US equities extended their winning streak on Wednesday as a renewed rebound in technology helped lift sentiment ahead of the Thanksgiving break. A strong performance from major AI and software names underpinned the advance, with investors largely embracing the week’s improving momentum and renewed confidence in the year-end outlook. Comments from market strategists highlighted a broader shift back into risk assets following last week’s volatility, while expectations for a December interest rate cut continued to firm. With traders preparing for Thursday’s holiday closure and a shortened session on Friday, attention turned to whether the recent rally can carry the major averages into the final weeks of November despite lingering concerns over valuations and the month’s uneven performance.

Key Takeaways:

- Dow Extends Winning Streak Ahead of Thanksgiving: The Dow Jones Industrial Average gained 314.67 points, or 0.67%, to finish at 47,427.12, marking its fourth consecutive session of gains. The index is now up more than 2% for the week, on pace for its strongest weekly performance since late June.

- S&P 500 Posts Firm Rise as AI Leaders Support Gains: The S&P 500 climbed 0.69% to close at 6,812.61, led by renewed interest in growth, semiconductors and megacap technology. The index is now more than 3% higher for the week, trimming earlier November losses after valuation pressures cooled earlier momentum.

- Nasdaq Rebounds With Tech Up 0.82%: The Nasdaq Composite rose 0.82% to 23,214.69, lifted by gains of more than 1% in Nvidia, nearly 2% in Microsoft and around 4% in Oracle. Alphabet reached new record highs after reports that Meta could adopt its TPU chips from 2027. The tech-heavy index has climbed more than 4% so far this week, its strongest weekly pace since late June, though it remains more than 2% lower for November as valuation concerns persist.

- Europe Stocks Rally as Fed Cut Bets Strengthen and UK Budget Supports Sentiment: European equities pushed higher across all major indices as growing confidence in a December Federal Reserve rate cut lifted risk appetite. The Stoxx 600 rose almost 1.1% in a broad-based advance, while the FTSE 100 gained 82.05 points to 9,691.58 and the CAC 40 added 71 points. Italy’s FTSE MIB climbed 432 points and Germany’s DAX increased 262 points as technology and banking names led the regional rally. UK assets also strengthened after Chancellor Rachel Reeves unveiled a budget that increased fiscal headroom to nearly £22 billion over five years, easing long-term fiscal concerns and sparking the largest single-day drop in 30-year gilt yields since mid-April, down 11 basis points to 5.215%. Strong gains from ASML, Infineon, Santander, BBVA, Intesa Sanpaolo and ING helped drive the move.

- Asia-Pacific Markets Track Wall Street Momentum as Fed Expectations Firm: Asian markets rallied broadly as speculation grew that Kevin Hassett is the frontrunner for the next Fed chair, reinforcing hopes for a more dovish policy path. Japan’s Nikkei 225 surged 1.85% to 49,559.07, with utilities, real estate and financials outperforming, while the Topix added nearly 2% to 3,355.5. Semiconductor-linked names saw sustained interest, with Toppan up 6.27%, SoftBank 5.65%, Advantest 2%, Tokyo Electron 0.23%, and Renesas 3.15%; however, Kioxia plunged 14.89% as Bain Capital prepared a ¥350 billion share sale. South Korea’s Kospi rose 2.67% 7 and the Kosdaq climbed 2.49%, despite Lotte Corp sliding 6.09% after announcing plans involving Lotte Chemical and HD Hyundai Chemical. Australia’s ASX 200 gained 0.81% to 8,606.5 even as CPI accelerated to 3.8% year on year. Hong Kong’s Hang Seng added 0.38%, China’s CSI 300 gained 0.61% to 4,517.63, Taiwan’s Taiex rose 1.85% backed by Foxconn’s 3.65% advance, and India’s Nifty 50 and Sensex both climbed over 1% despite a 2.2% drop in Bharti Airtel.

- Oil Prices Climb Ahead of Thanksgiving: Brent crude settled 65 cents higher, or 1.04%, at $63.13 a barrel, while WTI rose 70 cents, or 1.21%, to $58.65. US crude inventories increased by 2.8 million barrels to 426.9 million, far above forecasts for a 55,000-barrel rise, with net imports jumping 1.05 million bpd to 2.84 million bpd.

- Treasury Yields Hold Steady Near 4%: The 10-year yield eased less than 1 bp to 3.994%, the 30-year fell just over 1 bp to 4.641%, while the 2-year rose more than 1 bp to 3.477%. Markets are pricing in an 80%+ probability of a 25-bp Fed cut in December.

- US Jobless Claims Fall to 216,000: Initial jobless claims dropped by 6,000 to 216,000 for the week ended 22 November, below expectations for 225,000 and marking the lowest level since 12 April. Continuing claims rose by 7,000 to 1.960 million, covering the survey period for November’s employment report.

FX Today:

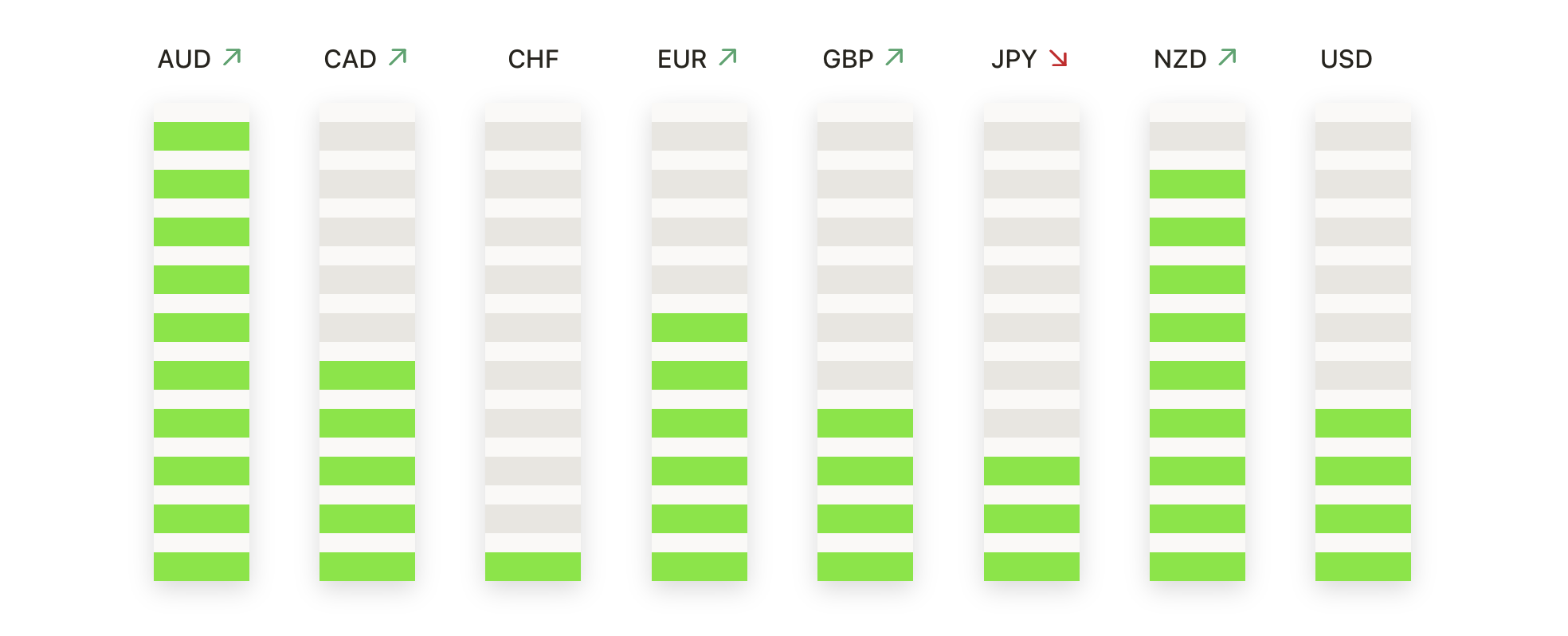

- EUR/USD Stabilises as Buyers Work to Reclaim Lost Ground: EUR/USD closed at 1.1593, up 0.20%, after moving between 1.1601 and 1.1547, with the pair showing early signs of regaining momentum following recent weakness. Despite the improvement, it continues to trade below the 50-day and 100-day SMAs at 1.1628 and 1.1646, keeping upside progress contained. Support at 1.1547 remains the immediate line of defence, while the 1.1628–1.1646 region forms the next hurdle to clear. A decisive break above those averages would strengthen recovery prospects toward 1.1700.

- GBP/USD Rebounds as Sterling Edges Back Toward Key Barriers: GBP/USD finished at 1.3236, rising 0.53% after a session range of 1.3242 to 1.3124, as renewed bid interest helped lift the pair toward the 200-day SMA at 1.3307. The broader trend still faces resistance from the 50-day and 100-day SMAs at 1.3293 and 1.3380, though the latest move signals improving near-term sentiment. A break above 1.3307 would open scope for further gains, while a drop back under 1.3124 would expose the prior swing levels.

- AUD/USD Firms With Momentum Building Near Moving Averages: AUD/USD closed at 0.6518, up 0.76%, after trading between 0.6521 and 0.6464, showing solid interest as the pair moved closer to the 50-day and 100-day SMAs at 0.6533. The 200-day SMA at 0.6461 continues to offer deeper support, helping maintain the broader consolidation phase. Resistance rests at 0.6521 and 0.6533, with a break above this zone needed to shift the bias more clearly upward.

- USD/CAD Eases From Highs but Retains Its Broader Upward Tone: USD/CAD settled at 1.4041, down 0.41%, following a range of 1.4105 to 1.4035, slipping modestly after testing overhead resistance. Despite the pullback, the pair continues to hold above its 50-, 100- and 200-day SMAs at 1.3993, 1.3882 and 1.3923, maintaining the broader constructive trend. Resistance remains at 1.4105 and 1.4150, while support at 1.4035 and 1.3993 forms the first downside zone to watch.

- USD/JPY Pushes Higher as Uptrend Drives Fresh Cycle Highs: USD/JPY ended at 158.44, up 0.26%, after moving between 158.74 and 155.65, extending its strong run as momentum carried the pair to new multi-year highs. Prices remain significantly above the 50-, 100- and 200-day SMAs at 152.20, 149.92 and 147.89, keeping the bullish structure firmly intact. Resistance at 158.74 and the 159.00 level remains the key barrier, while 155.65 provides support.

- Gold Climbs to New Records With Uptrend Firmly Intact: Gold closed at $4,165, up 0.83%, after trading between a high of $4,173 and a low of $4,130, extending its powerful run to fresh record territory. Price remains significantly above the 50-day, 100-day and 200-day SMAs at $4,009, $3,714 and $3,448, underscoring the strength and maturity of the prevailing bullish trend. The latest candle confirms firm upside momentum, with $4,173 marking the immediate resistance zone in uncharted territory. On the downside, $4,130 and the psychological $4,100 level form the first support band, ahead of the 50-day SMA at $4,009, which is the next major level to watch on any corrective pullback.

Market Movers:

- Urban Outfitters Surges on Strong Quarterly Sales: Urban Outfitters jumped more than 12% after reporting Q3 net sales of $1.53 billion, beating expectations of $1.49 billion.

- Semiconductor Strength Lifts Broader Tech Sector: Chip makers outperformed, with Marvell Technology up more than 5% and ASML rising over 4%. AMD, Applied Materials, Broadcom and ON Semiconductor gained more than 3%, while Micron, Analog Devices, Intel, Microchip Technology, Lam Research and Texas Instruments advanced over 2%.

- Robinhood Rallies After Expanding Into Derivatives: Robinhood rallied more than 10% after announcing it had acquired a majority stake in LedgerX, giving the company access to a regulated US derivatives exchange and opening a pathway into prediction markets.

- Oscar Health Climbs on Analyst Upgrade: Oscar Health rose more than 8% after Piper Sandler upgraded the stock to overweight from neutral, setting a new price target of $25.

- Dell Moves Higher on Upgraded Revenue Outlook: Dell gained more than 5% after raising its 2026 revenue forecast to $112.2 billion from a prior range of $105 billion–$109 billion, well above consensus expectations of $107.94 billion.

Markets head into the holiday period on firmer footing, with the latest rebound helping to stabilise what had been a challenging month for equities. The combination of stronger tech leadership, improving global risk sentiment and firm expectations for a December rate cut has given investors renewed conviction after several weeks of uneven trading. While questions around valuations and the broader economic backdrop remain, this week’s performance has gone some way toward rebalancing sentiment. Attention now turns to whether the current momentum can survive the lighter volumes of the shortened week and carry through into the start of December, where incoming data and central bank signals will set the next direction of travel.