US stocks ended the week on a strong note, with the Nasdaq closing at an all-time high after a tech-led rally spearheaded by Apple’s surge. Gains came as reports emerged that US and Russian officials are working on a potential agreement to end the war in Ukraine, allowing Moscow to retain occupied territories. The iPhone maker’s commitment to expand domestic manufacturing lifted sentiment in the sector, offsetting some caution over President Donald Trump’s newly enacted reciprocal tariffs. Oil prices steadied after a sharp weekly drop, while Treasury yields ticked higher as traders positioned ahead of key US inflation data due next week.

Key Takeaways:

- Dow Rises as Week Ends on Positive Note: The Dow Jones Industrial Average gained 206.97 points, or 0.47%, closing at 44,175.61. The index advanced about 1.4% over the week, supported by strength in technology and optimism over geopolitical developments.

- S&P 500 Nears Record Close: The S&P 500 rose 0.78% to finish at 6,389.45, just shy of a record, delivering a 2.4% gain for the week. Strength in large-cap technology shares and easing concerns over tariff impacts drove broad-based buying.

- Nasdaq Hits Record High: The Nasdaq Composite jumped 0.98% to a record 21,450.02, adding 3.9% for the week. Apple led the rally, surging 13% over the period after pledging to spend $600 billion on US manufacturing and benefiting from tariff exemptions.

- Europe Gains on US-Russia Peace Reports: European markets ended the session higher after reports that Washington and Moscow are working on a deal to halt the war in Ukraine, potentially allowing Russia to retain occupied territories. The STOXX 50 rose 0.4% on Friday, delivering a strong 3.6% weekly advance, while the pan-European STOXX 600 gained 0.3% on the day and 2.2% over the week. London’s FTSE 100 edged up 0.3% this week to 9,095.73, Paris’ CAC 40 climbed 0.54%, Milan’s FTSE MIB rose 0.56%, and Frankfurt’s DAX ended flat but posted a gain of more than 3% for the week, aided by solid Q2 earnings across key sectors. Bank stocks outperformed, with BBVA, BNP Paribas, and UniCredit all up more than 2%, while auto makers Volkswagen, Mercedes-Benz, and Stellantis also gained over 2%.

- Asia-Pacific Mixed as Tariff Concerns Linger: Asian markets closed mostly lower, weighed by renewed trade tensions and softer Wall Street cues, though Japan outperformed. Hong Kong’s Hang Seng fell 0.89% and mainland China’s CSI 300 dipped 0.24% to 4,104.97, pressured by weakness in property and technology shares. In Japan, the Nikkei 225 surged 1.85% and the Topix gained 1.21% after a week of choppy trade, though gains were capped by weaker-than-expected June household spending data showing a 1.3% year-on-year rise versus forecasts of 2.6%. The data highlighted ongoing pressure on consumption from higher food prices, with rice spending dropping at the fastest pace since 2022. South Korea’s Kospi fell 0.55%, while the Kosdaq rose 0.43%, and Australia’s S&P/ASX 200 eased 0.28% as miners slipped. In Southeast Asia, Jakarta’s Composite rallied more than 2% to its highest since late July, Kuala Lumpur’s Bursa added 0.4%, while Singapore’s Straits Times Index lagged. India’s Nifty 50 and Sensex both declined 0.95%, marking a fifth consecutive weekly loss for the rupee as US-India trade tensions deepened following President Trump’s 50% tariff on Indian goods.

- Oil Steadies After Steep Weekly Drop: Brent crude rose 0.2% to $66.59 a barrel while WTI was flat at $63.88. Prices fell over 4% and 5% respectively for the week as tariff-related economic concerns and an OPEC+ supply increase weighed on sentiment. Traders also monitored reports of a potential US-Russia agreement on Ukraine ahead of a planned Trump-Putin summit.

- Treasury Yields Edge Higher Ahead of Inflation Data: The 2-year yield rose 3 basis points to 3.764%, the 10-year climbed over 4 basis points to 4.285%, and the 30-year increased 4 basis points to 4.852%. Investors are awaiting next week’s US CPI and PPI reports, which could shape expectations for the Federal Reserve’s September policy meeting.

FX Today:

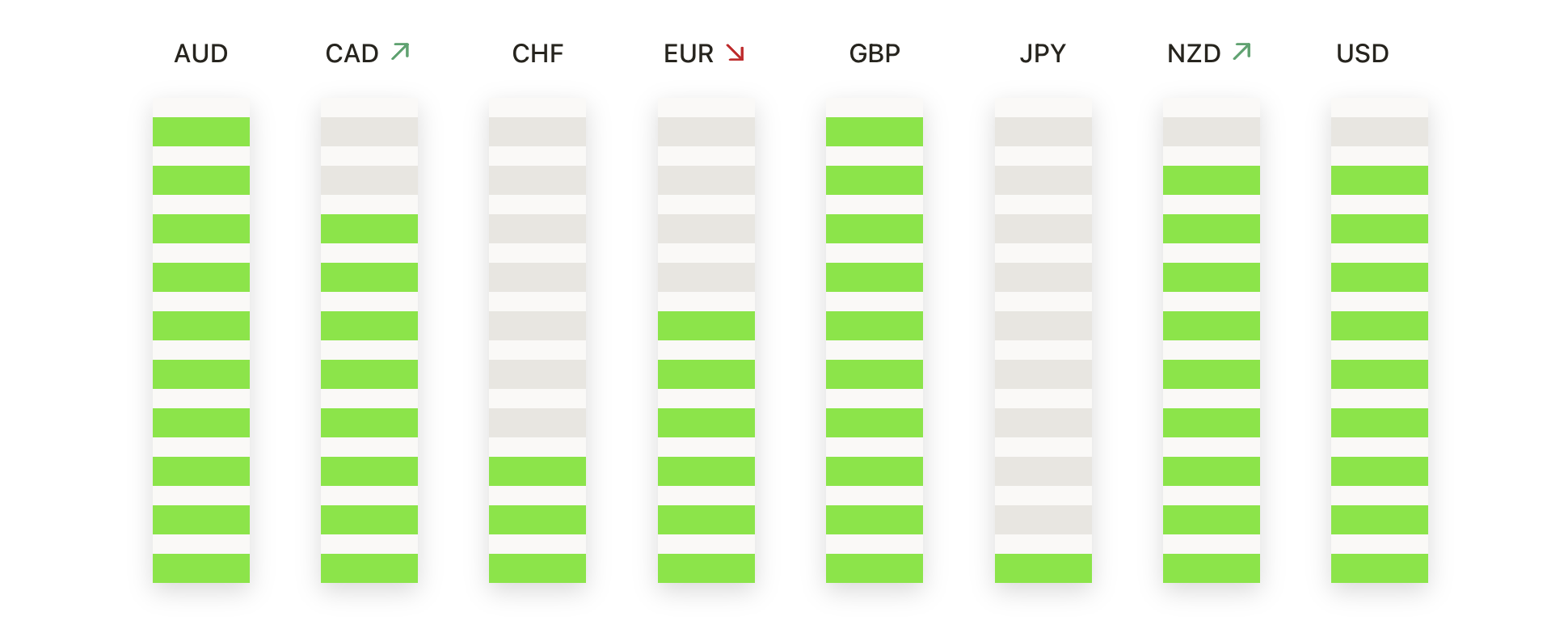

- EUR/USD Steadies Above Support as Bulls Target 1.1150 Breakout: EUR/USD closed at 1.1128, up 0.04%, after trading between 1.1101 and 1.1140. The pair remains supported by the 50-day average at 1.1084, the 100-day at 1.1020, and the 200-day at 1.0844, all sloping higher to confirm a steady medium-term uptrend. Price has been consolidating in a tight band between roughly 1.1080 and 1.1150 since mid-July, following a strong rally from early June’s low near 1.0700. The structure of higher lows since late May keeps the bias pointed upward, with the July peak at 1.1150 now the key level for a breakout toward 1.1200 and then 1.1270. Holding above 1.1100 should maintain upward pressure, while a drop below 1.1080 would bring the 1.1050 area and the 100-day average back into focus.

- GBP/USD Holds Gains as Price Approaches 1.3500 Resistance: GBP/USD settled at 1.3451, up 0.06%, after ranging between 1.3418 and 1.3459. The pair is above the 100-day average at 1.3361 and the 200-day at 1.2993, though still capped just under the 50-day at 1.3505, which has flattened after recent declines. Price has been climbing steadily from last week’s low near 1.3250, building higher lows that reinforce short-term bullish control. A close above 1.3500 would open the path toward 1.3550–1.3600, while failure to clear the 50-day could see a move back toward 1.3400. Below there, the 100-day at 1.3360 is the first key support, followed by 1.3300 and 1.3250.

- USD/JPY Holds Above 147.50 But Faces 200-Day Average Barrier: USD/JPY closed at 147.74, up 0.43%, after moving between 146.72 and 147.91. The pair remains above the 50-day average at 146.04 and the 100-day at 145.63, but the 200-day near 149.36 continues to slope lower, capping recent rallies. Support around 147.00 has kept the short-term bias constructive, with a push through 148.00–148.50 needed for another test of the 200-day. A daily close above 149.40 would shift the medium-term view to bullish, while a drop back under 147.00 could bring 146.00 and 145.00 back into play.

- Gold Holds Below $3,410 Resistance: Gold ended around $3,399, down 0.04%, after trading between $3,375 and $3,409. Price finished just under the session high, maintaining a constructive tone after a week of steady gains. The metal remains well supported by the rising 50-day average at $3,348, while the 100-day at $3,280 and the 200-day at $3,013 confirm the broader uptrend. Since late June, successive higher lows have underpinned momentum, with the $3,360–$3,370 zone acting as a strong technical base. A clean break above $3,410 would likely draw momentum buying toward $3,430 and then the $3,450–$3,470 band, which capped rallies in late June and mid-July. Failure to clear $3,410 could lead to a consolidation back toward $3,380, with a deeper slide below $3,360 shifting focus to the 100-day average.

- Silver Approaches $38.50 Barrier: Silver closed at $38.39, up 0.38%, after trading between $38.01 and $38.48. The metal extended its rebound from the $37.00 support area earlier in the week. The 50-day average at $36.85, along with the 100-day at $34.79 and the 200-day at $33.08, are all trending higher, confirming the strength of the medium-term uptrend. Price action since June has formed a rising channel with consistent higher highs and higher lows, and the $38.00–$38.10 area now serves as immediate support following the latest breakout attempt. A decisive move above $38.50 would expose $38.90 next and then the July peak near $39.50, while a reversal below $38.00 could trigger a deeper pullback toward $37.50.

Market Movers:

- Apple Extends Rally on Manufacturing Commitment: Apple gained over 4%, continuing a three-session run that has added more than 12% after President Trump confirmed the company will invest an additional $100 billion in US manufacturing, benefitting from tariff exemptions.

- Gilead Sciences Jumps on Strong Sales and Upgraded Outlook: Gilead Sciences rose more than 8% after reporting Q2 product sales of $7.05 billion, ahead of the $6.94 billion consensus.

- Monster Beverage Advances on Solid Quarterly Sales: Monster Beverage climbed more than 6% after reporting Q2 net sales of $2.11 billion, exceeding estimates of $2.08 billion.

- Trade Desk Plunges on Disappointing Earnings Reaction: Trade Desk dropped more than 38% despite Q2 adjusted EPS of $0.41 topping the $0.40 consensus, as analysts flagged underwhelming guidance.

- Sweetgreen Falls on Wider Loss and Sales Forecast Cut: Sweetgreen sank over 22% after posting a Q2 loss of $0.20 per share, wider than the $0.13 expected.

- Twilio Slides on Weak EPS Outlook: Twilio lost over 19% after projecting Q3 adjusted EPS of $1.01–$1.06, below the $1.14 estimate.

- Goodyear Tire & Rubber Drops on Surprise Loss: Goodyear fell over 18% after reporting a Q2 loss of $0.17 per share, versus expectations for a $0.19 profit.

- Pinterest Weakens on EPS Shortfall: Pinterest slid over 10% after posting Q2 adjusted EPS of $0.33, missing the $0.36 consensus.

Markets wrapped up the week in an upbeat mood, with a record close for the Nasdaq and optimism over potential progress in US-Russia talks helping offset lingering concerns about trade policy. Apple’s surge provided a powerful lift to the tech sector, while European equities gained on geopolitical hopes and Asian markets reflected a more cautious stance amid tariff tensions. Oil steadied after sharp weekly losses, and Treasury yields edged higher as investors positioned for next week’s key US inflation data. With geopolitical negotiations, trade developments, and economic indicators all in play, the coming sessions are set to test whether this week’s positive momentum can carry through.