Wall Street closed modestly higher on Thursday, lifted by a strong earnings report from Nvidia, though gains were tempered by renewed volatility surrounding US trade policy. A federal trade court initially struck down President Trump’s “reciprocal” tariffs, but a subsequent appeals court ruling quickly reinstated them, injecting fresh uncertainty into the market. Investors also digested economic data showing rising jobless claims and weaker-than-expected GDP revisions, raising concerns about the labour market and broader economic trajectory. Despite the volatility, the S&P 500, Nasdaq, and Dow all advanced, supported by optimism around artificial intelligence and selective earnings strength. As the week nears its end, major indexes remain on track for strong weekly and monthly gains.

Key Takeaways:

- Dow Rises Modestly in Choppy Session: The Dow Jones Industrial Average added 117.03 points, or 0.28%, to close at 42,215.73 after swinging between gains and losses throughout the day. Uncertainty surrounding US trade policy and mixed economic data kept gains in check, though sentiment was supported by select corporate strength, including Boeing’s rally.

- S&P 500 and Nasdaq Advance but Miss Highs: The S&P 500 rose 0.4% to 5,912.17 and the Nasdaq Composite gained 0.39% to 19,175.87. Both indexes were well off their intraday highs of 0.9% and 1.5%, respectively, as investor caution emerged following legal volatility over tariff rulings and softening economic data.

- Europe Ends Mixed as Trade Ruling Sparks Unease: European markets finished unevenly on Thursday, reversing earlier optimism after a US trade court invalidated Trump’s reciprocal tariffs. The Stoxx 600 slipped 0.19%, dragged by losses in German and UK stocks. Germany’s DAX dropped 0.44% to 23,933.23, while the UK’s FTSE 100 edged down 0.11% to 8,716.45. France’s CAC 40 bucked the trend, rising 0.9% to 7,862, and Italy’s FTSE MIB added 0.4% to near 40,280. Britain’s auto sector weighed on sentiment as April vehicle output plunged 15.8%, the worst April since 1952 excluding pandemic-related shutdowns. The drop was blamed on weak global demand, US tariffs, and the timing of the Easter holiday, adding to growing concerns about the region’s industrial resilience.

- Asia Rebounds as Courts Challenge US Tariffs: Asian equities broadly advanced on Thursday after the US Court of International Trade ruled against President Trump’s sweeping tariff orders, boosting regional risk appetite. Japan’s Nikkei 225 climbed 1.88% to 38,432.98, while the Topix rose 1.53% to 2,812.02. South Korea’s Kospi jumped 1.89% to 2,720.64 and the Kosdaq gained 1.03%. Hong Kong’s Hang Seng added 1.35% to 23,573.38, and China’s CSI 300 rose 0.59% to 3,858.70. Australia’s ASX 200 inched up 0.15% to 8,409.8. India’s Sensex and Nifty were flat. The Bank of Korea cut its policy rate to 2.5%, its lowest since 2022, as policymakers sought to support growth amid trade friction and slowing inflation. Traders also focused on Asian semiconductor stocks after Nvidia’s blockbuster results raised optimism for global chip demand.

- Oil Drops Amid Demand Worries and Legal Jitters: Oil prices fell as demand concerns in China resurfaced and traders reacted to the back-and-forth US tariff news. Brent declined 1.19% to $64.13, while WTI dropped 1.52% to $60.90. Comments from the IEA citing weak consumption and geopolitical uncertainty added to bearish sentiment.

- Treasury Yields Slide on Jobs and Court News: The 10-year Treasury yield dropped 5 bps to 4.438% as markets absorbed the tariff ruling and soft economic signals. The 30-year yield fell to 4.922%, while the 2-year eased to 3.945%. Investors sought safety as rising jobless claims and policy uncertainty clouded the outlook.

- Jobless Claims Rise Sharply, GDP Revised Down: Initial jobless claims rose to 240,000, exceeding expectations and marking the highest level since late 2021. Continuing claims climbed to 1.83 million. First-quarter GDP was revised down to -0.2%, driven by a surge in imports, though private investment partially offset slowing consumer spending.

FX Today:

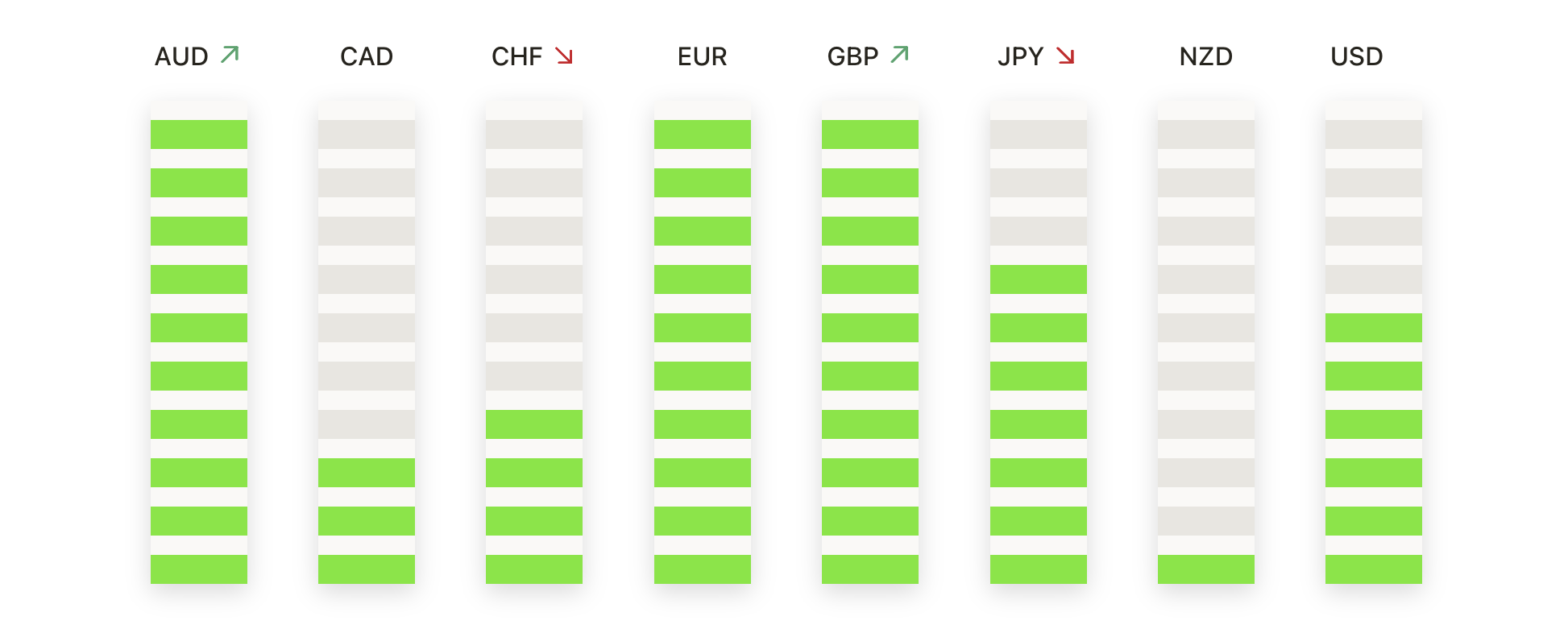

- EUR/USD Rebounds Sharply on Weaker US Data: The euro strengthened against the dollar on Thursday, with EUR/USD climbing 0.67% to settle at 1.1366. The pair rallied from an open of 1.1291, driven by soft US jobless claims and GDP data that weighed on the greenback. EUR/USD cleared resistance at 1.1340 and touched an intraday high of 1.1384 before easing slightly into the close. The move marked its strongest finish in over a week and brought the pair closer to the key 1.1400 level. The 50-day SMA at 1.1184 continues to provide firm support, while the 100-day and 200-day SMAs at 1.0849 and 1.0812, respectively, reinforce the pair’s bullish alignment. As long as price holds above 1.1300, the broader uptrend remains intact.

- GBP/USD Holds Near 1.3500 as Bulls Remain in Control: GBP/USD edged up 0.17% to close at 1.3493, extending its consolidation near recent highs. The session saw a dip to 1.3415 before recovering, with price holding above key support at the 50-day SMA at 1.3206. Medium-term momentum remains bullish, supported by rising 100-day and 200-day SMAs at 1.2899 and 1.2890. The pair continues to respect its breakout above 1.3300 earlier in May, and Thursday’s higher low reaffirms buyers’ dominance above the 1.3400 zone. A decisive close above 1.3600 would open the door to further gains toward 1.3700, while support rests at 1.3410 and 1.3330 if the rally stalls.

- USD/JPY Drops to 144.14 After Rejection at 146: USD/JPY declined 0.47% to settle at 144.14, reversing early gains after failing to hold above the 146 handle. The pair initially rose to 146.28 but was capped by the 50-day SMA at 145.31, triggering a sharp reversal. With price now well below the 100-day and 200-day SMAs at 148.71 and 149.44, the medium-term trend remains tilted to the downside. Thursday’s close reinforces the pair’s trading range between 143.50 and 145.50, and a break below the lower bound could bring the May low near 140.30 into focus. Bulls must reclaim 146.00 to regain traction, but momentum continues to favour sellers below the major averages.

- USD/CHF Pressured Below 0.8300 as Downtrend Deepens: The dollar weakened against the Swiss franc, with USD/CHF falling 0.36% to close at 0.8230. The pair failed to sustain gains above 0.8347 and reversed into a daily bearish candle, marking the third failed rally since early May. The price remains below key moving averages, with the 50-day SMA at 0.8388 and both the 100-day and 200-day SMAs near 0.8690. Persistent downside pressure and shallow rebounds suggest bears remain in control. With 0.8200 being retested, a break below could target the April low at 0.8080. Resistance remains firm near 0.8350, and unless reclaimed, rallies are likely to be faded.

- Gold Advances to $3,316 as Momentum Builds: Gold extended its recovery with a gain of 0.87%, settling at $3,316 on Thursday. The metal rallied from an open of $3,288 and hit $3,331 before easing slightly. This marks the second consecutive advance and reinforces support at $3,245, which held earlier in the week. The 50-day SMA at $3,217 continues to guide the uptrend, with the 100-day and 200-day SMAs at $3,028 and $2,824 confirming bullish structure. Resistance at $3,330 remains the key short-term barrier. A breakout could aim for April’s peak near $3,400, while any pullback toward $3,275 or $3,217 would likely attract fresh demand.

Market Movers:

- Nvidia Surges on Blowout Earnings: Nvidia (NVDA) jumped over 3% after posting Q1 revenue of $44.06 billion, beating estimates of $43.29 billion. Its data centre division grew 73% year-over-year, fuelling renewed AI enthusiasm.

- Elf Beauty Soars on Rhode Deal: Elf Beauty (ELF) surged more than 22% after Q4 sales hit $332.6 million, above the $327.4 million forecast. Investors cheered its $800 million acquisition of Hailey Bieber’s Rhode brand.

- Veeva Systems Pops on Upbeat Outlook: Veeva Systems (VEEV) rallied more than 18% after Q1 revenue topped expectations at $759.0 million. The company raised its full-year forecast to $3.09–$3.10 billion.

- Boeing Rallies on Production Boost: Boeing (BA) gained more than 3% after announcing plans to increase 737 jet production to 47 units per month by year-end. The update reassured investors amid recent delivery delays. Boeing led gainers within the Dow.

- HP Inc. Sinks on Weak Guidance: HP (HPQ) plunged over 8% after Q2 EPS of $0.71 missed expectations of $0.80. It also cut full-year EPS guidance to $3.00–$3.30, well below the prior $3.45–$4.75 range. Demand softness weighed on sentiment.

- SentinelOne Falls on Revenue Downgrade: SentinelOne (S) dropped more than 11% after cutting its 2026 revenue forecast to $996 million–$1.00 billion. That missed previous projections of $1.01 billion. The cybersecurity firm cited slower deal flow.

- Best Buy Slips on Outlook Cut: Best Buy (BBY) fell over 9% after lowering its 2026 EPS forecast to $6.15–$6.30 from $6.20–$6.60. The retailer flagged cautious consumer trends. The update disappointed investors looking for stability.

- Uber Drops After Tesla Enters Ride-Share: Uber (UBER) declined over 4% after Elon Musk said Tesla was testing self-driving taxis in Austin. Uber already partners with Waymo in the same city. The news sparked fresh concerns over disruption.

Thursday’s session reflected a market torn between optimism over strong corporate results and the lingering unease stirred by shifting trade policies and weakening economic signals. Nvidia’s earnings helped keep major indexes in positive territory, but volatility surrounding Trump’s reinstated tariffs and a surprise spike in jobless claims dampened risk appetite. Treasury yields fell as investors turned cautious, while oil dropped on global demand concerns. As May draws to a close, markets remain on track for solid monthly gains, yet fragile sentiment suggests any escalation in policy uncertainty or economic softness could quickly test the rally’s resilience.