In a financial landscape riddled with volatility, global markets are navigating through a blend of uncertainty and recalibration. Major indices like the Dow Jones, S&P 500, and Nasdaq are reacting sensitively to shifting labour data and central bank policies. The close of 2023 sees investors wrestling with mixed signals. The labour market hinting at easing inflation yet bracing for adjustments and central banks like the Bank of England delicately balancing inflation control with economic growth paints a complex picture of the global economic scenario.

Key Takeaways:

- Volatility in Major Indices: The Dow Jones, S&P 500, and Nasdaq displayed volatility, with the Dow dropping 0.2% and the S&P 500 and Nasdaq both falling 0.4% and 0.5% respectively. This reflects the market’s sensitivity to rapid shifts in economic conditions and policy changes.

- Labour Market Developments: Labour costs decreased significantly, showing a 1.2% drop in the third quarter, while private payrolls increased by 103,000 in November, signalling a potential shift in the job market dynamics.

- Interest Rate Policies by Central Banks: The Bank of England and other central banks are fine-tuning their policies in response to economic signals. The BoE, for instance, has increased rates by over 500 basis points since December 2021, emphasising the delicate balance between curbing inflation and promoting growth.

- Corporate Sector Trends: Major companies like Box and Toll Brothers reported contrasting performances, with Box shares dropping nearly 11% post-earnings while Toll Brothers gained over 2% following a strong financial report.

- Energy Market Dynamics: U.S. crude oil prices fell sharply by 4%, closing at their lowest since late June at $69.38 a barrel, despite OPEC+’s supply cut strategies, indicating a complex scenario in the global energy sector.

- Corporate Movements and Stock Performance: Box Inc. experienced a significant drop, with shares tumbling nearly 11% following a third-quarter earnings report that fell short of expectations. Conversely, Toll Brothers saw its stock rise over 2% after reporting earnings that surpassed forecasts on both top and bottom lines.

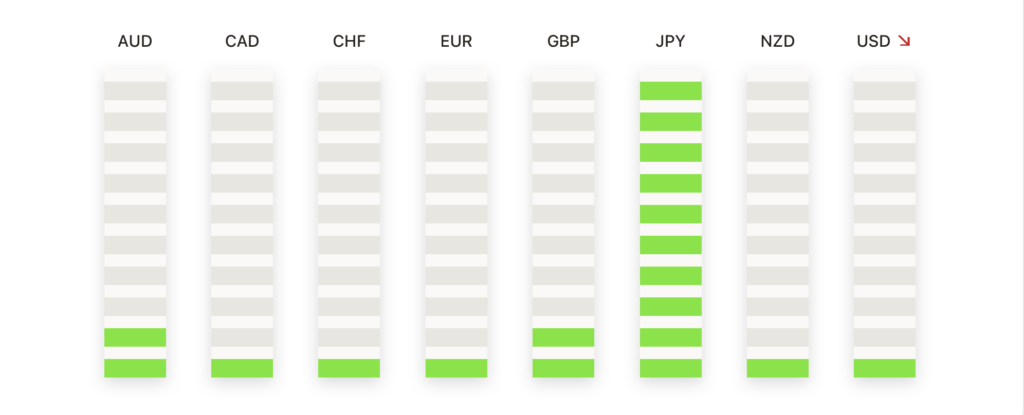

- Currency Pair Fluctuations: Major currency pairs like EUR/USD and GBP/USD saw significant movement, with EUR/USD dropping to a 2.5-week low at 1.0700 and GBP/USD declining towards 1.2600, a retreat of approximately 100 pips.

- European Markets’ Resilience: The European markets, especially Germany’s DAX, showcased strength, with the DAX extending its record high. This resilience indicates a diverging pattern in economic performance across regions.

- Precious Metals as Market Indicators: Gold prices, after peaking at $2,146, pulled back sharply to around $2,020, while silver also faced a downward trend, highlighting their roles as indicators of market sentiment and broader economic trends.

FX Today:

- GBP/USD Under Pressure: The GBP/USD pair witnessed a significant decline, dropping below the 1.2700 level and shedding over 1% during the week. The pair traded at 1.2555, down 0.28% after reaching a daily high of 1.2613. This downward trend is influenced by disappointing ADP Employment Change data from the US and ongoing financial pressures signalled by the Bank of England.

- EUR/GBP Struggles: The EUR/GBP pair remained in a tight consolidation, trading just above 0.8560. The Euro saw a marginal week-on-week gain against the Pound but remained under pressure due to poor European Retail Sales data, which contracted by 1.2% year-on-year in October, and upcoming Eurozone GDP figures.

- Canadian Dollar’s Mixed Performance: After the Bank of Canada held interest rates steady at 5%, the Canadian Dollar (CAD) experienced mixed results. The CAD saw marginal gains against the US Dollar initially but lost ground later, indicating market uncertainty and reaction to the central bank’s policy stance.

- EUR/USD Continues to Decline: The EUR/USD pair extended its losses, dropping further by 0.3% and heading towards 1.0700. This decline reflects the Euro’s continued weakness, exacerbated by lower-than-expected Retail Sales in the Eurozone and anticipation of the Eurozone GDP report.

Conclusion:

As trading activities wind down, the global financial markets reflect a real back-and-forth of economic factors, from fluctuating stock indices to shifting currency values. This landscape – marked by the contrasting resilience of European markets and the cautious approach of U.S. indices – is shaped by labour market trends, central bank policies, and global economic developments. With the anticipation building around upcoming economic data, including the Nonfarm Payrolls report, it is evident that the financial markets are in a dynamic state, with each new development potentially redirecting the intricate narrative of global finance.

This material is for general information purposes only and is not intended as (and should not be considered to be) financial, investment or other advice on which reliance should be placed. INFINOX is not authorised to provide investment advice. No opinion given in the material constitutes a recommendation by INFINOX or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

All trading carries risk.