In a turnaround from previous trends, the stock market witnessed an impressive uplift, with the Dow Jones Industrial Average climbing over 400 points, lifted by a softer-than-anticipated April jobs report. This unexpected development has created investor hopes for potential interest rate cuts by the Federal Reserve, highlighting a shift in economic expectations. The S&P 500 and Nasdaq Composite also experienced significant gains, recording their best performances since February. This surge in optimism across major indices is reflective of a growing confidence in the strategic responses of monetary authorities to the prevailing economic indicators, setting a hopeful tone for market dynamics moving forward.

Key Takeaways:

- Dow Jones Industrial Average Makes Notable Gains: The Dow closed up by 450.02 points, a 1.18% increase, reaching 38,675.68. This uplift represents one of the most significant one-day gains for the index, underscoring a positive shift in investor sentiment.

- S&P 500 and Nasdaq Composite Surge: Both indices recorded impressive gains, with the S&P 500 rising by 1.26% to close at 5,127.79, and the Nasdaq Composite up by 1.99% to end at 16,156.33. These advances marked the indices’ best performances since February, driven by renewed optimism in the financial markets.

- European Markets Close Higher: The Stoxx 600 index rose by 0.44%, ending a week marked by strong earnings reports from key European banks, which reported profits that surpassed expectations. The FTSE 100 Index also rose 0.90% this week to 8213.49.

- Asian Markets Experience Mixed Outcomes: Hong Kong led the gains in Asia, with the Hang Seng index up 1.34%, while South Korea’s Kospi slipped by 0.26%. The Taiwan Weighted Index rose by 0.53%, reflecting a cautiously optimistic regional outlook.

- April Jobs Report Below Expectations Influences Rate Cut Hopes: The US economy added 175,000 jobs in April, significantly below the expected 240,000. This softer job growth, combined with a slight increase in the unemployment rate to 3.9%, has revitalised investor hopes for Federal Reserve rate cuts, with Fed funds futures indicating a nearly 50% likelihood of a 25 basis point cut by September.

- Significant Moves in Treasury Yields: Post-jobs report, the 10-year Treasury yield dipped below 4.5%, influencing a rally in rate-sensitive stocks and reinforcing the bond market’s role in shaping equity market trends.

- Oil Prices Decline Amid Economic Uncertainty: Brent crude futures fell to $82.96 a barrel, down 0.85%, while West Texas Intermediate crude dropped to $78.11 a barrel, a 1.06% decrease. Both benchmarks are set for their steepest weekly losses in three months, underscoring concerns that persistent high interest rates may dampen global economic growth and reduce demand for oil.

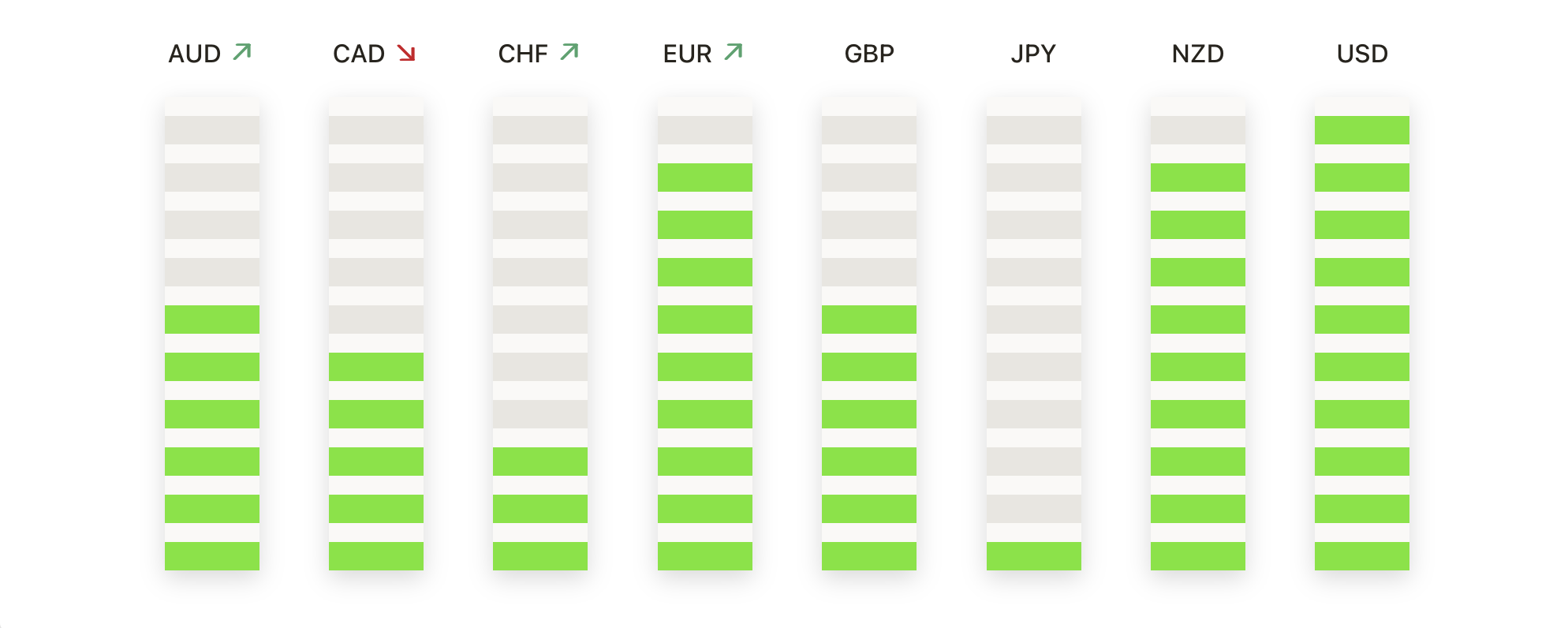

FX Today:

- EUR/USD Sees Uplift Amid Dollar Weakness: The EUR/USD pair advanced, breaking north of recent consolidation to hit a weekly high of 1.0813. This rise came after the pair navigated a rough supply zone between 1.0740 and 1.0720, with the week’s low parked at 1.0650. The surge reflects the market’s reaction to the weaker-than-expected US jobs data, which drove down the Greenback.

- GBP/USD Stalls Near Key Resistance Levels: Despite climbing earlier in the week, GBP/USD struggled to close above the 200-day simple moving average. This technical level may act as a pivotal point for future price actions, with potential resistance near 1.0620. On the downside, key support is observed from 1.2515 to 1.2500, where a breach could push the pair towards the 1.2430 level.

- USD/JPY Pulled Back Amid Intervention Rumours: The USD/JPY pair experienced significant volatility, weakening to 152.89, a 0.48% decline. This movement was influenced by suspected intervention from Japanese authorities, as traders eye the 152.00 mark for potential support. The week’s activities suggest a defensive posture from Japan, which may continue to impact the currency’s trajectory.

- NZD/USD Attempts to Break Key SMA: The NZD/USD pair showed signs of bullish momentum, rallying to around 0.6050, up by 0.80%. However, the pair faced resistance at the 100-day Simple Moving Average during Friday’s session, indicating that more traction is needed to turn the outlook bullish. The 20-day SMA’s breach, however, has improved the short-term outlook, potentially paving the way for further gains.

- USD/CAD Rebounds from Lower Boundaries: Following a quick fall into the 1.3610 level, USD/CAD rallied towards 1.3700. This bounce from the demand zone between 1.3680 and 1.3630 highlights the volatile nature of the pair amidst fluctuating market sentiments influenced by the US jobs report.

Market Movers:

- Apple Dominates with Record Buyback Announcement: Apple’s stock surged by more than 6% after the tech giant announced a record $110 billion share repurchase program and reported Q2 revenue of $90.75 billion, exceeding expectations. The announcement added significant momentum to Apple’s market valuation, influencing broader market sentiments.

- Amgen Leads with Strong Earnings and Drug Update: Biotech giant Amgen’s shares climbed more than 11%, marking its best day since 2009, after reporting Q1 adjusted EPS of $3.96, surpassing the consensus of $3.94. Amgen was also driven by positive updates on its experimental obesity drug MariTide, highlighting its potential market impact.

- Live Nation Entertainment Exceeds Revenue Expectations: Shares of Live Nation Entertainment soared more than 7% following a Q1 earnings report where revenue reached $3.80 billion, well above the consensus estimate of $3.26 billion. The strong performance reflects robust demand in the entertainment sector as live events continue to rebound.

- Arista Networks Upgraded, Shares Climb: Arista Networks saw its shares increase by more than 5% after Jeffries upgraded the stock to buy from hold, setting a price target of $320. The upgrade reflects growing confidence in Arista’s market position and future growth prospects.

- Motorola Solutions Reports Strong Sales and Upgrades Guidance: Motorola Solutions’ stock rose more than 4% after the company reported Q1 net sales of $2.39 billion, beating the consensus of $2.35 billion. The company also raised its full-year revenue growth forecast to about 7%, signalling stronger than expected market performance.

- Digital Realty Trust Beats FFO Estimates: Digital Realty Trust’s shares appreciated by more than 4% after reporting a Q1 core FFO per share of $1.67, surpassing the expected $1.63. The company also provided a bullish full-year core FFO guidance range, which is above the market consensus.

- Expedia Group Faces Setback on Lower Bookings: Expedia Group’s stock dropped over 15% as it reported Q1 gross bookings of $30.16 billion, missing the expected $30.50 billion. The drop highlights the challenges in the travel sector amid fluctuating global travel demand.

- Fortinet Disappoints on Billing Growth, Stock Declines: Shares of Fortinet fell by more than 9% after the cybersecurity firm reported Q1 billings of $1.41 billion, which was below the market’s expectation of $1.43 billion, raising concerns about its short-term growth trajectory.

- Ingersoll Rand Reports Weaker Than Expected Revenues: Ingersoll Rand saw its shares drop by more than 6% after reporting weaker than anticipated Q1 revenue of $1.67 billion, compared to the expected $1.70 billion, reflecting potential headwinds in the industrial sector.

The stock market has demonstrated remarkable resilience and adaptability, lifted by significant earnings reports and economic indicators that suggest a possible relaxation of Federal Reserve policies. The substantial gains in major indices, powered particularly by strong performances in the technology sector and exceptional earnings from corporate giants like Apple and Amgen, highlight a market filled with optimism. Additionally, the varied responses in the FX markets and the downturn in oil prices reveal the complex relationship between economic indicators and market sentiment. With renewed hopes for rate cuts, investors are well-prepared to manage the challenges of an evolving economic landscape, anticipating further developments that may shape market directions in the coming months.