Markets rallied strongly on Tuesday as hopes grew that a tentative ceasefire between Israel and Iran would hold, easing investor anxiety over further escalation in the Middle East. The Dow soared over 500 points, while the S&P 500 and Nasdaq also notched solid gains, with the tech-heavy Nasdaq closing at a new record. Oil prices plunged for a second consecutive session, boosting risk appetite and lifting travel-related stocks. Federal Reserve Chair Jerome Powell’s remarks to lawmakers struck a measured tone, reinforcing the central bank’s willingness to wait before adjusting interest rates. The overall mood turned decisively bullish as geopolitical risks faded and focus shifted back to policy and earnings.

Key Takeaways:

- Dow Jumps Over 500 Points as Truce Eases War Fears: The Dow Jones Industrial Average surged 507.24 points, or 1.19%, to close at 43,089.02, as investors welcomed signs that the fragile ceasefire between Israel and Iran would hold.

- S&P 500 Climbs Toward 52-Week High on Risk-On Mood: The S&P 500 advanced 1.11% to finish at 6,092.18, putting it within 0.9% of its 52-week high. The rally was broad-based, with tech, consumer discretionary, and industrials posting strong gains.

- Nasdaq Hits Fresh Record as Tech Stocks Lead Rebound: The Nasdaq Composite gained 1.43% to settle at 19,912.53, while the Nasdaq 100 climbed 1.53% to close at a new all-time high of 22,190.52. A resurgence in investor appetite for high-growth names powered the rally, with Nvidia rising 2.6% and Broadcom nearly 4%.

- European Shares Rally as Ceasefire Boosts Confidence: European markets ended sharply higher amid optimism that the Israel-Iran truce would hold, calming fears of wider conflict. The Stoxx Europe 600 rose 1.2%, led by industrials and financials. Germany’s DAX surged 1.60%, France’s CAC 40 added 1.04%, and Italy’s FTSE MIB climbed 1.63%. The FTSE 100 was flat, edging up just 0.01% as UK grocery price inflation rose to 4.7%, its highest level since March 2024. Meanwhile, Germany’s government announced an extra €19 billion in Q3 debt issuance to fund defence and infrastructure, drawing bond market attention.

- Asian Markets Advance After Trump Confirms Ceasefire: Asia-Pacific indices rallied strongly after President Trump confirmed the Israel-Iran ceasefire was in effect, easing investor nerves across the region. Japan’s Nikkei 225 rose 1.14% and the Topix gained 0.73%, while South Korea’s Kospi jumped 2.96% and the Kosdaq added 2.06%. Australia’s ASX 200 climbed 0.95%, supported by strength in tech and energy names. Hong Kong’s Hang Seng rose 2.06%, and China’s CSI 300 advanced 1.2% as mainland investors responded positively to reduced global tensions.

- Oil Craters as Geopolitical Premium Evaporates: Oil prices dropped for a second day as investors unwound risk premiums tied to Middle East conflict. US crude slid 5.17% to $64.97 a barrel, and Brent declined 5.19% to $67.77. The two-day loss now exceeds 13%, wiping out the gains made after the initial Israeli strikes. Trump’s announcement that China can resume buying Iranian oil also pressured prices lower. With supply disruption fears fading, traders are repositioning for a more stable outlook.

- Yields Decline as Powell Reiterates Patient Stance: Treasury yields slipped despite Powell’s comments that the Fed would wait before cutting rates. The 10-year yield eased 3.1 basis points to 4.291%, the 2-year dipped to 3.815%, and the 30-year fell to 4.832%. Markets interpreted the Fed’s tone as pragmatic amid tariff uncertainty, while the ceasefire in the Middle East further calmed bond markets. Traders now anticipate a more measured path for monetary easing in the months ahead.

- Consumer Confidence Slips Amid Job Market Concerns: US consumer confidence fell more than expected in June, with the Conference Board’s index dropping to 93.0 from 98.4. Fewer respondents viewed jobs as plentiful, and more expressed doubts about income growth and major purchases. Rising household concerns over tariffs and price pressures weighed on the survey, signalling potential softness in future spending. The data added to signs that labour market momentum may be weakening.

FX Today:

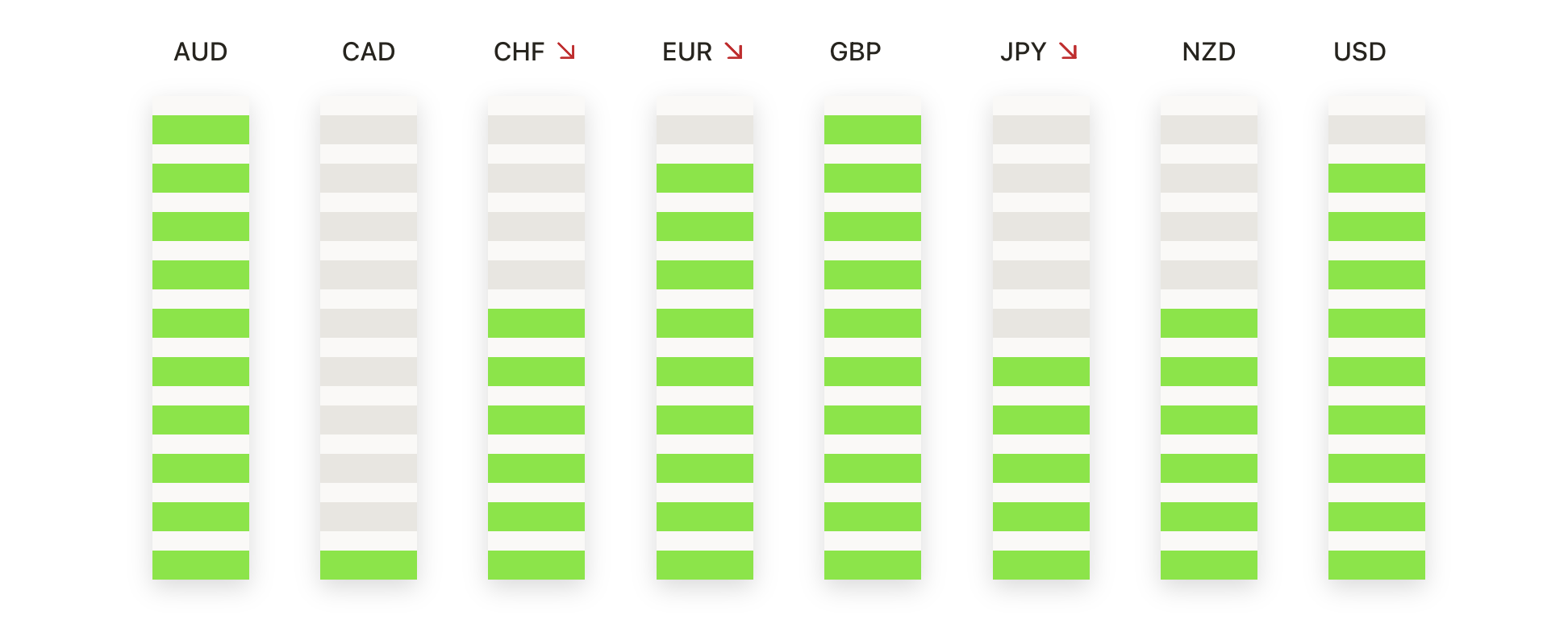

- EUR/USD Pushes to 13-Month High as Bullish Momentum Holds: The EUR/USD pair closed at 1.1614, rising 0.33% after trading between 1.1576 and 1.1614. It was the third consecutive daily gain and marked the highest close since May 2024, as euro strength held firm amid weakening dollar demand. The trend remains well-supported, with the pair positioned above its 50-day, 100-day, and 200-day SMAs at 1.1371, 1.1049, and 1.0847 respectively. Resistance is now seen at 1.1650 followed by 1.1720, while support lies at 1.1550 and the 50-day average below. A break above 1.1650 would likely attract additional momentum buyers, potentially opening the way to test yearly highs.

- GBP/USD Climbs Toward May High After Strong Rebound: GBP/USD ended at 1.3624, gaining 0.73% after trading between 1.3519 and 1.3649. The pair posted a solid bullish candle that erased last week’s losses and approached its highest level since early May. The uptrend remains supported by rising 50-day, 100-day, and 200-day moving averages, currently at 1.3412, 1.3107, and 1.2933 respectively. Immediate resistance stands at 1.3650, with a break above this level potentially targeting the 2024 high at 1.3740. Support sits at 1.3550, followed by the 50-day average near 1.3410.

- USD/CHF Extends Slide After Breaking Key Support Level: USD/CHF closed at 0.8050, falling 0.92% after ranging between 0.8130 and 0.8050. The pair posted a full-bodied red candle that broke through short-term support and registered its weakest close in weeks. Price action remains firmly bearish, with the pair trading below all major moving averages, including the 50-day at 0.8229, the 100-day at 0.8525, and the 200-day at 0.8669, each sloping lower. Immediate support is seen at the psychological level of 0.8000, followed by the year-to-date low near 0.7920. Resistance is now capped at 0.8130, while stronger resistance aligns with the falling 50-day average at 0.8220. Unless the pair reclaims these zones, the path of least resistance continues to point downward. A bounce would need to clear 0.8220 to ease downside pressure.

- USD/JPY Falls After Rejection from Key Averages Caps Rally: USD/JPY settled at 144.73 dropping 0.95% after ranging between 146.17 and 144.51. The pair posted a bearish engulfing candle that reversed Friday’s gains and confirmed strong selling pressure near the 100-day SMA at 146.67. Price also remains capped by the 200-day SMA at 149.48, and Monday’s close back below the 50-day average at 144.15 adds to the bearish case. The medium-term trend remains negative, with lower highs and downward-sloping averages reinforcing the structure. Key support lies at 144.00 followed by 143.20, while resistance sits at 145.50 and then 146.70.

- Gold Drops Below $3,330 as Rejection from Resistance Deepens: Gold settled at $3,323, falling 1.31% after trading between $3,296 and $3,370. The metal printed its sharpest one-day loss in over two weeks and closed decisively below the 50-day SMA at $3,318, negating last week’s recovery structure. Despite the loss, the longer-term trend remains constructive, with the 100-day and 200-day SMAs rising steadily at $3,138 and $2,897 respectively. Immediate support is now seen at $3,295 followed by $3,270, both of which align with recent swing lows and volume zones. Resistance stands at $3,360 and $3,375, and a strong close above these levels would be required to reinstate bullish control.

Market Movers:

- Carnival Jumps After Strong Q2 Results Beat Expectations: Shares of Carnival surged nearly 7% after the cruise line reported second-quarter earnings and revenue that topped analyst forecasts.

- Uber Rallies as Waymo Partnership Expands Robotaxi Access: Uber climbed nearly 8% after Waymo announced it would begin offering autonomous taxi rides in Atlanta via the Uber app.

- Advance Auto Parts Drops on Goldman Sachs Downgrade: Shares of Advance Auto Parts fell close to 7% after Goldman Sachs downgraded the stock to sell from neutral.

- CleanSpark Soars on Mining Milestone Announcement: Bitcoin miner CleanSpark jumped more than 13% after announcing it had reached its midyear operational hashrate target of 50 exahashes per second.

- Coinbase Rises as Crypto Rally Gains Traction: Coinbase shares rose 12% as cryptocurrencies advanced broadly in response to easing geopolitical tensions. Other crypto stocks followed suit, with Galaxy Digital up 5%, reflecting improved sentiment in the digital asset sector.

- Oil Stocks Decline on Middle East Ceasefire and Price Drop: Energy names traded lower following another sharp fall in oil prices. Exxon Mobil dropped more than 3%, while Chevron slipped 1.8%. The Energy Select Sector SPDR Fund (XLE) was down 1% as the Israel-Iran ceasefire reduced fears of supply disruption and triggered a retreat in crude prices.

Stocks extended their rally on Tuesday as investors grew more confident that the Israel-Iran ceasefire would hold, easing geopolitical risk and pushing oil prices sharply lower for a second straight session. The Dow, S&P 500 and Nasdaq all posted solid gains, supported by renewed risk appetite and strong performances in technology and travel stocks. Falling Treasury yields and a cautious stance from Fed Chair Jerome Powell reinforced the view that rate cuts are not imminent, but also not off the table. Meanwhile, disappointing US consumer confidence data added to signs of a softening job market. Looking ahead, attention shifts to upcoming inflation figures and any further developments in US fiscal and trade policy.