Wall Street remained under pressure on Wednesday as the S&P 500 recorded a fourth straight decline and the Nasdaq fell for a second consecutive session, dragged lower by losses in technology and semiconductor names. Investors digested a wave of corporate earnings and the Federal Reserve’s July meeting minutes, which highlighted concerns about both inflation and the labour market. In Europe, defence stocks extended steep losses as diplomatic momentum around Ukraine weighed on the sector, while broader bourses delivered a mixed showing. Asian equities tracked Wall Street declines, with Japan leading losses after its steepest export contraction in over four years. Meanwhile, US Treasury yields edged lower after the Fed minutes, oil firmed on inventory drawdowns and geopolitical risk, and UK inflation surprised to the upside, complicating the policy outlook for the Bank of England.

Key Takeaways:

- Dow Holds Near Flatline Amid Tech Pressure: The Dow Jones Industrial Average edged higher by 16.04 points, or 0.04%, to close at 44,938.31. Despite the muted move, the index remains near record levels, with investors cautious ahead of Jerome Powell’s upcoming speech.

- S&P 500 Falls for Fourth Session: The S&P 500 slipped 0.24% to 6,395.78, extending its losing streak to a fourth consecutive day as profit-taking in technology and semiconductors deepened. Nvidia ended only marginally lower, but AMD and Broadcom lost about 1%, while Intel dropped sharply by 7%. The steady retreat reflects valuation concerns amid thin August trading volumes.

- Nasdaq Suffers Back-to-Back Losses: The Nasdaq Composite declined 0.67% to 21,172.86, marking a second straight loss and underscoring fragility in the AI trade. Mega-cap names including Apple, Amazon, Alphabet and Meta all fell more than 1%, while Palantir lost about 1%.

- Europe Mixed as Defence Stocks Sink Again: European equities delivered a mixed performance, with defence names dragging after renewed hopes for a Ukraine ceasefire. The Stoxx Europe Aerospace and Defence index fell 1.13% after Tuesday’s 2.6% drop, reflecting speculation about a diplomatic breakthrough. Headline moves were uneven, with the Euro Stoxx 50 down 0.2% to 5,472, France’s CAC 40 off 0.08% at 7,973.04, Italy’s FTSE MIB down 0.4% to 42,865, and Germany’s DAX lower by 0.60%, while the pan-European Stoxx 600 rose 0.3% to 559 and the UK’s FTSE 100 gained 1.08% to 9,288.14. Macro signals were mixed as well, with Eurozone CPI steady at 2.0% year on year and core at 2.3%, and Germany’s producer prices down 1.5% year on year in July, a larger fall than expected. Crucially for the policy outlook, UK inflation surprised to the upside at 3.8% year on year in July, with core also at 3.8% and services inflation rising to 5.0%, a combination that reduces the likelihood of additional Bank of England rate cuts this year. UK housing data showed June house prices up 3.7% year on year, while private rents rose 5.9% in July, the slowest annual increase since January 2023. Sweden’s Riksbank held its policy rate at 2.00%, noting inflation remains above the 2.0% target even as growth stays subdued.

- Asia Declines on Weak Japan Trade Data: Asian markets mostly tracked Wall Street’s pullback, with Japan leading losses after reporting exports fell 2.6% in July, the steepest drop in more than four years. The Nikkei 225 shed 1.51% to 42,888.55, while the Topix lost 0.57%. SoftBank dropped over 9% after announcing a $2 billion Intel investment, mirroring US tech weakness. South Korea’s Kospi fell 0.68% and the Kosdaq 1.31%. Taiwan’s Taiex slid nearly 3% to 23,625.44, while Australia’s S&P/ASX 200 managed a 0.25% gain after early losses. By contrast, Chinese equities firmed, with the CSI 300 up 1.14% and the Hang Seng reversing higher by 0.21% as Beijing held key lending rates steady. India outperformed regionally, with the Nifty 50 up 0.27% and Sensex up 0.32%, supported by 2% growth in infrastructure output.

- Oil Firms on Inventory Draw and Geopolitics: Brent crude rose 1.85% to $67.01 a barrel, while WTI gained 1.25% to $63.13. Prices were supported by API data showing a US crude inventory decline and expectations around next steps in Ukraine ceasefire talks. The gains followed a more than 1% slide on Tuesday, when optimism around peace progress briefly pressured energy markets.

- Treasury Yields Ease After Fed Minutes: US Treasury yields edged lower as markets digested the Fed’s July minutes. The 10-year yield slipped to 4.289%, while the 2-year yield was little changed at 3.748%. The minutes showed a rare dissent, with Governors Christopher Waller and Michelle Bowman opposing the hold decision, the first double dissent since 1993. Policymakers acknowledged risks to both inflation and employment, though most judged inflation the greater threat. Traders now see around an 84% chance of a rate cut in September, with attention fixed on Powell’s Jackson Hole remarks on Friday.

FX Today:

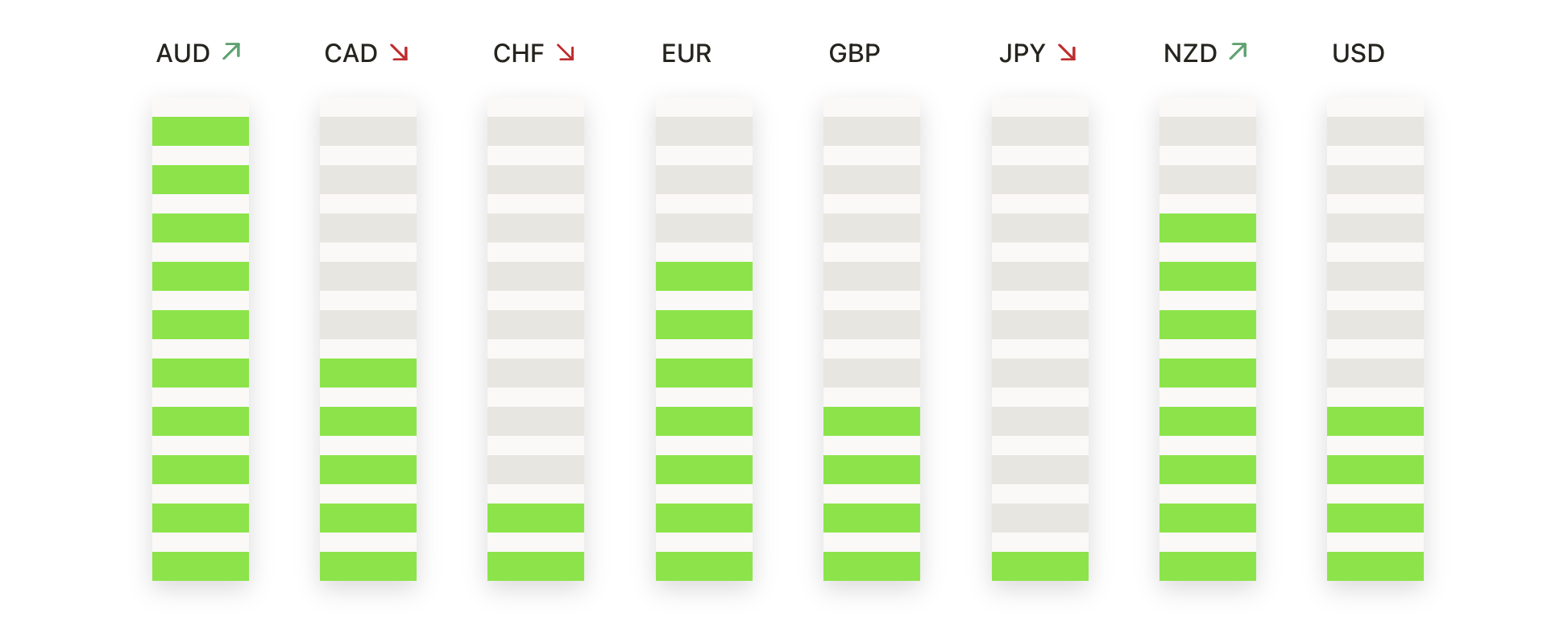

- EUR/USD Presses Lower as Sellers Drive Break Beneath 50-Day SMA: EUR/USD finished at 1.1653, down 0.36% after trading between 1.1645 and 1.1700, with the daily candle forming a solid red body that confirmed fading momentum. The break beneath the 50-day SMA at 1.1685 shifted near-term bias to the downside after repeated failures to sustain traction above 1.1750. Structurally, the pair has been consolidating since July, carving out lower highs under 1.1800 while support at 1.1650 has been tested several times. The 100-day SMA at 1.1609 now emerges as key support, while the longer-term picture remains underpinned by a rising 200-day SMA at 1.1407. A close below 1.1600 would expose deeper downside towards 1.1500 and June’s low at 1.1450, while buyers would need to reclaim 1.1700 then 1.1750 to restore bullish intent.

- GBP/USD Pulls Back as Sellers Cap Rally Near 1.3500: GBP/USD ended at 1.3452, down 0.30% after trading between 1.3447 and 1.3510, with the daily candle forming a red body that marked a pause in momentum. The pair slipped back beneath the 50-day SMA at 1.3499, tempering the recovery from July’s trough near 1.3050. Structurally, sterling has built a series of higher lows since mid-July, but resistance around 1.3500–1.3550 has repeatedly blocked progress. The 100-day SMA at 1.3407 is now immediate support, with the 200-day SMA rising steadily at 1.3016. A break below 1.3400 would risk a deeper retracement towards 1.3300 and July’s low, while a daily close above 1.3550 would reassert bullish control and set the stage for a retest of 1.3600.

- AUD/USD Slips as Sellers Test Support at 200-Day Average: AUD/USD closed at 0.6433, down 0.31% after trading between 0.6424 and 0.6457, with the daily candle leaving a small red body near the lower end of its range. The pair has slipped beneath the 50-day SMA at 0.6515, leaving short-term momentum in favour of sellers, while the 200-day SMA at 0.6385 stands as the next critical support. Structurally, the market has remained range-bound through the summer, capped by resistance at 0.6550–0.6600 and supported near 0.6400. The 100-day SMA at 0.6452 is currently being tested from above, reinforcing the importance of this zone. A daily close below 0.6400 would expose 0.6300 and June’s low near 0.6200, while buyers would need a push back above 0.6500 to regain traction.

- USD/JPY Holds Range as Momentum Stalls Below 148.00: USD/JPY closed at 147.37, down 0.19% after trading between 146.87 and 147.82, with the daily candle leaving a small red body that reflected hesitation. The pair is hovering near the 50-day SMA at 146.63, which has acted as short-term support after several retests. The broader trend context remains mixed, with the recovery from June’s low at 140.00 still intact but capped under the 200-day SMA at 149.15. Structurally, buyers have defended higher lows since May, yet resistance in the 149.00–150.00 area continues to limit momentum. A break above 148.00 would re-expose the 149.00 ceiling, while a close beneath 146.50 would risk opening a deeper retracement towards 145.50 and the June breakout zone near 144.00.

- Gold Pushes Higher as Buyers Defend 200-Day Support: Gold settled at $3,348, up 0.99% after trading between $3,312 and $3,350, with the daily candle forming a solid green body that reclaimed ground after recent weakness. Price held firm above the 200-day SMA at $3,304, signalling that buyers are defending long-term structural support. The broader pattern is one of consolidation, with repeated swings between ceiling resistance at $3,400 and support at $3,300. The 50-day SMA at $3,348 and the 100-day SMA at $3,304 provide additional layers of balance. A break above $3,400 would reassert bullish control and target $3,450, while a close beneath $3,300 would risk deeper retracement towards $3,250 and the June swing low near $3,200.

Market Movers:

- Tech Giants Retreat as Valuations Face Pressure: The Magnificent Seven dragged on indices as Apple, Amazon and Alphabet each lost more than 1%, Tesla also fell over 1%, Microsoft slipped 0.79%, Meta eased 0.50%, and Nvidia edged lower by 0.14%.

- James Hardie Plunges After Weak Quarter: James Hardie Industries tumbled more than 34% after reporting Q2 operating profit down 29% year on year. Management cited deteriorating housing conditions, with demand in the spring season at its weakest pace in over twelve years.

- Target Declines on Sales Outlook: Target shares sank more than 6% after the retailer projected full-year sales to fall worse than the consensus estimate of a 1.71% decline.

- La-Z-Boy Drops on Guidance Miss: La-Z-Boy lost more than 12% after reporting Q1 comparable sales down 4% year on year, compared with a 3% decline a year earlier. The company also guided Q2 sales to $510–$530 million, below the $528.5 million consensus midpoint.

- Hertz Gains on Amazon Partnership: Hertz Global Holdings rose more than 6% after confirming a tie-up with Amazon Autos to sell pre-owned cars on the platform.

Markets remained cautious on Wednesday as the Fed’s July minutes underscored divisions over inflation and employment risks, leaving investors focused on Jerome Powell’s upcoming remarks at Jackson Hole for clearer direction on policy. Wall Street extended losses, led by weakness in technology, while Europe and Asia posted mixed sessions weighed by sector-specific pressures and weak trade data. Oil firmed on inventory draws and geopolitics, US yields edged lower, and UK inflation surprised to the upside, complicating the Bank of England’s task.