Momentum carried through US markets on Wednesday as investors leaned back into risk, extending the rebound sparked in the previous session. Strength in large-cap technology once again set the tone, with enthusiasm around artificial intelligence leaders helping to steady sentiment after recent volatility. Nvidia’s continued rally and renewed interest in software names reinforced the view that last week’s AI-driven sell-off may have gone too far. At the same time, political and geopolitical headlines remained in the background, with tariffs and Middle East tensions watched but failing to derail the broader recovery. The result was a confident session that signalled growing willingness among investors to selectively re-engage rather than retreat.

Key Takeaways:

- S&P 500 Gains Ground on Tech Strength: The S&P 500 climbed 55.81 points, or 0.81%, to finish at 6,946.13. The index was supported by a strong performance in the software sector and continued momentum in semiconductor giants, as investors re-evaluated the risk-reward profile of major technology players.

- Dow Jones Advances as Blue-Chip Sentiment Improves: The Dow Jones Industrial Average advanced 307.65 points, or 0.63%, to settle at 49,482.15. Gains were broad-based as market sentiment was lifted by a more moderate tariff implementation and positive economic rhetoric from the latest State of the Union address.

- Nasdaq Composite Outperforms amid Software Rebound: The Nasdaq Composite surged 288.01 points, or 1.26%, to end the session at 23,152.08. Outperformance was driven by a relief rally in AI-focused firms and software stocks, further bolstered by Nvidia’s strong post-market earnings and news of Anthropic’s new AI tool integrations.

- European Markets Rise as Tariff Fears Moderate: European equity markets finished the session in positive territory as investor anxiety over global trade tensions eased. The pan-European Stoxx 600 index climbed 0.7%, while the FTSE 100 in London gained 1.09% to close at 10,797. Sentiment was bolstered by the implementation of a 10% universal US tariff, which was notably lower than the 15% rate previously threatened. On the economic front, Eurostat confirmed that Eurozone inflation fell to a 16-month low of 1.7% in January, providing some relief regarding the regional cost-of-living crisis. However, the outlook remained clouded by a surprise decline in German consumer sentiment to -24.7 for March and a modest 0.2% GDP growth for 2025. Corporate performance was also a drag, with Diageo shares tumbling 12.7% after the spirits maker cut its sales forecast, and Aston Martin announcing significant job cuts due to the impact of international trade duties.

- Asian Indices Reach Record Highs following Tech Rally: Asian markets experienced a historic session, with several major indices reaching all-time highs following a technology-led recovery on Wall Street. Japan’s Nikkei 225 surged over 2% to a record 58,583.12, while South Korea’s Kospi breached the significant 6,000-point milestone for the first time, closing at 6,083.86. In Australia, the S&P/ASX 200 rose 1.17% to 9,128.3, despite annual inflation data coming in slightly higher than expected at 3.8%. Chinese markets also participated in the upside, with the Hang Seng and CSI 300 posting gains of 0.45% and 0.6% respectively. Taiwan’s benchmark continued its remarkable run, securing a record high for the fifth consecutive day, as the region’s tech-heavy indices capitalised on the dissipation of AI-related industry disruption fears.

- Oil Holds Steady as Inventory Surge Offsets Supply Risks: Oil prices were little changed as a much larger-than-expected US crude stock build outweighed supply concerns tied to US–Iran tensions. Brent settled up 0.25% at $70.95 a barrel, while WTI ended at $65.49 after a decline on the day. US crude inventories rose by 16 million barrels last week versus expectations for a 1.5-million-barrel increase, while the EIA adjustment factor hit a record 2.7 million barrels per day, limiting price upside despite the broader geopolitical backdrop.

- Treasury Yields Edge Higher After Trump Speech and Weak Auction Demand: US Treasury yields drifted higher as investors assessed President Donald Trump’s State of the Union address and digested fresh supply. The 10-year yield rose to 4.05%, the 30-year yield edged up to 4.694%, and the 2-year yield climbed to 3.471%. A $70 billion five-year note auction drew low demand, with the bid-to-cover ratio marking its weakest level since July, adding to the upward pressure at the margin.

FX Today:

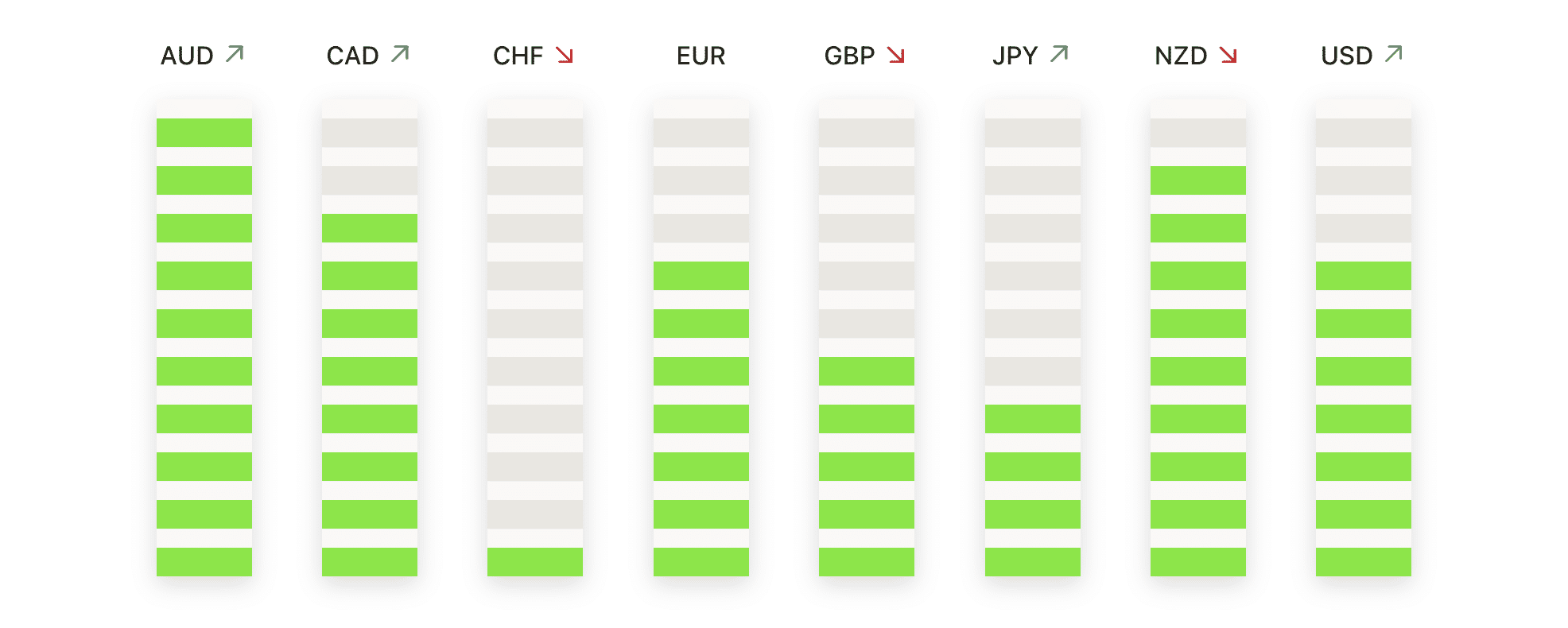

- EUR/USD Recovers Towards Recent Highs: EUR/USD rose 0.28% to close at 1.1805 after trading between 1.1771 and 1.1814, ending the session near the high as buying interest re-emerged. The pair remains comfortably above the 50-day SMA at 1.1774 and well above the 100-day and 200-day SMAs at 1.1690 and 1.1656, keeping the broader technical bias constructive. Price action suggests the pair is recovering toward the upper boundary of its recent consolidation range following a brief pause. Resistance is located at 1.1814 and then the psychological 1.1900 level, while support is seen at 1.1771 and the 50-day moving average. Holding above these levels would keep the near-term outlook tilted higher.

- GBP/USD Rebounds Above Key Moving Averages: Sterling advanced 0.46% to close at 1.3552, with the pair trading between 1.3488 and 1.3556 and finishing close to its daily peak. The rebound pushed GBP/USD back above the 50-day SMA at 1.3535, while the 100-day and 200-day SMAs at 1.3394 and 1.3446 continue to slope higher beneath price. The move indicates renewed buying interest after a short-lived pullback within a well-defined uptrend. Immediate resistance sits at 1.3556, followed by the recent highs in the 1.3850–1.3870 region, while initial support is found at 1.3488 and then 1.3446.

- AUD/USD Resumes Upside Momentum: AUD/USD surged 0.88% to close at 0.7120 after trading between 0.7056 and 0.7124, breaking out of a short-term consolidation phase. The pair is trading well above its 50-day, 100-day and 200-day SMAs at 0.6858, 0.6697 and 0.6611, reinforcing the strength of the prevailing uptrend. The close near the session high suggests bullish momentum has reasserted itself. Resistance is located at 0.7124 and then near 0.7150, while support lies at 0.7056 and the 0.7000 area.

- USD/JPY Reclaims Bullish Trajectory near Recent Highs: USD/JPY rose 0.35% to close at 156.44, rebounding from an intraday low of 155.34 as buyers re-entered the market. The pair remains firmly supported by the 50-day SMA at 155.95 and the 100-day SMA at 155.05, indicating that the broader bullish trend is still dominant. Price action suggests a resurgence of interest following a brief corrective phase, with the pair now eyeing the recent swing high of 156.82. Resistance is noted at 156.82, while support is anchored at 155.34. Maintaining a position above 156.00 is critical for a challenge of the 158.00 level, while a breach of the 155.34 support could signal a shift toward a more neutral short-term bias.

- Gold Trades Higher After Consolidation: Gold edged up 0.16% to close at $5,150 after trading between $5,121 and $5,218. The metal continues to hold well above its 50-day, 100-day and 200-day SMAs at $4,738, $4,419 and $3,917, confirming the strength of the longer-term uptrend. Recent price action points to consolidation following a sharp rally, with buyers still broadly in control. Resistance is located at $5,218 and then $5,400, while support is seen at $5,121 and the $5,000 psychological level.

- Silver Rebounds Strongly Towards Resistance: Silver climbed 1.48% to settle at $88.37 after trading between $86.61 and $91.30, staging a sharp recovery from recent lows. The metal remains firmly above its 50-day, 100-day and 200-day SMAs at $82.28, $69.99 and $52.44, keeping the broader structure bullish. The long upper wick suggests some profit-taking near resistance, though momentum remains constructive. Resistance is seen at $91.30 and the $100.00–$104.00 zone, while support is located at $86.61 and the 50-day moving average.

Market Movers:

- Coinbase Surges After Expanding Into Stock Trading: Shares jumped 12% after the cryptocurrency exchange launched stock trading on its platform. The move is part of a broader strategy to position Coinbase as a multi-asset venue for stocks, ETFs and prediction markets.

- Clear Secure Soars on Earnings And Guidance Beat: The biometric identity platform surged 39% after fourth-quarter adjusted EPS, revenue and adjusted EBITDA all topped expectations. Strong first-quarter revenue guidance added to the upside momentum.

- Cava Group Rallies on Strong Sales Outlook: Shares climbed more than 26% after the company forecast full-year comparable restaurant sales growth of 3% to 5%. The outlook exceeded the 2.75% consensus estimate.

- Oddity Tech Plunges on Sharp Revenue Warning: Oddity Tech shares sank more than 49% after the company said first-quarter 2026 revenue is expected to fall 30% year-on-year. The guidance pointed to a sharp slowdown in growth.

- GoDaddy Slides After Soft Revenue Forecast: Shares dropped 14% after GoDaddy projected annual revenue of $5.195 billion to $5.275 billion, below estimates. The company cited slower AI-related adoption.

The midweek rally reinforced the market’s shift away from blanket caution and towards selective conviction, with technology once again setting the pace. Nvidia’s strength and renewed interest in software helped extend gains across US equities, while European and Asian markets followed through as tariff concerns eased and global risk sentiment improved. Although political headlines and geopolitical tensions remain in focus, investor behaviour suggests a growing willingness to look beyond near-term noise and focus on companies viewed as better positioned within the evolving AI landscape.