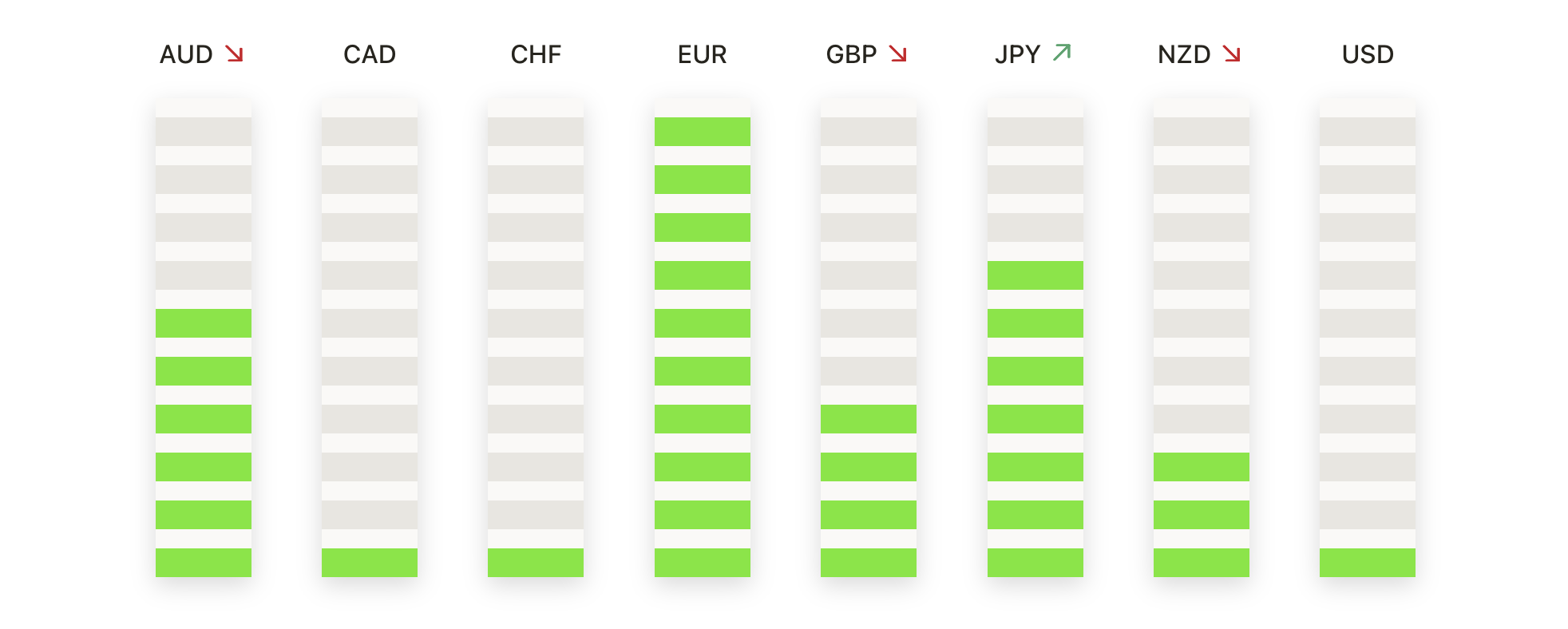

- EUR/USD Presses Higher Towards Key 1.1720 Resistance: EUR/USD closed at 1.1701, up 0.46% after trading between 1.1715 and 1.1646. The pair continued to build on Thursday’s advance, maintaining a firm position above the 50-day SMA at 1.1631 and the 100-day SMA at 1.1445. The rebound from early August lows near 1.1500 has reasserted the broader series of higher lows that has shaped price action since mid-April. Structurally, EUR/USD remains within a rising channel, with momentum narrowing the gap towards the July peak and resistance at 1.1720. A decisive close above this barrier would confirm renewed bullish control and open the way towards 1.1780 and 1.1850, while repeated failures could trigger consolidation back towards 1.1650.

- GBP/USD Consolidates Below Moving Average as Bulls Eye Breakout: GBP/USD ended at 1.3556, up 0.19% after trading between 1.3575 and 1.3526. The pair extended its recent consolidation just under the 50-day SMA at 1.3562, while holding comfortably above the 100-day SMA at 1.3391 and the 200-day at 1.3008. Momentum has remained steady since the early August rebound from 1.3260, which confirmed higher lows and pulled the pair back above key averages. Structurally, GBP/USD continues to grind higher within an upward channel established in late July, with resistance now focused on the 1.3600–1.3700 area. On the downside, initial support is seen at 1.3520, with stronger demand expected near the 100-day average if tested.

- USD/JPY Pulls Back as Sellers Keep Price Below 148.00: USD/JPY closed at 147.24, down 0.34% after trading between 147.87 and 146.73. The pullback left the pair capped under the 200-day SMA at 149.24, with resistance near 148.00 continuing to weigh on short-term sentiment. Price action has been range-bound after failing to hold the break above 150.00 in early August, with the 100-day SMA at 145.49 offering support beneath. Structurally, the pair remains in a sideways channel stretching back to mid-May, with recent momentum favouring consolidation rather than trend extension. A clear push above 148.20 would re-open a path to retest the 149.20–150.00 zone, while a close below 146.70 would expose 146.00 and 145.50.

- AUD/USD Holds Steady as Bulls Test 0.6520 Pivot Zone: AUD/USD finished at 0.6508, up 0.24% after trading between 0.6523 and 0.6487. The pair held steady just beneath the 50-day SMA at 0.6519 while keeping a firm base above the 100-day SMA at 0.6446 and the 200-day SMA at 0.6388. Structurally, price has been confined to a sideways channel since late May, with support repeatedly defended in the mid-0.6400s and rallies capped near 0.6520. The early August dip to 0.6420 was absorbed quickly, maintaining a constructive higher-low sequence from April. Resistance is now clustered at 0.6520–0.6530, where a daily close above could unlock a move towards the July high at 0.6600. On the downside, support lies at 0.6480, with firmer demand expected at the 100-day SMA.

- Gold Stays Range-Bound as $3,350 Resistance Caps Upside: Gold closed at $3,339, up 0.11% after trading between $3,349 and $3,332. The metal posted a modest gain but remained capped by the 50-day SMA at $3,348, which has contained price through recent sessions. Structurally, gold is consolidating within a sideways range following the early-August stall below resistance. The broader trend is supported by the 200-day SMA at $3,028 and a rebound from mid-July’s $3,280 low, but short-term momentum remains muted. A break above $3,350 would open the way to $3,380 and $3,400, while a close below $3,330 would expose $3,310 and $3,280.

Market Movers:

- UnitedHealth and Salesforce Lift Dow: UnitedHealth surged nearly 12% and Salesforce climbed 3.9%, helping the Dow outperform despite broader market weakness. The gains followed Berkshire Hathaway and Appaloosa filings showing increased positions in the healthcare group.

- Chip Stocks Slide on Weak Guidance: Applied Materials tumbled 14% after issuing disappointing guidance, dragging the VanEck Semiconductor ETF down 2%. Intel reversed the trend, rising 2.7% on reports of potential US government investment via Chips Act funding.

- Tech Leaders Mixed as Tesla Drops: The so-called Magnificent Seven ended unevenly with Tesla falling 1.5%, while Alphabet and Meta posted modest gains and Amazon closed little changed, highlighting selective strength within big tech.

- Crypto Stocks Retreat With Bitcoin: Bitcoin slipped 0.7% on Friday, pressuring crypto-linked shares as Riot Platforms sank 7.5% and Coinbase declined 2.2%, extending sector weakness.

- Sandisk Weakens After Outlook Cut: Sandisk dropped 4.6% as investors reacted negatively to management guidance, weighing further on the tech hardware segment.

Wall Street closed Friday on a mixed note, with chip sector weakness and falling consumer sentiment offsetting resilience in retail sales and strength in select Dow components. Attention quickly shifted to the weekend’s Trump–Putin summit, which ended without progress on Ukraine and left geopolitical risks firmly in focus. European and Asian markets showed stronger momentum, supported by upbeat earnings, trade optimism, and robust Japanese growth. With oil sliding and Treasury yields edging higher, the broader picture reflects a market still grinding higher, supported by expectations of a Federal Reserve rate cut next month despite lingering economic and geopolitical headwinds.