In a reversal from its recent upward trajectory, the stock market faced a downturn on Friday, shaken by the latest inflation reports that spurred a re-evaluation of the Federal Reserve’s expected timeline for interest rate adjustments. The Dow Jones Industrial Average, S&P 500, and Nasdaq Composite all retreated, halting a five-week stretch of gains. The producer price index for January indicated a rise beyond forecasts, igniting concerns over inflationary pressures and casting doubt on the likelihood of near-term monetary easing by the Fed. This shift has introduced a heightened level of uncertainty within the financial markets, as investors recalibrate their expectations in light of persistent inflation and a mixed landscape of economic indicators and corporate earnings.

Key Takeaways:

- Broad Market Retracement Ends Winning Streak: The Dow Jones Industrial Average slid 145.13 points to close at 38,627.99, marking a 0.37% decrease, while the S&P 500 and Nasdaq Composite fell by 0.48% to 5,005.57 and 0.82% to 15,775.65, respectively. This marked the end of a five-week winning streak for all three major indexes, with the S&P 500 and Nasdaq ending the week lower by 0.42% and 1.34%, and the Dow slipping by 0.11%.

- Producer Price Index Surpasses Expectations: The January PPI rose by 0.3%, exceeding the Dow Jones economists’ forecast of a 0.1% gain. Core PPI, excluding food and energy, increased by 0.5%, surpassing expectations for a 0.1% rise, highlighting persistent inflationary pressures.

- Treasury Yields Climb on Inflation Worries: Post-PPI report, the 10-year Treasury yield surged above 4.3%, and the 2-year yield reached 4.7%, its highest since December. These movements reflect growing concerns about inflation’s trajectory and its implications for Federal Reserve policy.

- Mixed Domestic Economic Indicators: The U.S. housing market indicators weakened, with January housing starts and building permits both falling unexpectedly. Conversely, the University of Michigan’s February consumer sentiment index rose to a 2-1/2 year high, presenting a mixed economic outlook.

- European Markets Edge Higher: European stocks closed higher, with the Stoxx 600 index up 0.6%. Mining stocks led the gains, while U.K. retail sales outperformed expectations, signalling potential economic resilience despite technical recession indicators.

- Asian Markets Show Mixed Responses: The Nikkei 225 in Japan approached an all-time high, indicating optimism around continued loose monetary policy amid economic slowdown signals. Meanwhile, Hong Kong’s Hang Seng index surged, leading gains across Asia-Pacific markets, with investors keenly watching global inflation trends and Fed policy implications.

FX Today:

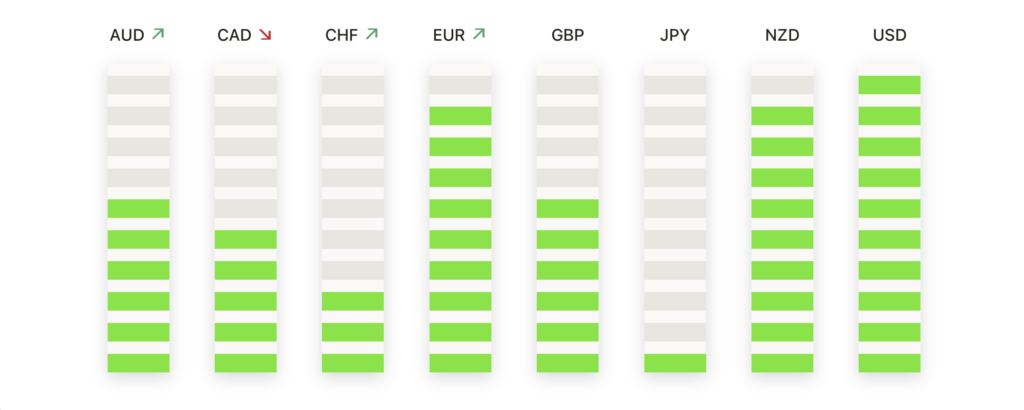

- Euro Faces Downward Pressure Amid Inflation Concerns: The EUR/USD pair encountered resistance below the 1.0800 threshold as the U.S.’s stronger-than-expected PPI report fuelled speculation that the Federal Reserve might delay interest rate cuts. The pair struggled for direction, oscillating around the 200-hour Simple Moving Average (SMA) at 1.0760, reflecting the market’s reassessment of the Fed’s policy trajectory.

- Pound Sterling Rallies on Strong Retail Sales: The GBP/USD pair advanced to 1.2617, helped greatly by an unexpectedly robust UK retail sales report, which indicated a 3.4% month-on-month increase, significantly above the anticipated 1.5%. This upbeat data provided a boost to the Pound, suggesting a quicker rebound from the recent technical recession and lending support amidst varied U.S. economic signals.

- Canadian Dollar Wavers After Inflation Data: The USD/CAD pair showed little movement, trading around the 1.3490 mark, close to the 200-hour SMA. Despite positive Canadian securities investment data, the U.S. inflation report’s implications for delayed Fed rate cuts left the Canadian Dollar in a state of uncertainty against a backdrop of mixed global sentiments.

- Yen Steadies Above 150.00 Amid Rate Speculations: The USD/JPY pair held firm above the 150.00 level, trading at 150.16, reflecting a modest gain of 0.16%. The pair’s outlook remains optimistic, with eyes on breaking above the 151.00 barrier, influenced by ongoing discussions around U.S. inflation and potential shifts in Fed policy.

- Gold Advances Amid Inflation and Policy Uncertainty: Gold prices saw an uptick, reaching a three-day high at $2015, as the U.S. dollar weakened despite a rise in Treasury yields. The precious metal’s gain reflects growing investor concern over persistent inflation and the Federal Reserve’s signals on policy adjustment. Despite the week’s overall loss, gold’s recovery underscores its appeal as a hedge against inflation and policy uncertainty.

- Crude Oil Climbs, WTI Tests $78.00 Barrier: West Texas Intermediate (WTI) crude oil extended its rebound, briefly touching $78.40 before settling around $78.20. This near-term bullish momentum, supported by the 200-hour SMA at $76.10, indicates a potential technical breakout. The oil market’s resilience, amidst fluctuating demand and geopolitical factors, suggests a cautious optimism for energy commodities.

Market Movers:

- Digital Realty Takes a Dive: Digital Realty (DLR) led the decliners in the S&P 500, closing down more than 8% after its fourth-quarter funds from operations (FFO) per share of $1.63 fell short of the consensus estimate of $1.65. The company’s forecast for full-year FFO per share between $6.60 and $6.75 also missed market expectations of $6.84, sparking investor concerns over future profitability.

- Nike Stumbles on Downgrade: Nike (NKE) saw a more than 2% drop, making it one of the Dow Jones Industrials’ major losers after Oppenheimer downgraded the stock from outperform to perform. The downgrade reflects growing caution about the company’s near-term growth prospects amidst competitive and market challenges.

- DoorDash’s Forecast Disappoints: DoorDash (DASH) experienced an 8% decline, leading losses in the Nasdaq 100, after projecting a full-year marketplace gross order value of $74 billion to $78 billion. This forecast, with its midpoint below the consensus of $76.54 billion, raised concerns about the food delivery service’s growth trajectory in a competitive environment.

- Roku’s Flat Earnings Outlook Shocks Investors: Roku (ROKU) shares plummeted over 23% following its first-quarter adjusted EBITDA guidance of $0, starkly underwhelming against the expected $12.5 million. The disappointing outlook triggered a sell-off, underscoring investor worries over the streaming platform’s profitability amid rising costs and heightened competition.

- Dropbox Underwhelms with User Growth: Dropbox (DBX) fell more than 23% after its fourth-quarter report showed paying users at 18.12 million, below the forecasted 18.21 million. The slower-than-expected user growth has cast doubts on the company’s market positioning and future expansion plans.

- TreeHouse Foods Faces Sales Shortfall: TreeHouse Foods (THS) closed down over 15% following its report of Q4 net sales at $910.8 million, missing the expected $925 million. The shortfall highlighted challenges in the consumer packaged goods sector, impacting investor sentiment.

- Yelp Inc’s Earnings Forecast Worries Market: Yelp Inc (YELP) ended the day down more than 14% after setting its full-year adjusted EBITDA target at $315 million to $335 million, below the market consensus of $342.4 million. The weaker-than-anticipated earnings guidance prompted concerns over the online review site’s growth amid advertising market fluctuations.

- Applied Materials Surges on Strong Earnings: Conversely, Applied Materials (AMAT) bucked the trend by closing up more than 6%, leading gainers in the S&P 500, after reporting Q4 net sales of $6.71 billion, surpassing expectations of $6.48 billion. The company’s optimistic sales forecast for Q2 further fuelled the stock’s upward momentum, highlighting strong demand for semiconductor manufacturing equipment.

- Trade Desk Soars on Revenue Beat: Trade Desk (TTD) enjoyed a more than 17% jump, topping gains in the Nasdaq 100, after its fourth-quarter revenue of $606 million exceeded analysts’ estimates of $582.1 million. The advertising technology company’s positive outlook for Q1 revenue also contributed to investor enthusiasm, underscoring the strength of digital advertising demand.

The markets have navigated through a maze of economic indicators, corporate earnings, and central bank policy speculations, culminating in a week marked by volatility and reassessment of investor expectations. The contrast of stronger-than-anticipated inflation data against mixed corporate earnings underscores the interplay between macroeconomic trends and individual company performances. While certain sectors and companies have showcased resilience and growth potential, others have faltered, highlighting the multifaceted nature of the current financial landscape. Investors, now more than ever, are urged to remain vigilant, adapting to the evolving market dynamics with a keen eye on inflation trends, monetary policy shifts, and corporate health to navigate the uncertainties ahead.