Stocks rose on Thursday as investors digested fresh signs of cooling US inflation, a mixed labour market, and weak economic data out of the UK. The producer price index edged up just 0.1% in May, below expectations, helping to ease concerns over persistent cost pressures. Jobless claims held steady at 248,000, but continuing claims rose to their highest level in more than three years, suggesting mounting strain in the labour market. In the UK, April GDP shrank by 0.3%, far worse than the anticipated 0.1% drop, adding to global growth worries. Despite macro headwinds, optimism around AI and cloud demand lifted sentiment, with Oracle soaring 13% on robust earnings and bullish guidance. Treasury yields fell, gold rallied, and the euro extended its breakout to fresh multi-year highs.

Key Takeaways:

- S&P 500 Rises Toward Record Highs: The S&P 500 gained 0.38% to close at 6,045.26, now sitting less than 2% below its all-time high. Tech optimism and inflation relief lifted the benchmark as Oracle led the advance and inflation data cooled concerns about rate pressure.

- Dow Adds Modestly Despite Boeing Drag: The Dow Jones Industrial Average added 101.85 points, or 0.24%, to finish at 42,967.62. Gains were limited as Boeing tumbled nearly 5% following a fatal crash involving one of its Dreamliner jets, overshadowing broader strength.

- Nasdaq Extends Gains on Tech Optimism: The Nasdaq Composite climbed 0.24% to end the session at 19,662.48, supported by a rally in Oracle and other cloud-related stocks. Sentiment remained strong as investors bet on AI-driven growth in the sector.

- Europe Slips as Tariff Tensions Mount and UK GDP Disappoints: European equities closed mostly lower on Thursday as tariff concerns and weak UK data weighed on sentiment. The Stoxx Europe 600 slipped 0.3 percent, while Germany’s DAX fell 0.74 percent and Italy’s FTSE MIB dropped 0.58 percent. France’s CAC 40 edged 0.1 percent lower. Despite the regional weakness, the UK’s FTSE 100 defied the trend and rose 0.23 percent to a record high of 8,884.92. UK GDP contracted 0.3 percent in April, far below the expected 0.1 percent decline, while exports to the United States saw their biggest drop since records began. German economic institutes raised their outlook for 2025 and 2026, projecting slow but improving growth.

- Asia Ends Mixed as Markets Eye China Trade Narrative: Asian markets posted mixed results as investors digested Trump’s remarks about a “done” deal with China, though no details were finalised. Japan’s Nikkei 225 dropped 0.65 percent to 38,173.09 and the Topix lost 0.21 percent. Australia’s ASX 200 declined 0.31 percent, and Hong Kong’s Hang Seng fell 1.11 percent. China’s CSI 300 ended flat. In contrast, South Korea’s Kospi rose 0.45 percent as unemployment fell to 2.8 percent, the lowest in a year, and the Kosdaq gained 0.4 percent. India’s Nifty 50 dipped 0.45 percent despite consumer inflation easing to 2.82 percent in May, a sign that price pressures may be abating faster than anticipated.

- Oil Retreats After Geopolitical Tensions Ease: US crude (WTI) dipped 0.16 percent to settle at $68.04 a barrel, while Brent fell 0.59 percent to $69.36. The mild pullback followed Wednesday’s 4% surge on Middle East fears. Trump’s comments suggesting no imminent Israeli strike on Iran helped ease supply disruption concerns, though risk remains if tensions escalate.

- Treasury Yields Drop on Benign Inflation Data: The 10-year yield fell 5 basis points to 4.361 percent, while the 2-year slid to 3.908 percent. Softer-than-expected PPI numbers, which rose just 0.1 percent in May, reinforced market expectations that inflation remains contained. A solid 30-year bond auction also supported demand.

- US Jobless Claims Flat but Continuing Claims Jump: Weekly jobless claims came in unchanged at 248,000, broadly in line with forecasts. However, continuing claims rose sharply to 1.96 million, which is the highest level since November 2021. This suggests that displaced workers are taking longer to find new employment. The data points to a labour market that remains stable but increasingly uneven.

FX Today:

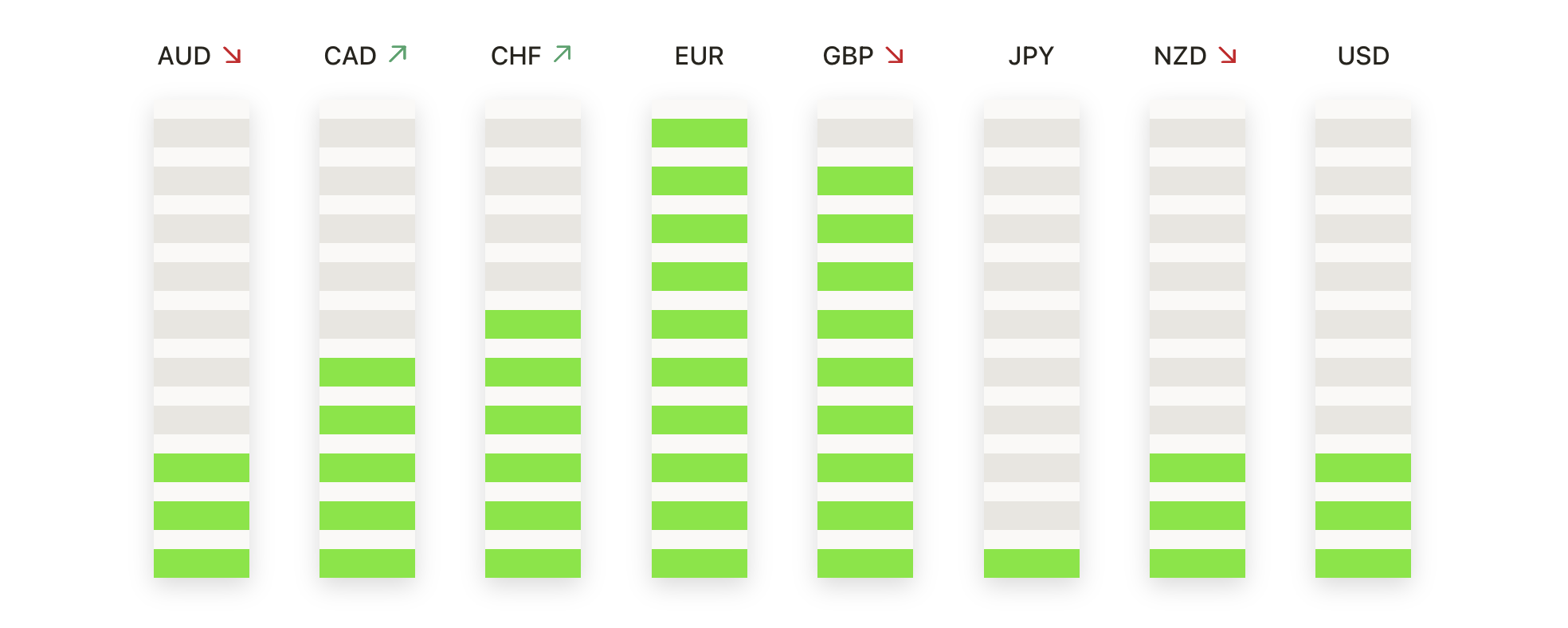

- Euro Smashes Past 1.1600 to Mark Strongest Close Since Early 2022: The EUR/USD pair closed at 1.1577 on Thursday, rising 0.78% as the euro extended its winning streak for a third day. The session high at 1.1631 marked the strongest level since early 2022, confirming a breakout above prior resistance. The technical backdrop remains bullish, with the 50-day SMA at 1.1304 rising above both the 100-day at 1.0959 and the 200-day at 1.0828. Immediate resistance is seen near 1.1650, while deeper targets include 1.1800. Pullbacks could find support around 1.1450 or the advancing 50-day average.

- Sterling Surges to 1.3623 as Uptrend Reaches New 2025 Peak: GBP/USD closed at 1.3603 on Thursday, gaining 0.41% and reaching its highest level since March 2022. Intraday price touched 1.3623 before settling slightly lower. The bullish trend has strengthened with price trading well above all major SMAs. The 50-day average has risen to 1.3323 and remains clearly above the 100-day at 1.3021 and the 200-day at 1.2918. Upside momentum remains strong, with resistance expected around 1.3750 and 1.3900. Key support zones sit at 1.3450 and 1.3300, the latter aligning with the 50-day average.

- Loonie Gains as USD/CAD Hits Lowest Close Since January: The USD/CAD pair settled at 1.3605 on Thursday, dropping 0.46% and recording its lowest close since early January. Selling pressure accelerated late in the session, pushing the pair down from an intraday high of 1.3668 to a low of 1.3599. The bearish technical trend remains intact. The 50-day SMA at 1.3856 continues to decline and stays well below the 100-day at 1.4089 and the 200-day at 1.4027. This full downward alignment confirms strong selling pressure. Support is now seen at 1.3550, with further downside risks pointing toward 1.3450. Resistance comes in at 1.3700, followed by the 50-day average near 1.3860.

- Swiss Franc Jumps Sharply as USD/CHF Collapses Below 0.8150: USD/CHF closed at 0.8111 on Thursday, sinking 1.10% for its steepest daily decline in nearly a month. After reaching a high of 0.8202 earlier in the session, the pair reversed abruptly and breached key support levels. The technical outlook is bearish, with the 50-day SMA at 0.8267 trending well below the 100-day at 0.8600 and the 200-day at 0.8683. Price action is now over 150 pips below the short-term average, confirming strong downside momentum. Immediate support lies at 0.8050, with the psychological 0.8000 level next in focus. Any rally attempt may struggle near 0.8200 or the descending 50-day SMA.

- Dollar Slides Against Yen as USD/JPY Extends Move Below 144: USD/JPY ended the day at 143.52 on Thursday, falling 0.70% as the pair resumed its downward trajectory. The session high of 144.54 was quickly rejected, and price dropped to its lowest level since late May. The 50-day SMA has declined to 146.17, remaining beneath the 100-day at 147.45 and the 200-day at 149.37. This formation supports the prevailing bearish tone. Short-term support is located at 143.00, followed by the May low near 141.60. Resistance is now firmly at 145.50 and 146.50.

- Gold Pushes Higher as Falling Yields Reinforce Bullish Setup: Gold settled at $3,388 on Thursday, climbing 0.93 percent as softer inflation data and falling yields renewed investor appetite. The metal briefly reached $3,399 intraday, nearing the May high of $3,420. The technical picture remains constructive, with the 50-day SMA rising to $3,275 and remaining well above the 100-day at $3,095 and 200-day at $2,867. Each pullback since April has found support at or above the 50-day average. A close above $3,420 would open up a potential move toward $3,500 or even the record high near $3,560. Key support levels include $3,300 and the rising 50-day moving average.

Market Movers:

- Oracle Jumps on Strong Cloud Outlook and Earnings Beat: Shares of Oracle surged 13% after the company reported fiscal Q4 results that topped analyst expectations. Earnings came in at $1.70 per share versus $1.64 expected, while revenue hit $15.9 billion.

- Boeing Slides Nearly 5% After Fatal Dreamliner Crash in India: Boeing fell sharply after an 11-year-old Air India 787 Dreamliner crashed following takeoff from Ahmedabad. The incident, involving 242 passengers and crew, is the first recorded crash of a Dreamliner aircraft.

- GameStop Tumbles 22.5% After Announcing Convertible Note Sale: GameStop sank after disclosing plans to sell $1.75 billion in convertible senior notes. The company said proceeds will be used for general corporate purposes, including investments.

- CureVac Soars on $1.25 Billion BioNTech Takeover: CureVac shares skyrocketed 38% after BioNTech announced it would acquire the German biotech firm in an all-stock deal valued at $1.25 billion.

- Chime Financial Pops 37% in Nasdaq Debut: Chime Financial closed at $37.11 on its first day of trading, up from its IPO price of $27. The online banking firm was valued at $11.6 billion at the offering. Strong investor demand lifted the stock well above its initial listing level.

- Voyager Technologies Falls After Volatile IPO Week: Voyager shares dropped 12.4% in their second day of trading, following an 82% jump on debut. The space technology firm closed at $49.45, down from Wednesday’s $56.48 as early gains were pared back by profit-taking.

Thursday’s market action reflected a balance between optimism over softer inflation data and caution surrounding global trade developments. Cooling wholesale prices and steady jobless claims helped calm investor nerves, sending Treasury yields lower and giving equities room to extend gains. Oracle’s strong earnings and cloud forecast gave tech stocks a boost, while Boeing’s drop limited broader upside. Meanwhile, the euro and pound rallied sharply, and gold approached key resistance as safe-haven demand returned.