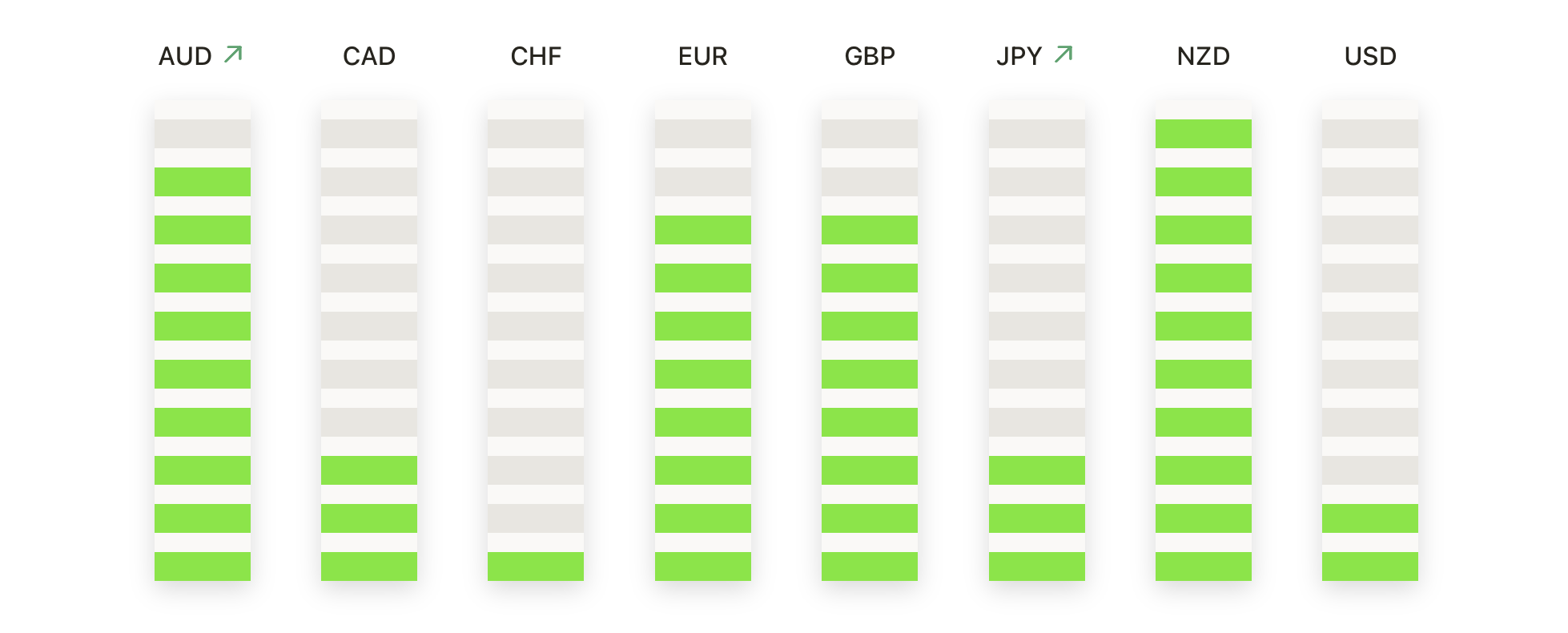

The Dow advanced on Wednesday as Wall Street digested robust corporate earnings alongside rising expectations for interest-rate cuts, even as political tensions in Washington remained in focus. The blue-chip index gained 147 points, while the S&P 500 edged to a fresh record close and the Nasdaq also moved higher. Nvidia reported results after the market closed that comfortably beat estimates, but the muted after-hours reaction highlighted investor caution over whether enthusiasm for artificial intelligence can continue to boost equities. Overall sentiment remained constructive, supported by resilient earnings and easing inflation, with traders awaiting further economic data later in the week.

Key Takeaways:

- Dow Rises on Optimism Over Rate Cuts and Earnings: The Dow Jones Industrial Average gained 147.16 points, or 0.32%, to close at 45,565.23, supported by strength in select retail and technology names.

- S&P 500 Ends at Fresh Record Before Nvidia Earnings: The S&P 500 added 0.24% to settle at 6,481.40, setting a new closing high before Nvidia’s after-hours results, with earnings and revenue above estimates as data centre revenue surges 56%.

- Nasdaq Edges Higher as Tech Stocks Trade Mixed: The Nasdaq Composite rose 0.21% to finish at 21,590.14, with moves across the technology sector uneven. Despite the late-session rebound, the broader index remains sensitive to swings in heavyweight AI.

- Europe Markets Mixed as Inflation and Politics Weigh: European equities ended with a mixed performance, as the Stoxx 600 gained 0.1% for its strongest monthly gain since May, while country indices diverged. France’s CAC 40 rebounded 0.44% after sharp losses a day earlier, though concerns persisted over Prime Minister Francois Bayrou’s ability to pass a 2026 budget. The FTSE 100 dipped 0.11% to 9,255.50, still marking its fifth-highest close in history, while Italy’s FTSE MIB fell 0.82% and Germany’s DAX slipped 0.44% to 24,046.21. UK producer output prices rose 1.9% in June, a two-year high, while CPI stood at 3.8% in July, the highest among major economies, adding to pressure on the Bank of England. Meanwhile, German consumer confidence is expected to fall for a third month in September, with fears of job losses and inflation clouding sentiment. UK retail sales also recorded their eleventh consecutive monthly decline in August, though the CBI survey showed an improved outlook for September.

- Asia Markets Close Mixed as China Data and Tariffs Shape Trade: Asia-Pacific equities ended with a split performance as investors digested Chinese industrial data, fresh US tariffs, and inflation surprises in Australia. China’s industrial profits fell 1.5% year-on-year in July, marking a recovery after months of steeper declines, though equities weakened as the CSI 300 slid 1.49% to 4,386.13 and Hong Kong’s Hang Seng lost 1.32%. Economists at Nomura warned of “irrational exuberance” after recent gains. In India, secondary US tariffs of 25% on exports took effect, lifting overall duties to 50%, though domestic markets were closed for a holiday. Japan’s Nikkei 225 gained 0.3% to 42,520.27, led by a more than 20% surge in Nikon, while the broader Topix ended flat at 3,069.74. South Korea’s Kospi added 0.25% to 3,187.16 but a Reuters poll suggested August export growth slowed to 3.0% from 5.8% in July after new US tariffs, with the Kosdaq little changed at 801.72. Australia’s ASX 200 advanced 0.28% to 8,960.5 as July’s inflation data sharply overshot expectations, with CPI accelerating to 2.8% year-on-year from 1.9%.

- Oil Prices Rebound on Inventory Draw and Tariff Impact: Brent crude rose 1.23% to settle at $68.05 a barrel, while WTI gained 1.42% to $64.15, recovering from steep losses in the previous session. Prices were lifted by a 2.4 million barrel draw in US crude inventories and concerns over the impact of new US tariffs on Indian shipments, even as Russia raised export plans following disruptions at domestic refineries.

- Treasury Yields Ease After Trump Fed Dispute: US Treasury yields fell from session highs as traders weighed political tensions around the Federal Reserve. The 10-year yield fell more than 2 basis points to 4.234% after earlier topping 4.27%, while the 30-year held near 4.91%. The 2-year yield slipped 6 basis points to 3.617%, leaving the curve at its widest spread since April. Investors are now looking ahead to GDP data and pending home sales for further direction.

FX Today:

- EUR/USD Struggles for Breakout as Sellers Cap 1.1650: EUR/USD closed at 1.1635, down 0.07% after trading between 1.1574 and 1.1648. The pair remains contained under the 50-day SMA at 1.1655, where sellers continue to block upside traction, even as broader recovery is anchored by the 100-day and 200-day averages at 1.1504 and 1.1024. The euro is still forming higher lows since early August, signalling that buyers are maintaining control despite fading momentum near the upper 1.1600s. A sustained move above 1.1700 would confirm bullish continuation, while a close under 1.1600 and 1.1550 would risk exposing the downside back toward 1.1450.

- GBP/USD Extends Climb as Buyers Defend Moving Averages: GBP/USD settled at 1.3499, up 0.16% after ranging between 1.3417 and 1.3502. The daily close produced a modest green candle showing resilience, with price holding above the 50-day SMA at 1.3495 and the 100-day SMA at 1.3437. The pair has higher lows from late July’s 1.3100 base, reinforcing a constructive trend despite repeated failures near 1.3600. Support remains firm at 1.3450–1.3430.

- USD/JPY Remains Range-Bound as 200-Day SMA Caps Upside: USD/JPY closed at 147.46, up 0.10% after trading between 147.29 and 148.19. The small-bodied candle highlights muted momentum, with the pair still supported above the 50-day SMA at 146.93 and the 100-day SMA at 145.46. Price action since mid-July has carved a tight consolidation between 147.00 support and the 149.50–150.00 resistance zone, reflecting indecision but also showing buyers defending dips. The broader context remains cautiously constructive, though the inability to clear the 200-day SMA at 148.97 caps conviction. A close above that level would reassert bullish control and open the path back to 150.00, while a drop beneath 146.90 would turn focus to 145.50.

- USD/CAD Retreats From Highs as Sellers Regain Momentum: USD/CAD finished at 1.3786, down 0.38% after a session between 1.3783 and 1.3838. The red daily candle marked renewed pressure as the pair pulled back from recent highs, slipping back under the 200-day SMA at 1.4027 while still holding above the 50-day and 100-day averages at 1.3731 and 1.3770. Structurally, the recovery from early July lows near 1.3600 has faltered below the 1.3900 ceiling, leaving a lower high relative to May’s peaks and signalling hesitation in the broader trend.

- Gold Consolidates Beneath $3,400 as Bulls Eye Breakout: Gold settled at $3,396, posting a 0.10% gain after ranging between $3,374 and $3,399. The session produced a small-bodied green candle that reflected ongoing consolidation beneath resistance, with price holding comfortably above the 50-day SMA at $3,348 and well clear of the 100-day and 200-day averages at $3,317 and $3,052. Structurally, the metal has built a higher-low formation since mid-August, reinforcing buyer control and keeping the broader uptrend intact. Attention now turns to the $3,400–$3,420 zone, where repeated highs have capped momentum. A decisive break above this ceiling would expose the July peak near $3,450, while failure to sustain gains risks a pullback towards $3,360 and $3,340, where the 50-day average provides initial support.

Market Movers:

- MongoDB Soars on Strong Results and Upgraded Outlook: MongoDB surged more than 38% after reporting Q2 adjusted EPS of $1.08, beating consensus of 65 cents, and raising its 2026 EPS forecast well above expectations.

- Kohl’s Jumps on Earnings Surprise and Guidance Boost: Kohl’s rallied more than 23% after delivering Q2 EPS of $1.35 against forecasts of 31 cents, while issuing stronger full-year guidance of 50–80 cents versus 49 cents expected. The report drove renewed interest in the retail sector.

- nCino Rallies After Revenue Beat and Raised Forecasts: nCino climbed over 13% as Q2 subscription revenue reached $130.8 million, exceeding estimates, and management lifted its 2026 revenue guidance above consensus. The upbeat tone reinforced demand for fintech names.

- American Eagle Outfitters Gains on Travis Kelce Collaboration: American Eagle rose more than 8% after unveiling its AE x Tru Kolors clothing line with NFL star Travis Kelce, a move designed to tap into Taylor Swift-related brand momentum.

- Elanco Animal Health Advances on Index Inclusion: Elanco Animal Health gained more than 3% after S&P Dow Jones Indices said the stock will join the S&P MidCap 400 on 2 September, replacing Sarepta Therapeutics.

- Dynatrace Climbs on Oppenheimer Upgrade: Dynatrace added more than 3% after Oppenheimer initiated coverage with an outperform rating and $65 price target, citing strong demand for cloud observability.

- J M Smucker Declines After Sales Miss: J M Smucker slipped over 4% as Q1 net sales of $2.11 billion came in just below expectations of $2.12 billion, raising concerns over slowing consumer demand.

The Dow led Wall Street higher on Wednesday as investors weighed political tensions with the Federal Reserve against optimism over earnings and policy easing. Nvidia’s stronger-than-expected results underscored the ongoing strength of demand for artificial intelligence infrastructure, but the lacklustre after-hours reaction highlighted caution over whether momentum can extend further. With key economic data due in the coming days, markets remain focused on whether the rally can sustain its pace into September.