The S&P 500, Dow Jones Industrials and Nasdaq 100 all closed higher, reflecting a market lifted by robust economic indicators. US Q4 GDP growth outpaced expectations, signalling a strong consumer spending environment and tempering fears of a hard economic landing. However, this optimistic economic backdrop was compared against mixed corporate results, with notable movements in key companies like United Rentals and IBM, alongside a downturn in Tesla and health insurers. As investors parsed through a variety of economic and corporate data, the market’s pulse seemed to synchronise with the Federal Reserve’s potential policy manoeuvres, awaiting the central bank’s next steps with bated breath.

Key Takeaways:

- Indices Show Moderate Gains: The S&P 500 Index closed up by 0.53%, the Dow Jones Industrials Index by 0.64%, and the Nasdaq 100 Index by 0.10%, reflecting a market boosted by positive economic data and corporate earnings.

- Strong US Economic Indicators: US Q4 GDP growth accelerated to an annualised pace of 3.3%, surpassing the forecasted 2.0%. Personal consumption also grew more than expected at 2.8%, highlighting consumer resilience.

- Housing Market Showing Strength: December’s new home sales surged by 8.0% month-over-month to 664,000, outstripping the anticipated 649,000, underscoring strength in the housing sector.

- Corporate Earnings Paint Mixed Picture: United Rentals soared over 12% after a strong Q4 report, and IBM rose more than 9% on better-than-expected Q4 operating EPS. Conversely, Tesla’s shares dropped over 12% following weaker Q4 adjusted EPS, and health insurers, led by an 11% drop in Humana, retreated on weak 2024 EPS forecasts.

- Global Market Reactions: European markets closed higher, with the Stoxx 600 up by 0.29%, and Asian markets showed strength, led by China and Hong Kong stocks. The Hang Seng index jumped 1.8%, and China’s CSI 300 closed 2% higher at 3,342.92, lifted by the People’s Bank of China’s liquidity-boosting measures.

- Corporate Earnings Influence: Standout corporate performances included United Rentals and IBM, with their stocks closing up more than 12% and 9% respectively, following stronger-than-expected earnings reports. Conversely, Tesla’s shares dropped significantly by over 12% after its earnings release, influencing the tech sector’s overall sentiment.

FX Today:

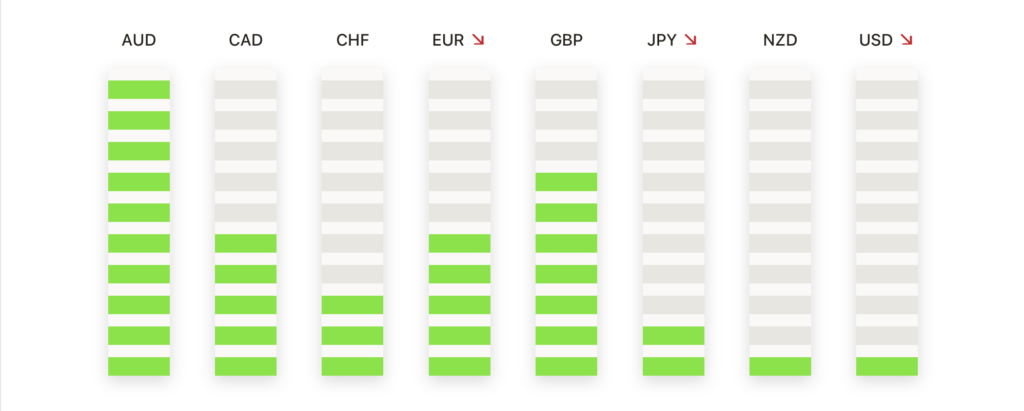

- Euro’s Struggle Amid Mixed Signals: The Euro experienced a notable dip, falling below its 200-day simple moving average near 1.0840. This movement indicates potential further declines, with the next key support level eyed at 1.0770. The currency’s trajectory remains under scrutiny, as analysts predict a possible pullback towards 1.0710 should the current weakness persist.

- British Pound’s Technical Retreat: The GBP/USD pair saw a retreat after failing to breach the upper resistance of a symmetrical triangle pattern, hovering around 1.2750 – 1.2770. A decisive break could lead to further momentum, potentially aiming for the 1.2830 mark or even the 1.3000 threshold in an extended rally.

- Gold Prices Show Resilience: Gold prices have recently found stability, trading between key technical thresholds of $2,030 (trendline resistance) and $2,005 (horizontal support). This consolidation phase reflects a cautious sentiment in the market, with a potential breakout on either side likely to set the new direction. A breach above $2,030 could propel prices towards $2,065, while a downside break might test supports at $1,990 and $1,975.

- NZD/USD Maintains Defensive Stance: The NZD/USD pair trades slightly weaker, hovering above the 0.6100 mark. The pair’s movements are influenced by the stronger GDP growth in the US, bolstering the USD. Traders are now focusing on the upcoming US Core PCE data, a key inflation indicator, for further cues. Currently, the pair stands at 0.6109, down marginally by 0.03% for the day.

- Oil Prices and Sectoral Movements: West Texas Intermediate crude futures settled up 3%, or $2.27, at $77.36 a barrel, while Brent crude finished up 2.99%, or $2.39, at $82.43, influenced by geopolitical tensions and supply chain risks.

Market Movers:

- United Rentals (URI) Surges on Strong Earnings: United Rentals led the gainers in the S&P 500 with a significant jump of over 12%. This surge came after the company reported Q4 revenue of $3.73 billion, exceeding the consensus estimate of $3.65 billion. Moreover, its 2024 revenue forecast of $14.65 billion to $15.15 billion, with the midpoint above the consensus of $14.8 billion.

- American Airlines Group (AAL) Soars on Upbeat Forecast: American Airlines Group’s stock closed up by more than 10% following its 2024 adjusted EPS forecast of $2.25-$3.25, well above the consensus of $2.22. The positive outlook also lifted other airline stocks, with United Airlines Holdings (UAL) closing up more than 5% and Delta Air Lines (DAL) up over 4%.

- ResMed (RMD) Advances on Earnings Beat: ResMed’s shares closed up more than 7% after the company reported a Q2 adjusted EPS of $1.88, stronger than the expected $1.79. This positive earnings surprise contributed to the stock’s upward movement.

- WR Berkley (WRB) Climbs on Premiums Written: WR Berkley’s stock ended the day up more than 7% following the report of Q4 net premiums written at $2.72 billion, which was better than the consensus of $2.67 billion.

- Humana (HUM) Leads Losses on Earnings Forecast: Humana’s shares plunged, closing down more than 11% and leading the losses in the S&P 500. This was a reaction to the company forecasting its 2024 adjusted EPS at about $16.00, significantly below the consensus of $29.18, and withdrawing its 2025 earnings target.

- Northrop Grumman (NOC) Declines on Sales Forecast: Northrop Grumman’s stock closed down more than 6% after forecasting 2024 sales of $40.80 billion to $41.20 billion, with the midpoint below the consensus of $41.15 billion.

- Boeing (BA) Drops Amid Production Halt: Boeing’s shares closed down more than 5%, leading the losses in the Dow Jones Industrials, following the FAA’s halt on planned production increases of the 737 Max airliner.

As the market closes on a day characterised by robust economic data compared with varied corporate performances, investors find themselves navigating through a landscape of optimism. The stronger-than-expected US economic growth and stable inflation figures offer a glimmer of hope for a soft landing, despite the undercurrents of uncertainty in the labour market. The divergent corporate earnings, from United Rentals’ robust performance to Tesla’s downturn, further add layers to this complex financial mosaic. As the market digests these mixed signals, all eyes are now on the Federal Reserve’s forthcoming policy decisions, with the subtle shifts in economic indicators likely to sway the delicate balance of market sentiment. In this intricate dance of macroeconomic trends and corporate narratives, investors remain alert, parsing through the data to chart their course in an ever-evolving economic environment.