An escalating clash between President Trump and Elon Musk stole the spotlight on Thursday, sending Tesla shares plunging and shaking broader market sentiment. Investors also weighed the uncertain outlook for US-China trade after Trump’s call with President Xi yielded few clear breakthroughs. Across the Atlantic, European stocks rallied after the ECB delivered a widely anticipated rate cut. In commodities, silver surged to its highest level since 2012, fuelling fresh momentum in the precious metals space. With the focus now shifting to Friday’s US payrolls data, markets remained in a cautious but reactive mood.

Key Takeaways:

• Dow Slips as Tech Weakness Pressures Blue Chips: The Dow Jones Industrial Average declined 108 points, or 0.25%, closing at 42,319.74. Losses in major tech names, particularly Tesla, weighed on sentiment, Tesla loses $152 billion in market cap.

• S&P 500 Drops as Tesla Leads Market Lower: The S&P 500 fell 0.53% to end at 5,939.30, snapping recent gains. Tesla’s sharp selloff dragged on the index, while broader uncertainty over the Trump-Xi phone call and upcoming US economic data kept investors wary.

• Nasdaq Retreats Amid Tech Sector Turmoil: The Nasdaq Composite slid 0.83% to settle at 19,298.45. Tesla’s more than 14% plunge dominated headlines, while chipmakers and other tech names also reversed earlier gains. Volatility spiked as traders weighed trade policy risks and softening US data.

• Europe Rallies on ECB Cut and Bond Market Response:European markets ended higher after the ECB delivered a widely anticipated 25-basis-point rate cut, taking the deposit rate to 2%. Easing inflation expectations and lower energy costs supported the move. Government bond yields fell across the euro zone, with German 10-year yields down 4 basis points. Italy’s retail sales rose above expectations, while mixed construction data kept regional sentiment balanced. The DAX and CAC advanced, alongside gains in financials and rate-sensitive sectors.

• Europe Data Mixed Amid Construction Slump and Factory Resilience: Germany’s construction PMI fell to 44.4 in May, signalling deeper contraction, though business outlook improved for the first time since early 2022. Eurozone construction PMI slipped to 45.6, with Italy’s sector showing slight growth at 50.5, while France remained in contraction with a reading of 43.1. German factory orders surprised to the upside, rising 0.6% versus an expected 1% decline. In the UK, new car registrations climbed 1.6% year on year in May, adding a modest positive signal.

• Asia Mixed as South Korea Outperforms on Stimulus Hopes: Asia-Pacific markets delivered a mixed performance on Thursday. South Korea’s Kospi led regional gains, surging 1.49% to close at 2,812.05, hitting a fresh 10-month high. The Kosdaq added 0.8% to finish at 756.23. Analysts at Nomura expect the Kospi to reach 2,900 by year-end, fuelled by anticipated capital market reforms and fiscal stimulus under President Lee Jae-myung. Japan’s Nikkei 225 declined 0.51%, while the Topix lost 1.03% to 2,756.47. Australia’s ASX 200 ended flat at 8,538.9. Hong Kong’s Hang Seng rose 0.85%, and mainland China’s CSI 300 edged up 0.23% to close at 3,877.56. India’s Nifty 50 advanced 0.84%, and the BSE Sensex climbed 0.77%, ahead of the Reserve Bank of India’s expected rate cut on Friday.

• Oil Prices Rebound on Hopes of Trade Progress: Oil prices rose, with Brent crude up 0.74% to $65.34 a barrel and WTI gaining 0.83% to $63.37. The move followed news of a Trump-Xi phone call and plans for further trade talks. Analysts noted that easing trade tensions could boostdemand expectations, while Canadian wildfire risks also provided support despite concerns about future supply.

• Treasury Yields Climb Ahead of Payrolls Data: The 10-year Treasury yield rose over 3 basis points to 4.402%, while the 2-year yield jumped more than 5 basis points to 3.93%. Yields moved higher as investors braced for Friday’s nonfarm payrolls report. Softer jobless claims data and declining productivity added to uncertainty about the US economic outlook.

• US Labour Market Cools as Productivity Slumps: Initial jobless claims rose by 8,000 to 247,000 for the week ended May 31, exceeding expectations of 236,000 and marking the second consecutive weekly increase. Continuing claims slipped by 3,000 to 1.904 million. Separately, US productivity declined at a revised annualised rate of 1.5% in Q1, compared with an initial estimate of a 0.8% drop, marking the first decline since Q2 2022.

FX Today:

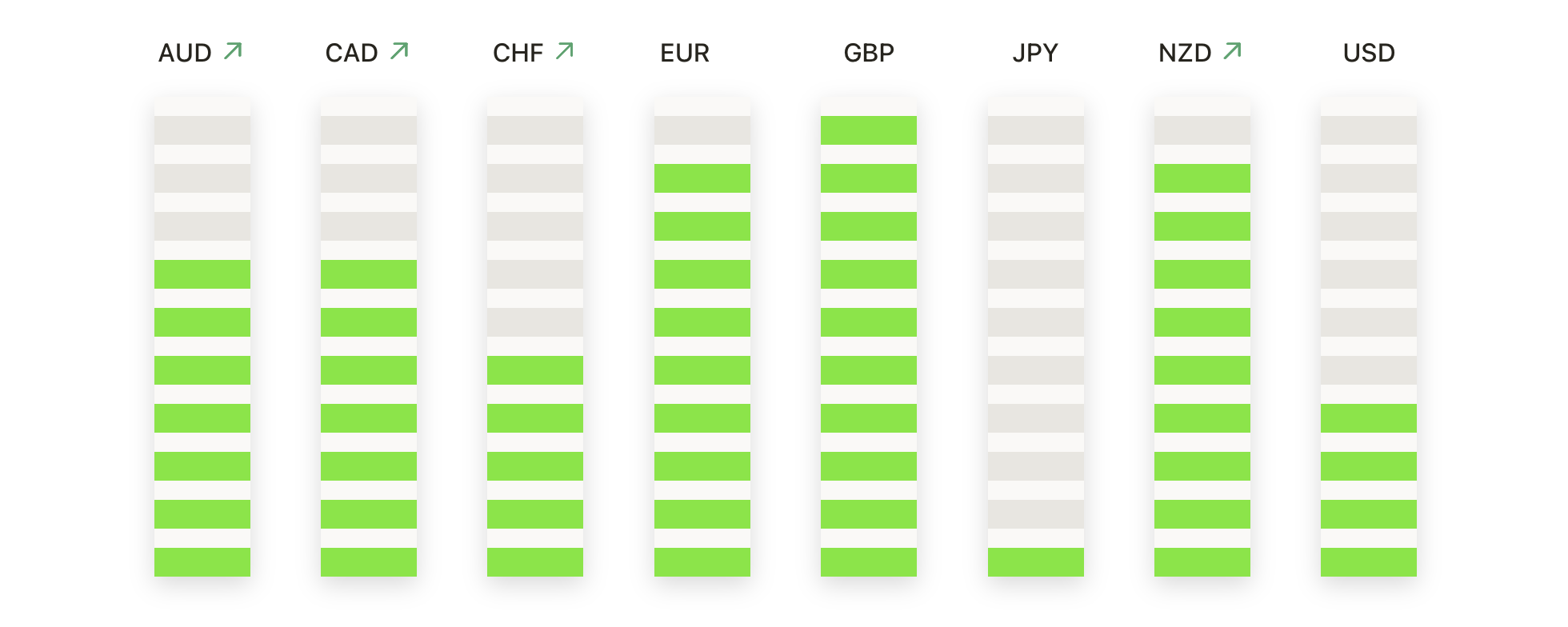

• EUR/USD Extends Uptrend Toward 1.1500 as Bulls Maintain Control: EUR/USD pushed higher on Thursday, closing at 1.1437, a gain of 0.18%, as bullish momentum remained intact. The pair continued to build on its breakout above 1.1200 from late May, with the 50-day SMA at 1.1242 providing dynamic support. Both the 100-day and 200-day SMAs are trending higher, confirming a solid medium-term structure. After consolidating above 1.1400 this week, EUR/USD is now eyeing the 1.1500 psychological barrier. A break above this level could expose resistance near 1.1550–1.1600. Dips toward 1.1350–1.1380 are likely to attract buyers.

• GBP/USD Bulls Target 1.3600 as Uptrend Accelerates:GBP/USD climbed modestly to close at 1.3573 on Thursday, up 0.14%, as the uptrend from early April remained firmly in place. Sterling continues to benefit from supportive UK economic data and hawkish Bank of England expectations. The 50-day SMA at 1.3266 is trending sharply higher, while the 100-day and 200-day SMAs also confirm the bullish bias. Immediate resistance is now in focus at 1.3600, with potential for an extension towards 1.3700 and 1.3750 on a break higher. On the downside, support rests near 1.3450 and the 50-day SMA. A sustained close above 1.3600 would likely fuel further gains heading into the second half of June.

• USD/JPY Slides Below 145 as Bearish Momentum Builds: USD/JPY dropped sharply on Thursday, settling at 143.66, down 0.63%, as the pair continued to retreat from recent highs. The move below the 50-day SMA at 144.62 signals a shift in near-term momentum. Additional resistance remains at 145.50 and 147.00, but the bias has turned negative. Support is now seen at 143.00, with stronger demand expected near 142.50. A break below this could open a path toward 140.00 in coming weeks. Unless bulls reclaim the 50-day SMA, the near-term outlook remains tilted lower.

• AUD/USD Breaks Above Key Resistance Toward 0.6550:AUD/USD extended its rally for a third straight session, closing at 0.6507, up 0.24%, as bullish momentum gathered pace. The pair cleared resistance near 0.6480 and is now challenging the upper boundary of its multi-month range. Importantly, it is trading well above the 200-day SMA at 0.6440, reinforcing the positive trend. The 50-day and 100-day SMAs are also turning higher. Immediate targets include 0.6550, with potential to test 0.6600–0.6630. Pullbacks toward 0.6450–0.6480 should find buyers.

• Gold Holds Support Near $3,350 as Bulls Defend Recent Gains: Gold settled at $3,358 on Thursday, down 0.46%, as the market remained in consolidation mode after its recent pullback. Buyers defended the $3,340 level, keeping prices above key short-term support. The 50-day SMA at $3,249 continues to act as a strong dynamic floor. Immediate resistance stands at $3,400, with a break above this level potentially targeting $3,450 and fresh all-time highs. On the downside, a breach of $3,340 could trigger moves toward $3,300 and the 50-day SMA.

• Silver Surges to 13-Year High as Bullish Momentum Builds: Silver surged on Thursday, closing at $35.67, up 3.55%, as bullish momentum accelerated to fresh multi-year highs. The metal broke decisively above the $35.00 level, clearing prior resistance and testing an intraday high of $36.06. The rally is supported by a rising 50-day SMA at $32.81, with the 100-day and 200-day SMAs also trending higher. Strong investor demand, favourable industrial trends, and supportive macro conditions are driving the uptrend. Immediate resistance lies at $36.50, with $37.00 coming into view if momentum persists. A close above $36.50 would bring the metal within striking distance of its all-time high, further reinforcing the bullish trend.

Market Movers:

• Tesla Plunges After Trump Threatens Musk’s Government Contracts: Tesla shares dropped more than 14%, losing their trillion-dollar market cap, after President Trump criticised Elon Musk and proposed ending government contracts and subsidies for Musk’s companies.

• Brown-Forman Tumbles on Weaker-Than-Expected Sales: Brown-Forman dropped more than 17% after posting Q4 net sales of $894 million, falling short of analysts’ expectations for $968.4 million.

• PVH Corp Cuts Forecast, Shares Slide Sharply: PVH Corp fell over 17% after lowering its 2026 adjusted EPS guidance well below prior forecasts and market consensus.

• Costco Wholesale Falls as Sales Miss Market Forecast:Costco shares lost more than 3% after May comparable sales rose 4.3%, below the expected 4.7% growth.

• MongoDB Surges After Strong Earnings and Upbeat Outlook: MongoDB jumped more than 12% after posting Q1 adjusted EPS of $1.06, topping estimates, and raising its full-year guidance.

• Ciena Corp Drops After Earnings Miss Expectations:Ciena Corp shares declined more than 12% after reporting Q2 adjusted EPS of 42 cents, missing analyst estimates of 52 cents.

Investors faced a mix of caution and opportunity on Thursday, with Tesla’s sharp decline and uncertainty over US-China trade talks tempering broader market enthusiasm. While European equities found support from the ECB’s rate cut and improving bond markets, sentiment elsewhere remained mixed ahead of key US data. Asia’s varied performance reflected both local drivers and global trade risks. All eyes now turn to Friday’s nonfarm payrolls report, which could shape near-term expectations for the US economy and monetary policy. Developments in US-China trade discussions will also remain a key focal point for markets heading into next week.