Wall Street paused near record levels on Wednesday as investors weighed conflicting forces of tech optimism and geopolitical uncertainty. The S&P 500 ended virtually unchanged, holding within 1% of its all-time high, while the Nasdaq rose modestly and the Dow retreated. Momentum in artificial intelligence stocks, led by Nvidia’s record-breaking surge, helped offset weak housing data and caution around Middle East tensions. A fragile ceasefire between Israel and Iran continued to hold, easing fears of energy disruption. With easing trade worries and strong tech leadership, the broader market stayed on a steady path despite pockets of economic softness.

Key Takeaways:

- S&P 500 Holds Steady Near Record High: The S&P 500 ended the day little changed at 6,092.16, remaining within 1% of its all-time intraday and closing highs. Investors appeared cautious but steady, with the index up more than 2% so far this week amid easing geopolitical risk.

- Dow Slips While Nasdaq Gains on Tech Strength: The Dow Jones Industrial Average slipped 106.59 points, or 0.25%, settling at 42,982.43. Meanwhile, the Nasdaq Composite rose 0.31% to close at 19,973.55, supported by strong performances from Nvidia, Alphabet, and AMD.

- European Markets Fall Despite Defence Stock Surge: European equities declined broadly on Wednesday as concerns over slowing growth and tariff uncertainty weighed on sentiment. The Stoxx Europe 600 lost 0.74% to 536.99, led lower by banks and consumer staples. Germany’s DAX dropped 0.61%, with economic institutes cutting 2025 growth forecasts to just 0.1%. France’s CAC 40 shed 0.70%, while the FTSE 100 lost 0.46%. Spain confirmed weaker Q1 growth at 0.6% and downgraded its full-year outlook to 2.4%, still above the Eurozone’s 0.9% forecast. The Bank of Spain cited tariff wars involving the US, China, and Europe as a key headwind. Food producers like Danone fell sharply, while defence stocks including Rheinmetall and Babcock rallied on rising rearmament budgets.

- Asia-Pacific Markets Trade Mixed Amid Ceasefire Hopes and Fed Watch: Asia-Pacific equities were mixed as investors assessed geopolitical tensions and monetary policy signals. Japan’s Nikkei 225 rose 0.39% to 38,942.07, lifted by services inflation data and a rebound in industrial names. Hong Kong’s Hang Seng led regional gains with a 1.22% rise, and mainland China’s CSI 300 climbed 1.44%, both lifted by easing tensions in the Middle East. South Korea’s Kospi added 0.15%, though the Kosdaq slipped 0.34%. Australia’s ASX 200 was flat at 8,559.2 after May CPI fell to 2.1%, its lowest since October 2024. In Thailand, the SET Index fell 0.2% after the central bank held rates steady at 1.75%.

- Oil Rebounds After Ceasefire-Led Selloff: US crude futures climbed 1.30% to settle at $65.21 a barrel, recovering some ground after two days of steep losses triggered by a ceasefire between Iran and Israel. Brent crude gained 1.16% to close at $67.92. Both benchmarks had previously spiked to five-month highs following US airstrikes but tumbled when Iran refrained from targeting energy infrastructure. BP shares briefly jumped on acquisition rumours involving Shell, though the latter denied any deal was in progress.

- Treasury Yields Hold Steady as Powell Maintains Caution: US Treasury yields were little changed on Wednesday as investors digested Federal Reserve Chair continued cautious tone. The 10-year yield was nearly flat at 4.289%, while the 2-year yield edged down to 3.775%. Powell told lawmakers that the Fed would hold off on rate adjustments while it gauges the impact of tariffs on prices, keeping markets in wait-and-see mode amid stable economic data.

- New Home Sales Drop Sharply as Mortgage Rates Stay Elevated: US new home sales fell 13.7% in May to a seasonally adjusted annualised rate of 623,000 units, marking the slowest pace since October 2024. The figure was 6.3% below the same month last year and missed expectations by a wide margin. The sharp decline, driven by persistently high mortgage rates near 7%, pushed housing supply to a three-year high, raising concerns about demand sustainability in the sector.

FX Today:

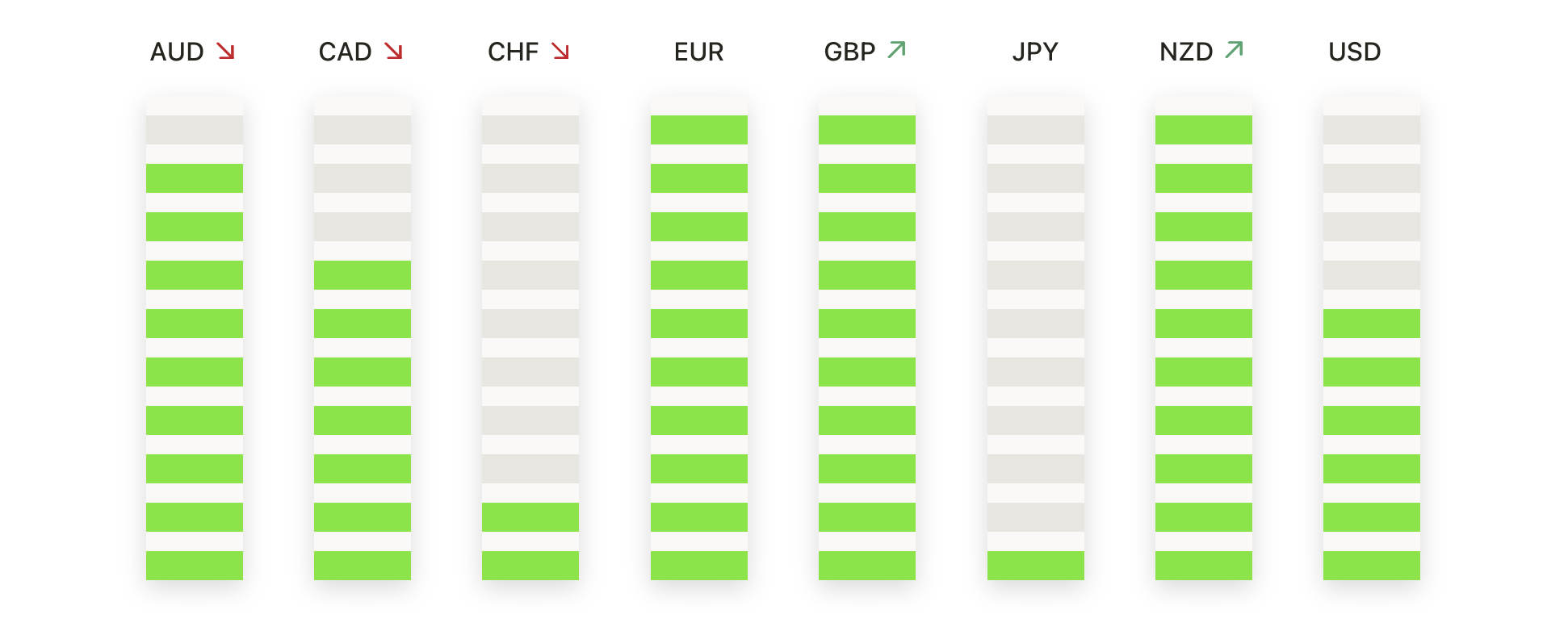

- EUR/USD Holds Firm as Bullish Momentum Builds: The EUR/USD pair finished Wednesday at 1.1658, advancing 0.42% after ranging between 1.1589 and 1.1669. The euro continued to gain ground for a fifth straight session, closing near its intraday high as upward momentum remained intact. The pair is now well above its 50-day SMA at 1.1376, with all key moving averages aligned to support further appreciation. Market focus is shifting to the 1.1700 level, which could act as short-term resistance, followed by the March 2024 high near 1.1800. On the downside, support is seen at 1.1500, and any drop below this level may prompt a deeper correction.

- GBP/USD Surges to Fresh Yearly High on Breakout Move: GBP/USD closed the session at 1.3665, climbing 0.36% after rising from 1.3591 to a peak of 1.3671. The price remains comfortably above the 50-day SMA, which has now crossed both the 100-day and 200-day averages in a bullish sequence. Immediate upside resistance is located at 1.3800, while former resistance at 1.3500 has turned into solid support. The short-term structure stays constructive, and unless the pair slips back below the 50-day average, further gains remain likely.

- USD/JPY Struggles to Overcome Stubborn Resistance Near 146.00: USD/JPY settled at 145.24, gaining 0.24% after moving between 144.60 and 145.94 during the session. The pair marked its third straight daily rise but again failed to close above the resistance zone near 146.00, with a long upper wick hinting at intraday rejection. The 100-day SMA at 146.60 continues to act as a ceiling, while the 50-day SMA has begun to slope upward from below, keeping the broader trend in a neutral stance. A decisive break above 147.00 would shift bias back to the upside, though repeated failures at current levels suggest a possible pullback toward initial support at 143.00 if bulls lose control.

- NZD/USD Extends Rebound as Key Resistance Approaches: NZD/USD finished the day at 0.6037, rising 0.51% after bouncing from a low of 0.6005 and hitting a high of 0.6043. The New Zealand dollar posted a solid bullish candle, regaining ground lost in the prior session and closing firmly above the 50-day and 100-day SMAs. Price is now consolidating just beneath the April swing high at 0.6100, a level that may trigger profit-taking if retested. The 50- and 100-day averages have both moved above the 200-day SMA, confirming a bullish alignment. Support is now seen at 0.5950, and as long as price stays above this zone, further upside is likely.

- AUD/USD Climbs After Softer Inflation Eases Policy Pressure: The AUD/USD pair closed at 0.6510 on Wednesday, gaining 0.32% after bouncing from a low of 0.6484 and reaching a high of 0.6519. The Australian dollar extended its recovery for a second day as investors responded to the latest inflation data, which showed the monthly CPI slowed to 2.1% in May, the lowest level since October 2024. The Australian dollar posted a second straight gain, reversing Monday’s sharp decline and closing above the 50-day SMA. Buyers held control throughout the session despite some resistance near the 0.6520 area. The pair remains in a gradual recovery phase, but the 200-day SMA around 0.6550 continues to limit upward progress. A confirmed daily close above this zone would open the path for a more sustained rally, while support is at 0.6420.

- Gold Edges Higher as Buyers Defend the 50-Day Average: Gold ended the session at $3,334 on Wednesday, up 0.31% after moving between $3,312 and $3,337. The metal posted a modest recovery, bouncing off its 50-day SMA near $3,320 and settling above that key support for another session. The structure remains technically strong, with price also holding well above the 100-day and 200-day SMAs in a sustained uptrend. Resistance remains firm around $3,400, where bulls have repeatedly failed to break higher, while downside protection lies in the $3,280 to $3,300 range. As long as price remains supported above $3,300, the outlook stays bullish within an extended period of consolidation.

Market Movers:

- AeroVironment Jumps on Strong Earnings and Outlook: Shares of AeroVironment surged 21.6% after the company reported adjusted earnings of $1.61 per share on revenue of $275.1 million, both topping estimates.

- Bumble Soars After Workforce Reduction Plan: Bumble surged 25% as it announced a 30% staff cut expected to save $40 million annually.

- SiTime Declines After Announcing Share Offering: SiTime dropped 15.7% after unveiling plans for a $350 million common stock offering.

- BlackBerry Gains on Earnings Beat and Raised Outlook: BlackBerry advanced 12% as first-quarter results exceeded estimates and the company raised full-year guidance.

- FedEx Drops as Guidance Disappoints Investors: FedEx lost 3.3% after forecasting earnings below analyst estimates for the current quarter. Although Q4 results beat expectations, forward outlook weighed on sentiment.

- Flagstar Falls on New York Political Risk: Flagstar fell nearly 4% amid concerns tied to Zohran Mamdani’s likely victory in the NYC mayoral primary. The bank has heavy exposure to rent-regulated housing loans.

- QuantumScape Soars on Battery Technology Update: QuantumScape jumped over 30% after announcing a production advance involving its Cobra separator.

Markets remained steady on Wednesday, supported by strength in technology shares and a rebound in oil prices, while investors assessed the impact of easing inflation, soft housing data, and geopolitical developments. The S&P 500 hovered just below record territory, with Nvidia’s rally helping offset broader concerns over growth and trade. A fragile Middle East ceasefire continued to hold, calming earlier volatility, while Federal Reserve Chair Powell maintained a measured tone on rates. As attention turns to upcoming inflation readings and global economic signals, traders appear willing to stay engaged, with AI enthusiasm and macro stability keeping sentiment broadly constructive.