US equities rallied on Wednesday after the Federal Reserve cut interest rates by 25 bp, marking its third consecutive reduction and bringing the federal funds rate to a range of 3.5% to 3.75%. The move strengthened expectations that policy is now shifting more decisively toward supporting growth, lifting sentiment across the market. The Dow led the advance as investors also welcomed the Fed’s decision to resume short-term bond purchases, which added further liquidity support. The S&P 500 briefly pushed above its previous record closing level before easing back, while the Nasdaq posted a steadier rise as traders absorbed Powell’s reassurance that further tightening is no longer a realistic outcome. With financial conditions improving and confidence rebuilding, talk of a potential “Santa Claus rally” gained momentum heading into the final stretch of the year.

Key Takeaways:

- Dow Jumps After Fed Delivers Third Straight Cut: The Dow surged 497.46 points to 48,057.75 as traders welcomed the Fed’s rate move and bet on further easing in 2026. The Fed’s messaging was seen as supportive for risk assets, boosting sentiment into year-end.

- S&P 500 Briefly Breaks Record Close: The S&P 500 added 0.7% to finish at 6,886.68 after briefly surpassing its previous record closing high of 6,890.89. Strong growth forecasts and renewed liquidity support helped justify elevated equity valuations.

- Nasdaq Edges Higher on Mixed Tech Reaction: The Nasdaq rose 0.3% to 23,654.16, lagging the broader market as traders assessed the Fed’s stance on growth and inflation alongside sector-specific earnings headwinds.

- Russell 2000 Hits Fresh All-Time High: Small-caps outperformed as easing expectations boosted rate-sensitive names. The Russell 2000 climbed as much as 1.5% intraday and is on track for a record close above 2,531.16, bringing its year-to-date gain to roughly 14.9%, still behind the S&P 500’s approximately 17.2% advance.

- European Markets End Mixed as Fed Decision Looms: The Stoxx 600 finished broadly flat, up 0.07%, while major regional indexes diverged with the FTSE 100 up 0.14%, Germany’s DAX down 0.13%, and France’s CAC 40 sliding 0.37%. Italian equities also weakened, with the FTSE MIB down 0.2%. Investors weighed weaker prospects for further ECB cuts, with German and French yields rising to multi-month highs on increased fiscal borrowing. Corporate headlines added to the split tone, including a 1.2% fall for Anglo American as it progresses a merger with Teck Resources, a strike call at LVMH’s champagne units, and a sharp rally in Delivery Hero after the group announced strategic reviews.

- Asia-Pacific Trade Mixed as China Inflation Ticks Higher: Sentiment was divided across the region as investors balanced improving consumer price data in China with ongoing deflation risks in manufacturing and near-term uncertainty around Fed policy. Hong Kong’s Hang Seng gained 0.22%, while the CSI 300 dipped 0.14% as producer prices fell 2.2% year-on-year, extending a four-year deflation stretch. The Nikkei 225 slipped 0.1% but the Topix rose 0.12%, with bond yields hitting their highest since 2007 after Bank of Japan comments fuelled expectations of a rate hike next week. Australia’s ASX 200 was flat as local yields broke above 4.8% for the first time since late 2023. South Korea’s Kospi fell 0.21% while the Kosdaq climbed 0.39%, and New Zealand’s NZX-50 dropped 0.62% to a three-week low.

- Oil Prices Rise on US Tanker Seizure Near Venezuela: Brent crude increased 1.13% to $62.64 and WTI gained 1.20% to $58.95 after US officials confirmed the seizure of an oil tanker, intensifying short-term supply concerns in an already sensitive market.

- Yields Fall as Fed Expands Balance Sheet: Treasury yields eased following the rate cut to a 3.5%–3.75% range. The 10-year yield slipped to 4.143%, the 30-year eased to 4.791%, and the 2-year fell to 3.534% as renewed bond-buying supported liquidity.

FX Today:

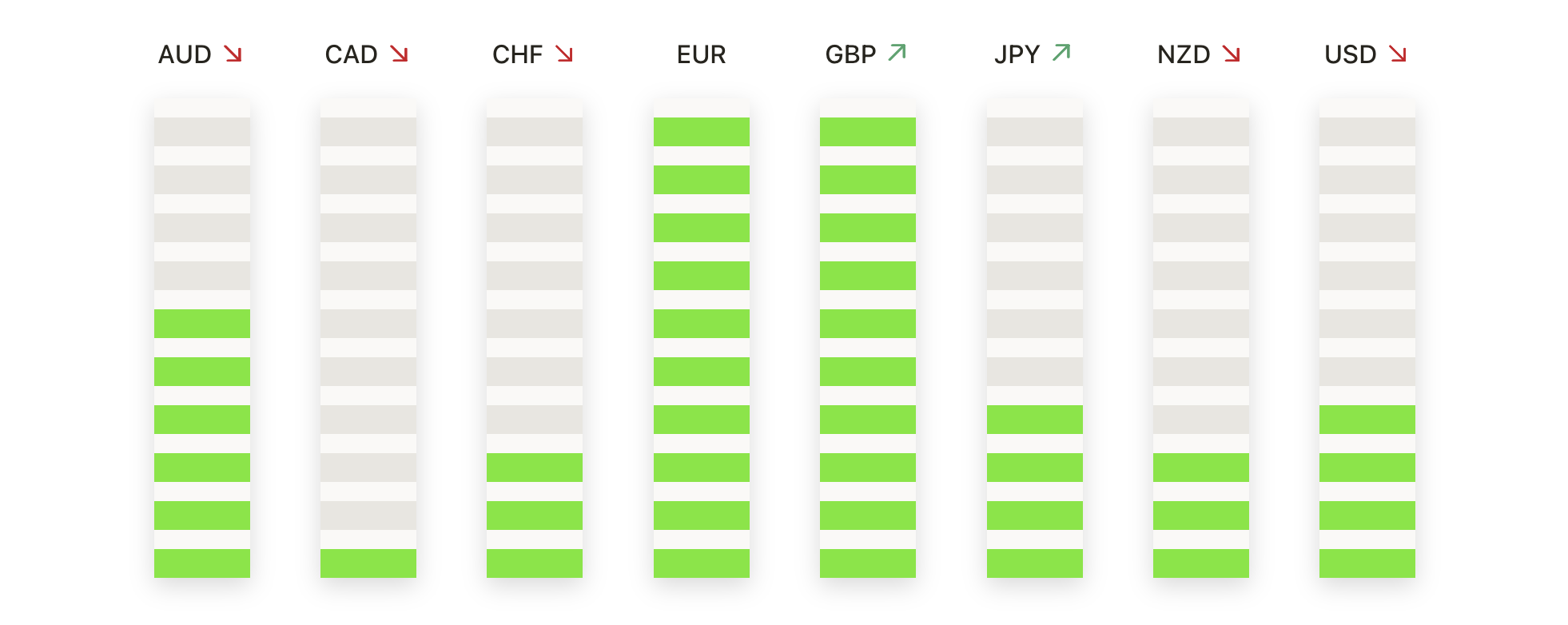

- EUR/USD Breaks Higher as Bullish Momentum Builds: EUR/USD climbed 0.55% to close at 1.1693, extending its rally after a strong session high of 1.1699 and a low of 1.1622. The pair delivered a decisive bullish candle, lifting firmly above the 50-day SMA at 1.1606, the 100-day SMA at 1.1642 and the 200-day SMA at 1.1478. Price has now cleared resistance that previously capped rallies in late October and early November, turning those former barriers into support as the advance gains traction. With buyers in control, focus is now on the early-October swing high around 1.1900 as the next major upside target. Initial support sits at the 100-day SMA at 1.1642, with the 50-day SMA at 1.1606 providing a deeper buffer if profit-taking emerges.

- GBP/USD Sustains Uptrend Above Key Support Levels: GBP/USD gained 0.65% to finish at 1.3385 after trading between 1.3389 and 1.3298, posting a strong bullish close near its high. Price remains above the 50-day SMA at 1.3260, while the 100-day SMA at 1.3362 and the 200-day SMA at 1.3337 now act as nearby support as the recovery extends. The pair has broken above the 200-day SMA with conviction and is testing resistance around the 100-day SMA, signalling strengthening bullish control after a reversal that began in late November. Immediate resistance is identified at 1.3396, with scope for continuation toward the October swing high near 1.3700 if buying momentum persists. Initial support lies at 1.3298 and then at 1.3260.

- USD/JPY Pulls Back as Momentum Moderates After Recent Highs: USD/JPY slipped 0.57% to close at 155.91 after reaching a high of 156.81 and a low of 155.79, forming a bearish engulfing pattern as profit-taking emerged at the upper end of the trend. The overall structure remains firmly bullish, with price trading well above rising moving averages. The 50-day SMA is at 153.70, the 100-day at 150.74 and the 200-day at 148.21, confirming strong underlying momentum. Resistance remains at 156.81, with the next upside objective near 158.00 if buyers regain traction. Initial support rests at 155.79, followed by the 50-day SMA at 153.70 which has repeatedly acted as dynamic support.

- AUD/USD Extends Rally Toward Multi-Month Highs: AUD/USD advanced 0.58% to settle at 0.6679 after trading between a high of 0.6686 and a low of 0.6641, continuing a strong upward phase that has lifted the pair cleanly above all major moving averages. The 50-day SMA at 0.6536, the 100-day at 0.6538 and the 200-day at 0.6476 are all now acting as firm support as buyers maintain control. With price approaching the September swing high around 0.6700, a breakout above that threshold would open a path toward 0.6800. Initial support lies at 0.6641 and then the 50-day SMA at 0.6536 if a pullback develops.

- Gold Consolidates Near Peak Levels as Buyers Remain in Control: Gold rose 0.56% to close at $4230 after testing a high of $4238 and a low of $4182, marking another bullish session near the top of its recent range. Price remains well above its moving averages. The 50-day SMA stands at $4091, the 100-day at $3792 and the 200-day at $3505, reinforcing a powerful long-term trend. Resistance is positioned near the recent high around $4380, with traders watching whether price can hold above the $4250 area to unlock further upside. Initial support sits at $4182, followed by $4091 if consolidation deepens.

- Silver Jumps to Fresh Highs as Rally Strengthens: Silver jumped 1.77% to close at $61.77 after trading between $61.95 and $60.01, with a strong candle finish near the session high signalling persistent buying pressure. The metal remains substantially above all major moving averages. The 50-day SMA is at $51.38, the 100-day at $45.75 and the 200-day at $39.88, highlighting the strength of the uptrend. With price in new high territory, the next potential upside markers are psychological barriers such as $62.00 and $65.00, given the lack of visible resistance. Initial support is seen at $60.01 and then around $56.00 if profit-taking develops.

Market Movers:

- Photronics Soars on Strong Results: Shares surged more than 45% after the company reported better-than-expected fourth-quarter earnings and issued first-quarter guidance that also topped forecasts.

- Dave & Buster’s Jumps Despite Earnings Miss: Shares climbed 13% after adjusted EBITDA exceeded expectations, even though the entertainment operator missed forecasts on both revenue and profit.

- AeroVironment Declines After Profit Miss: The drone maker fell more than 12% after reporting fiscal second-quarter earnings of 44 cents per share, below estimates of 78 cents from LSEG.

- GE Vernova Gains on Upbeat Outlook: Shares advanced 15% after management signalled revenue for 2025 tracking toward the high end of guidance.

- Oracle Slides Following Revenue Shortfall: Shares dropped 6% after quarterly revenue grew 14% year on year but fell short of expectations. Net income rose to $6.14 billion, or $2.14 per share, from $3.151 billion a year earlier.

- EchoStar Rallies on Analyst Upgrade: The stock rose 11% after Morgan Stanley upgraded it to overweight, citing favourable positioning amid rising competition in US wireless markets.

The Fed’s latest decision has helped remove a key source of uncertainty, allowing markets to refocus on the prospects for growth heading into 2026. With policymakers signalling they are now more alert to economic softness than inflation risks, investors are increasingly treating lower rates and renewed liquidity support as foundations for further equity strength. The rally in smaller companies and rate-sensitive areas of the market suggests confidence is broadening beyond the large-cap benchmarks. While future moves will depend on data and global conditions, the tone across trading desks has shifted toward opportunity rather than caution, raising hopes that positive momentum can carry through the final stretch of the year.