The S&P 500 notched another record close on Thursday, lifted by investor confidence in Nvidia’s earnings as traders embraced the company’s reaffirmation of the artificial intelligence boom. The broad market index rose above the 6,500 mark for the first time, while the Nasdaq also advanced and the Dow edged higher. Nvidia’s second-quarter figures underscored robust growth despite a cautious revenue outlook, with several Wall Street banks lifting price targets on the stock. Gains spread across the semiconductor sector and select technology names, helping offset lingering political tensions surrounding the Federal Reserve and trade. Attention now shifts to Friday’s inflation report, with markets looking for fresh guidance on policy direction.

Key Takeaways:

- Dow Jones Edges Higher: The Dow Jones Industrial Average gained 71.67 points, or 0.16%, to finish at 45,636.90. The index saw muted moves compared with its peers as strength in technology was partially offset by weakness in consumer and industrial names.

- S&P 500 Reaches Fresh Record: The S&P 500 advanced 0.32% to close at 6,501.86 after briefly topping 6,500 intraday for the first time. Nvidia’s results, which confirmed surging demand for artificial intelligence technology, proved the key driver.

- Nasdaq Climbs on Tech Momentum: The Nasdaq Composite rose 0.53% to 21,705.16, extending gains as chipmakers and AI-linked names rallied. Snowflake surged more than 20% after strong results, while Micron and Broadcom added over 3%.

- European Markets Struggle Despite Strong Data: European equities finished mixed to lower, with the Stoxx 600 down 0.2% despite early strength. The FTSE 100 slipped 0.42% to 9,216.82, weighed by an 8% drop in Drax after a UK probe into its biomass disclosures. France’s CAC 40 gained 0.24% to 7,762.61, supported by Pernod Ricard, while Italy’s FTSE MIB rose 0.2% to 42,447. Germany’s DAX was flat at 24,044. Auto sector optimism helped sentiment after EU car registrations jumped 7.4% in July, led by a nearly 40% surge in battery-electric vehicles. Lending data also signalled improving credit conditions, with household loans up 2.4% and corporate lending up 2.8%, both at multi-year highs. UK car production rose 5.6% in July, while the government’s new £2.5 billion DRIVE35 industrial plan was a support for manufacturing.

- Asia-Pacific Markets Trade Mixed: Asia-Pacific equities closed with no clear direction as investors absorbed the Bank of Korea’s decision to hold rates steady at 2.5%. Japan’s Nikkei 225 rose 0.73% to 42,828.79 and the Topix gained 0.65% to 3,089.78, helped by strength in exporters. South Korea’s Kospi added 0.29% while the Kosdaq lost 0.41%. Australia’s S&P/ASX 200 advanced 0.22% to 8,980, with Qantas rallying on stronger-than-expected earnings, though Lynas Rare Earths was halted after announcing a discounted capital raise. Hong Kong’s Hang Seng slid 0.79% but the mainland CSI 300 rose 1.77% to 4,463.78. India’s Nifty 50 dropped 0.49% as fresh 25% US tariffs on Indian exports came into effect, lifting overall duties to 50% and pressuring key sectors such as gems, jewellery and electrical machinery.

- US Economy and Labour Market Resilient: US gross domestic product expanded at a 3.3% annualised pace in the second quarter, stronger than the initial 3.0% estimate and beating forecasts of 3.1%. Consumer spending rose 1.6% compared to a prior 1.4% estimate, while imports fell nearly 30% as firms adjusted to tariff policy. Weekly jobless claims also underscored labour market resilience, falling by 5,000 to 229,000 against expectations of 230,000. Continuing claims eased to 1.95 million after hitting a near four-year high the week before.

- Oil Prices Recover After Early Weakness: Brent crude futures settled 0.84% higher at $68.62 per barrel, while WTI gained 0.7% to $64.60. Prices bounced after initial losses as traders digested reports of fresh Russian missile strikes on Ukraine. OPEC+ supply growth of 547,000 barrels per day in September remains a headwind, but geopolitical tensions in Eastern Europe are underpinning demand for crude.

- Treasury Yields Ease Ahead of Inflation Data: The US 10-year Treasury yield slipped more than 2 basis points to 4.209% as investors shifted focus to Friday’s PCE inflation release, the Fed’s preferred gauge. The 2-year yield edged slightly higher to 3.637%, reflecting caution around short-term policy expectations. Market participants also kept watch on political developments after President Trump’s dismissal of Fed Governor Lisa Cook sparked a legal challenge and renewed concerns over central bank independence.

FX Today:

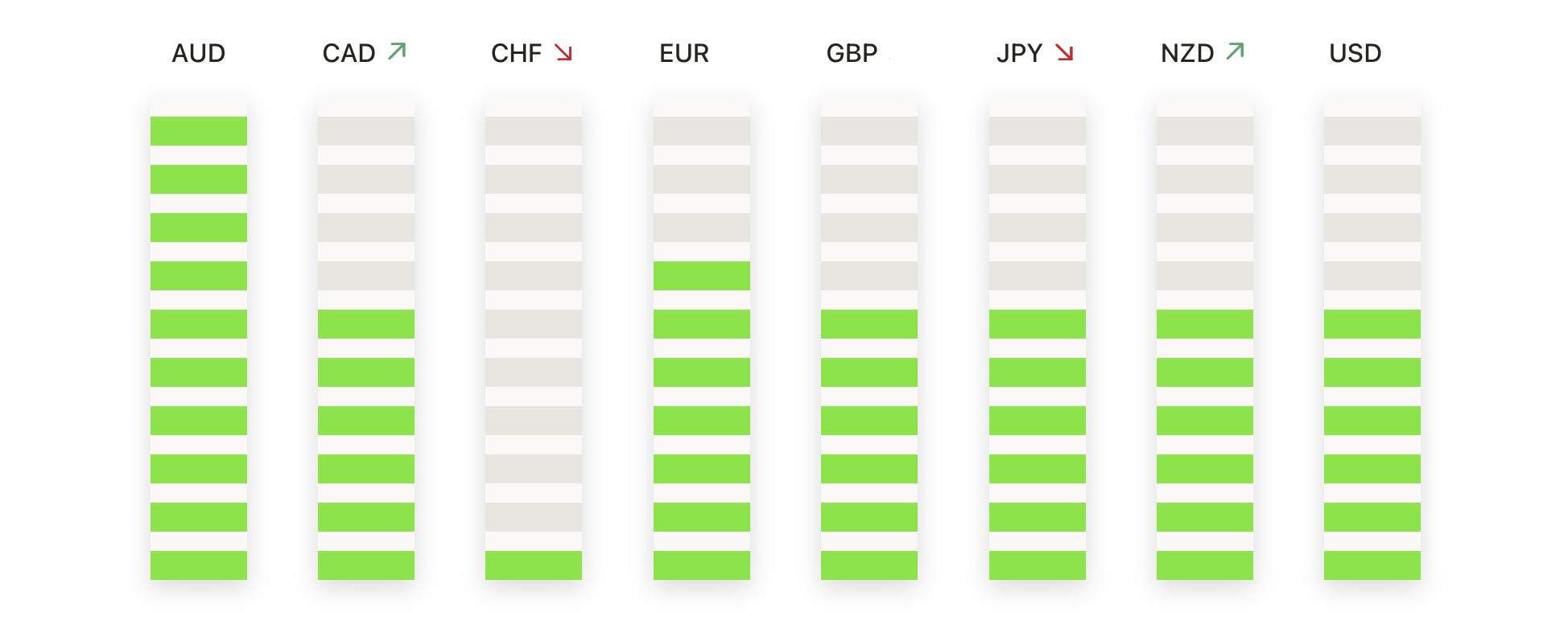

- EUR/USD Builds Momentum with Buyers Pressing Resistance: EUR/USD closed at 1.1683, up 0.38% after trading between 1.1629 and 1.1697, with a strong green candle leaving buyers in control into the close. The pair is holding above the 50-day SMA at 1.1659, underpinned by longer-term support from the 100-day at 1.1509 and 200-day at 1.1029. The recovery from August lows around 1.1500 has reinforced higher lows and a bullish bias, though resistance at 1.1700 remains the key hurdle. Unless sellers push the market back below 1.1600, the near-term outlook favours a break higher, with scope to test 1.1850 if momentum builds.

- GBP/USD Maintains Stability as Bulls Confront Barrier: GBP/USD settled at 1.3511, up 0.09% after trading between 1.3483 and 1.3531, with a modest green candle reflecting stability above support. The pair remains supported by the 50-day SMA at 1.3495 and the 100-day at 1.3442, while the 200-day at 1.3039 provides a broader floor. The recovery from early August lows near 1.3100 has shifted the bias back to the upside, though resistance at 1.3550 continues to cap progress. A sustained break above this level could open the way toward 1.3700, while dips toward 1.3450 are likely to attract demand.

- USD/JPY Softens as Repeated Rejections Cap Upside: USD/JPY closed at 146.93, down 0.31% after trading between 146.66 and 147.49, forming a red candle that highlighted renewed hesitation near resistance. The 50-day SMA at 146.96 is now capping upside attempts, while the 100-day at 145.48 and 200-day at 148.93 frame the wider structure. The pair remains stuck in consolidation between 146.50 and 147.50, with repeated rejection near the upper bound dampening momentum. Unless buyers reclaim the 200-day SMA at 148.93, the near-term bias looks soft, with a break below 146.50 exposing 145.80.

- AUD/USD Advances as Buyers Reclaim Key Moving Averages: AUD/USD finished at 0.6532, up 0.41% after trading between 0.6490 and 0.6538, with a solid green candle extending the rebound. The pair has regained the 50-day SMA at 0.6514, while the 100-day at 0.6474 and 200-day at 0.6386 remain supportive beneath. The recovery from the late-August low near 0.6400 has lifted the pair back toward the centre of its two-month range. Resistance is now in view at 0.6560 and then 0.6600, while support sits at 0.6500 and 0.6470. A decisive push above 0.6560 would reinforce the bullish outlook, opening the way toward 0.6650.

- Gold Strengthens as Bulls Drive Price Toward $3,440: Gold settled at $3,422, up 0.71% after trading between $3,384 and $3,423, closing near the session peak with a strong green candle. The metal is comfortably above its 50-day SMA at $3,349 and the 100-day at $3,321, while the 200-day at $3,067 continues to rise, confirming a solid uptrend. The recovery from mid-August has put buyers back in charge, with the move through $3,400 shifting bias firmly to the upside. Immediate resistance is marked at $3,440, while support is found at $3,380 and then $3,350. A sustained break higher could open the path toward $3,500, with dips expected to attract demand so long as price holds above $3,350.

Market Movers:

- Chipmakers Lead Tech Rally as AI Optimism Grows: Shares of Marvell Technology jumped over 4%, while Micron and Broadcom gained more than 3%, with AMD, Applied Materials and NXP Semiconductors also advancing as Nvidia’s results fuelled confidence in the sector.

- Snowflake Surges on Strong Earnings Beat: Snowflake rallied more than 18% after reporting product revenue of $1.09 billion against expectations of $1.04 billion and lifting its 2026 outlook.

- Pure Storage Soars on Upgraded Outlook: Pure Storage surged more than 31% after beating second-quarter revenue estimates at $861 million and raising its 2026 forecast.

- Food and Pharma Stocks Diverge on Results: Hormel Foods plunged 13% after weaker profit guidance, while Phibro Animal Health rose 18% on upbeat 2026 sales forecasts. Cooper Cos tumbled more than 12% after cutting revenue expectations.

- Cloud and Enterprise Software Mixed: Salesforce gained over 1% to lead the Dow higher, while Veeva Systems sank 7% on margin disappointment and Nutanix dropped 5% after soft revenue guidance, highlighting divergence within the sector.

- Consumer Names Face Tariff-Linked Headwinds: Brown-Forman slipped 4% after a miss on quarterly EPS, while Best Buy fell more than 3% despite beating forecasts, warning that tariffs continue to weigh ahead of the holiday season.

Wall Street extended its winning streak on Thursday as the S&P 500 closed at a fresh record, with Nvidia’s results reinforcing confidence in the artificial intelligence boom and sparking gains across technology sectors. Semiconductor and software stocks rallied broadly, offsetting lingering uncertainty over the Federal Reserve’s independence and upcoming trade negotiations. European markets ended mixed as investors digested corporate updates and regulatory developments, while Asia-Pacific trading showed little clear direction amid central bank policy decisions and fresh tariff pressures. With GDP growth revised higher and jobless claims easing, US economic data continued to point to underlying resilience. Attention now turns to Friday’s PCE inflation reading, which will be closely watched for its implications on the Fed’s next policy steps and the durability of recent market momentum.