In a market atmosphere thick with anticipation, US stocks and Bitcoin navigate a landscape marked by the looming release of crucial inflation data. Wednesday’s trading session saw a subtle pullback in major US stock indices, where investors are eyeing the forthcoming personal consumption expenditure report with keen interest. Amidst a recalibration of expectations in the tech sector and potential overvaluation of AI technologies, Bitcoin’s notable surge to heights not seen since November 2021 introduces a new dimension to the market’s narrative. This contrast of traditional market anxieties with cryptocurrency’s bold strides captures a moment of crossroads for investor sentiment. As the US market teeters on the edge of economic data-driven shifts, the spotlight on Bitcoin’s performance highlights the evolving dialogue between traditional financial mechanisms and cryptocurrency, each waiting for signals that could redefine investment trajectories in a landscape with many uncertainties.

Key Takeaways:

- Marginal Downturn as Markets Anticipate Key Inflation Data: The Dow Jones Industrial Average edged lower by 41 points, a decrease of 0.1%, marking its third consecutive day of losses amidst investor anticipation of crucial inflation insights. The S&P 500 and Nasdaq Composite also saw declines, pulling back 0.2% and 0.5% respectively, reflecting a cautious stance ahead of the Personal Consumption Expenditures (PCE) report.

- Record Highs Amidst Uncertainty: Despite the day’s overall downturn, nearly 60 companies within the S&P 500 index achieved new 52-week highs, showcasing areas of resilience and optimism. Notably, financial giants Wells Fargo and American Express, alongside discount retailers Ross Stores and TJX Companies, and home improvement leaders Home Depot and Lowe’s, stood out for their performance.

- Global Markets Echo Cautious Sentiment: European stocks closed lower, with the Stoxx 600 index falling 0.3%, led by a 1.4% decline in tech stocks, while Asia-Pacific markets mostly ended in the red, signalling a cautious global outlook. The Hang Seng index in Hong Kong notably declined by 1.3% following policy announcements aimed at stimulating the real estate sector.

- Economic Indicators Under Microscope: The U.S. economy’s growth for the fourth quarter was slightly revised down to a 3.2% annualized rate, from the previously reported 3.3%, indicating a slow but steady economic expansion. Meanwhile, mortgage application volumes fell by 5.6%, reflecting the impact of persistently high interest rates on the housing market.

- Oil Markets Show Mixed Signals: Crude oil futures were mixed, with West Texas Intermediate dropping 0.42% to $78.54 a barrel, while Brent futures edged up slightly by 0.04% to $83.68.

- Apple Embraces Generative AI: Apple’s announcement of significant investments in generative AI underscores its leadership in innovation and shapes market expectations. This strategic move signals the company’s commitment to defining the future of technology, potentially impacting its product ecosystem and investor sentiment amidst broader economic and sectoral shifts.

- Corporate Movements and Forecasts: Snowflake’s announcement of CEO Frank Slootman’s retirement led to a 20% plunge in its stock price, while Salesforce’s forecast of single-digit full-year revenue growth caused its shares to slide up to 6% in extended trading, highlighting the varied corporate landscape amidst economic uncertainties.

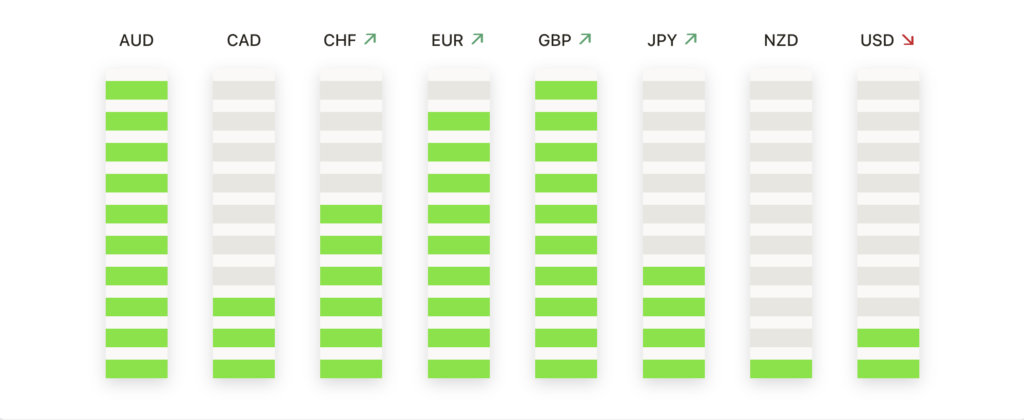

FX Today:

- EUR/USD Faces Downward Pressure Amidst PCE Anticipation: The EUR/USD pair fluctuated, reaching a low of 1.0796 as markets braced for the forthcoming PCE inflation data. The pair struggled to find direction, reflecting investors’ recalibrated expectations for Federal Reserve rate adjustments, eventually hovering around the 1.0800 mark.

- GBP/USD Tests Key Support Levels Amid Economic Speculation: The GBP/USD currency pair saw resistance, ultimately challenging support levels near 1.2600 after dipping below the 50-day simple moving average. This movement highlighted the increased scrutiny by investors over UK economic indicators, with the pair closing below the crucial 1.2675 mark, suggesting potential further declines towards the 200-day simple moving average around 1.2570.

- EUR/GBP Seeks Recovery Within Bearish Trend: In its prolonged downtrend, the EUR/GBP pair aimed for a recovery, targeting the resistance at 0.8575. Despite modest gains against the pound, the pair’s trajectory remains constrained by significant resistance levels and the broader bearish trend, reflecting the ongoing economic disparities between the Eurozone and the UK.

- USD/CAD Reaches Ten-Week High, Reflecting USD Strength: The USD/CAD pair ascended to a new ten-week high, momentarily surpassing the 1.3600 barrier to reach 1.3606 before retreating. Despite near-term congestion, USD/CAD has closed in the green for all but one of the last eight consecutive weeks, with the 200-day Simple Moving Average (SMA) at 1.3480.

- Gold Holds Steady Despite Economic Headwinds: Gold traded sideways, with XAU/USD struggling to break above the $2,035 resistance level. Despite failing to surpass this threshold for the 12th consecutive day, the precious metal maintained its upward bias. If buyers can reclaim the $2,035 level, gold may challenge the psychological $2,050 mark, with key resistance at the February high of $2,065.60 looming overhead.

- Bitcoin Surges to New Heights, Touching $64,000: Bitcoin continued its remarkable rally, briefly surpassing $63,000 for the first time since November 2021. The flagship cryptocurrency saw a 7% increase to $61,031.02, nearing its all-time high of $68,982.20. This week’s nearly 20% surge underscores the growing investor enthusiasm for Bitcoin, particularly as it approaches its next halving event, expected to trigger a major market rally.

Market Movers:

- Urban Outfitters Takes a Hit on Earnings Miss: Urban Outfitters (URBN) saw its shares plummet by 13.2% after the retailer reported fourth-quarter results that fell short of market expectations. The significant decline underscores the impact of consumer behaviour and economic uncertainties on the retail sector.

- DirectLine Surges on Takeover Speculation: Shares of British insurer DirectLine soared approximately 24% following confirmation from Belgium’s Ageas of a potential offer valued at £3.095 billion ($3.91 billion). The surge highlights the market’s responsiveness to M&A activities, with the proposed offer representing a premium of 42.8% over the closing price on the day prior to the announcement.

- Salesforce Projects Single-Digit Growth, Stock Declines: Salesforce (CRM) shares slid up to 6% in after-hours trading after the company projected single-digit revenue growth for the full year and announced the initiation of a dividend payment at 40 cents per share. The software giant’s light revenue forecast and dividend news contributed to the stock’s decline, reflecting investor concerns over growth prospects.

- Viatris Leads S&P 500 Decliners on Sales Miss: Viatris (VTRS) closed down more than 7%, leading the losers in the S&P 500 after reporting fourth-quarter net sales of $3.83 billion, missing the consensus estimate of $3.86 billion. The pharmaceutical company’s performance highlights the challenges faced by the sector in maintaining growth amidst competitive and regulatory pressures.

- Axon Enterprise Surges on Earnings Beat: Axon Enterprise (AXON) led the gainers in the S&P 500, with its shares jumping more than 13% after reporting fourth-quarter adjusted earnings per share of $1.12, surpassing the consensus estimate of 85 cents. The strong financial performance underscores the company’s robust growth trajectory and operational efficiency.

- Constellation Energy and eBay Post Notable Gains: Constellation Energy (CEG) and eBay (EBAY) both registered significant gains, with Constellation Energy up more than 9% after an upgrade by KeyBanc Capital Markets, and eBay climbing over 7% following better-than-expected fourth-quarter net revenue. These movements reflect the market’s positive reception to corporate strategies and financial results.

- Bumble Stumbles on Revenue Forecast: Bumble Inc. (BMBL) experienced a sharp decline, dropping over 14% after its fourth-quarter revenue of $273.6 million fell short of the consensus estimate of $275.6 million. The dating app company’s forecast for Q1 revenue also disappointed the market, projecting between $262 million to $268 million, below analyst expectations. The stock’s significant fall reflects investor concerns over the company’s growth trajectory amidst a competitive online dating landscape.

- Revolve Group Rallies on Analyst Upgrade: Revolve Group (RVLV) saw its stock soar more than 22% after an upgrade to ‘outperform’ from ‘market perform’ by Raymond James, with a new price target of $21. The fashion retailer’s shares responded positively to the bullish outlook, reflecting confidence in its ability to capture market share and drive revenue growth in the competitive online retail space.

- Flywire Surges on Strong Revenue Outlook: Payment solutions provider Flywire (FLYW) enjoyed an 18% increase in its stock price after projecting full-year revenue that significantly exceeded market expectations, indicating robust demand for its services. The company’s optimistic revenue forecast highlights its effective market penetration and the growing reliance on digital payment solutions across industries.

The narrative of anticipation for pivotal inflation data, the recalibration of growth expectations in the tech sector, and the ripple effects of corporate earnings across global markets have come to the forefront of the stock news. This week’s cautious trading behaviour underscores the delicate balance between optimism driven by potential and the practical realities of economic indicators. The upcoming inflation report remains a beacon for market direction, with its outcome likely to influence Federal Reserve policy decisions and the broader market sentiment. Meanwhile, the resilience of certain sectors and the agility of investors in responding to both challenges and opportunities highlight the dynamic and evolving landscape of the financial markets.