A soft private payrolls report and lingering trade tensions cast a shadow over Wall Street on Wednesday, halting the Dow’s recent winning streak. The blue-chip index slipped as investors weighed signs of slowing job growth against resilient tech sector strength. In contrast, the S&P 500 ended flat, while the Nasdaq edged higher, supported by semiconductor stocks. European markets advanced as optimism around US-EU trade talks lifted sentiment, while Asian equities rallied on political developments and tech sector gains. Falling oil prices and sliding Treasury yields reflected caution across global markets.

Key Takeaways:

- Dow Snaps Four-Day Win Streak on Weak Payrolls Data: The Dow Jones Industrial Average fell 91.90 points, or 0.22%, to close at 42,427.74, ending a four-session rally. The move lower followed the weakest ADP private payrolls report in over two years, stoking concerns about the resilience of the US economy.

- S&P 500 Ends Flat as Investors Weigh Mixed Signals: The S&P 500 made a small gain of 0.01% to finish at 5,970.81. While strength in technology and semiconductor shares provided support, broader caution persisted due to disappointing labour market figures and concerns about global trade tensions.

- Nasdaq Climbs on Semiconductor Momentum: The Nasdaq Composite rose 0.32% to 19,460.49, extending recent gains driven by semiconductor stocks. ON Semiconductor, Marvell Technology, and other chipmakers rallied after signs of improving demand trends. Tech optimism helped the index shake off broader market worries.

- Europe Markets Rise on Trade Talks Progress and Eurozone News: European markets closed higher as EU trade chief comments signalled that talks with the US were “advancing in the right direction.” The Stoxx Europe 600 rose 0.5%, the DAX climbed 0.77%, the CAC 40 added 0.60%, while the FTSE 100 edged up 0.16%. Separately, Bulgaria secured approval to join the eurozone starting in January 2026, marking an expansion of the currency bloc to 21 members. The move added to positive regional sentiment.

- Asia Stocks Rally Led by South Korea Election and AI Optimism: Asia-Pacific markets advanced on Wednesday, tracking Wall Street’s tech-driven gains. South Korea’s Kospi surged 2.66% to 2,770.84, its highest since August, after opposition leader Lee Jae-myung won the presidential election and pledged reforms to enhance corporate governance. The Kosdaq rose 1.34%. Nvidia shares jumped nearly 3%, helping its market cap surpass Microsoft’s, while Broadcom and Micron Technology rallied over 3% and 4%. In Japan, the Nikkei 225 climbed 0.8% and the Topix rose 0.51%, led by AI and chip stocks. Australia’s ASX 200 gained 0.89%, despite Q1 GDP growth of 1.3% falling short of expectations. India’s Nifty 50 and Sensex each rose 0.29%. Meanwhile, China’s CSI 300 edged up 0.43%, and Hong Kong’s Hang Seng added 0.6%, as trade tensions lingered after President Trump described talks with China as “extremely hard.”

- Global PMIs Show Mixed Economic Trends: PMI data showed uneven momentum across Europe and the UK. The eurozone composite PMI fell to 50.2 in May, with the services index slipping to 49.7, marking the sector’s first contraction since late 2024. Germany’s composite PMI declined to 48.5, while its services reading dropped to a 30-month low of 47.1. France’s composite improved to 49.3 and services rose to 48.9, the strongest since December. Italy’s composite rose to 52.5, with services climbing to 53.2. Spain’s composite eased to 51.4, while services slowed to 51.3. In the UK, the composite PMI rebounded to 50.3, while the services index rose to 50.9, signalling modest expansion. The data reflected stabilisation in southern Europe and the UK, but continued softness in Germany’s key service sector.

- US Treasury Yields Tumble on Weak Payrolls and Services Data: Treasury yields fell sharply after ADP private payrolls showed only 37,000 new jobs and ISM services unexpectedly contracted. The 10-year yield dropped over 10 basis points to 4.357%, while the 2-year yield fell to 3.866%. The soft data reinforced investor expectations of possible Fed rate adjustments.

- Oil Prices Fall on Rising OPEC+ Output and Trade Fears: Oil prices retreated after news of higher OPEC+ production and ongoing global demand concerns amid escalating trade tensions. Brent crude settled at $64.86 per barrel, down 1.17%, while WTI closed at $62.74 per barrel, down 1.06%. US stockpile data and Canadian wildfire impacts remained in focus.

- US Private Sector Job Growth Slows Sharply as Services Sector Contracts: ADP reported private sector payrolls rose by just 37,000 in May, the weakest reading since March 2023 and far below the consensus forecast of 110,000. In addition, the ISM services index fell to 49.9, missing expectations of 52.1 and slipping below the expansion threshold. The combined data raised fresh concerns about US economic momentum ahead of Friday’s key nonfarm payrolls report.

FX Today:

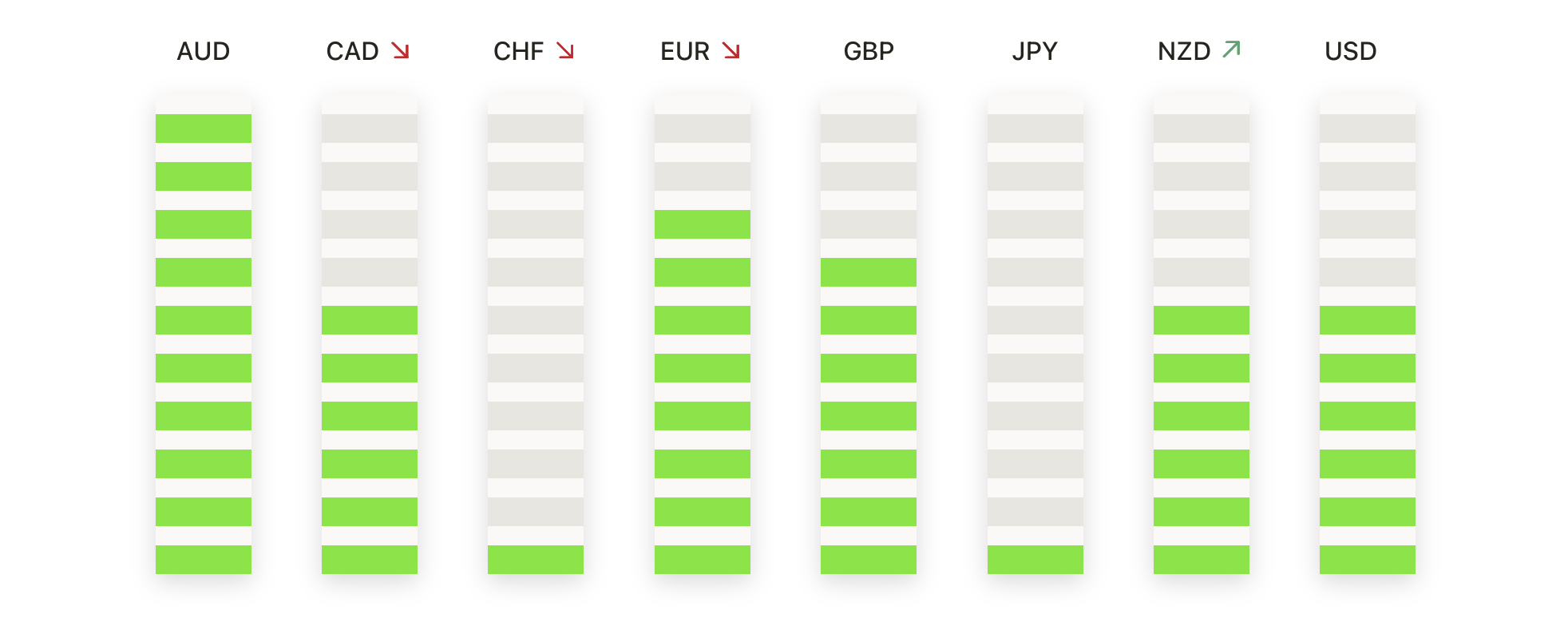

- EUR/USD Presses Higher Toward 1.1500: EUR/USD climbed further on Wednesday, closing at 1.1412, a gain of 0.38% for the day. The pair has been building on a series of higher lows since mid-April, supported by firm eurozone data and easing inflation fears. Technically, the pair remains well above the 50-day SMA at 1.1231 and the 100-day SMA at 1.0899. After consolidating around the 1.1350 zone, buyers are targeting the 1.1500 resistance area, with potential to test the April high of 1.1600 if bullish momentum continues. Initial support lies near 1.1300, followed by the rising 50-day SMA.

- GBP/USD Maintains Bullish Bias Above 1.3500: GBP/USD extended its advance on Wednesday, closing at 1.3547, up 0.22% on the session. The pair remains in a well-defined uptrend, comfortably trading above the 50-day SMA at 1.3253 and the 100-day SMA at 1.2946. Immediate resistance is seen near 1.3600, with scope to challenge the March high at 1.3700 on further gains. Key support levels are located at 1.3450 and 1.3400. Sterling remains underpinned by improving UK data and stable policy expectations, while softness in the US dollar continues to fuel the rally.

- USD/CHF Weakens Further Toward 0.8150: USD/CHF extended its recent losses on Wednesday, settling at 0.8189, a drop of 0.59%. The pair has remained under sustained pressure since mid-April, consistently trading below key moving averages. The 50-day SMA at 0.8338 and the 100-day SMA at 0.8653 are both sloping lower, confirming a bearish trend. Immediate focus is on the 0.8150 level, with further downside toward 0.8050 if selling persists. Resistance is now seen at 0.8300 and 0.8450. Safe-haven demand for the Swiss franc and broad dollar weakness remain dominant drivers.

- USD/JPY Slides Toward 143.00 as Bearish Momentum Builds: USD/JPY declined sharply on Wednesday, closing at 142.89, down 0.74% on the session. The pair has extended its recent downtrend after failing to hold above the 144.00 level. Technical signals remain bearish, with the pair trading below its 50-day SMA at 144.77, and lower 100-day and 200-day SMAs. Immediate support lies near 142.00, with risk of a deeper pullback toward the 140.00 psychological level if selling accelerates. Resistance is now at 144.00 and near the 50-day SMA. Ongoing yield differentials and safe-haven flows are likely to drive near-term direction.

- Gold Pushes Higher Toward $3,400 on Renewed Buying Interest: Gold advanced on Wednesday, closing at $3,373, up 0.59% for the day. The metal extended its rebound after finding strong support above $3,250 last week. Technically, gold remains firmly in an uptrend, with the 50-day SMA at $3,242 rising steadily. Buyers are eyeing a break of the $3,400 resistance zone, with potential to retest the $3,450 record high. On the downside, support is seen at $3,300 and the 50-day SMA. Ongoing geopolitical risks, inflation concerns, and central bank demand continue to underpin bullish sentiment in gold.

Market Movers:

- Marvell Technology Jumps on Improving Demand: Marvell Technology gained more than 6%, leading Nasdaq 100 gainers, as chip stocks extended their recent rally driven by optimism in AI and high-performance computing markets.

- Guidewire Software Soars on Upgraded Outlook: Guidewire Software jumped more than 15% after raising full-year revenue guidance above consensus expectations, boosting investor confidence in its growth prospects.

- Dollar Tree Slumps on Weak Outlook: Dollar Tree tumbled more than 8%, leading S&P 500 decliners, after issuing a weaker-than-expected 2026 sales forecast.

- CrowdStrike Slides on Lower Guidance: CrowdStrike fell more than 5% after posting Q1 subscription revenue below estimates and cutting its 2026 adjusted operating income forecast.

- Flowserve Drops on Merger Announcement: Flowserve declined more than 6% after announcing an all-stock merger with Chart Industries, which will see Chart shareholders receive 3.165 Flowserve shares for each Chart share.

- ON Semiconductor Leads Chipmaker Rally: ON Semiconductor surged over 5% after reporting signs of a broad-based recovery in demand. The upbeat outlook lifted sentiment across the semiconductor sector.

Markets ended the day with a mixed tone as investors weighed soft US payrolls and services data against ongoing resilience in tech stocks. The Dow’s pullback underscored caution ahead of Friday’s key nonfarm payrolls report, while the S&P 500 and Nasdaq found support from semiconductor strength. European markets were lifted by progress in trade talks and positive regional developments, though PMI data signalled uneven growth. In Asia, optimism around South Korea’s election and AI momentum drove gains. With economic signals mixed, traders now turn their attention to upcoming labour data and evolving trade policy dynamics.