US stocks soared on Friday as Federal Reserve Chair Jerome Powell indicated the central bank could begin easing policy as soon as September. The Dow Jones Industrial Average surged more than 800 points to a record close, leading a broad market rally that lifted the S&P 500 close to all-time highs and sent the Nasdaq sharply higher. Technology shares, which had weighed on indices earlier in the week, staged a strong comeback as Powell’s Jackson Hole speech raised expectations for imminent rate cuts.

Key Takeaways:

- Dow Hits Record High on Powell’s Remarks: The Dow Jones jumped 846.24 points, or 1.89%, to 45,631.74, its highest ever close. Friday’s rebound capped a weekly gain of 1.5% after losses earlier in the week, with Powell’s dovish comments providing a decisive shift in sentiment.

- S&P 500 Nears Record Peak: The S&P 500 advanced 1.52% to 6,466.91, coming within three points of its record high before settling just shy of the mark. On the week the index added 0.3%, with strength in housing and semiconductors offsetting earlier weakness in technology.

- Nasdaq Rebounds But Still Lower on Week: The Nasdaq Composite climbed 1.88% to 21,496.53, lifted by strong gains in megacap technology. Tesla surged about 6%, while Alphabet and Amazon added than 3% each. Despite the rally, the index still closed the week down 0.6%.

- Europe Rallies as FTSE 100 Posts Best Week Since May: European equities ended broadly higher, buoyed by Fed rate cut hopes and progress on a US-EU trade deal. London’s FTSE 100 rose 0.13% on Friday to notch its fourth straight record close at 9,321.40, gaining 2% on the week, its strongest since May. The STOXX 600 added 0.5% to 562, just short of record territory, while the STOXX 50 gained 0.5% to 5,492. France’s CAC 40 rose 0.5% to 7,970, and Germany’s DAX advanced 0.5% past 24,400. Italy’s FTSE MIB added 0.69%. Sentiment was supported despite Germany’s GDP revision showing a 0.2% contraction in Q2, with analysts warning growth may remain subdued into 2026. UK consumer confidence also improved in August, though concerns remain over inflation and taxation.

- Asia Mixed Ahead of Powell Speech: Asia-Pacific markets finished mostly higher on Friday as investors awaited Powell’s address. South Korea’s Kospi gained 0.86% to 3,168.73, while the Kosdaq added 0.68%. Japan’s Nikkei 225 ended flat at 42,633.29, with the Topix rising 0.58% to 3,100.87. Core CPI in Japan eased to 3.1% in July, still above forecasts. China’s CSI 300 jumped more than 2% to 4,378 and Hong Kong’s Hang Seng added 0.32%, with Hong Kong inflation cooling to a four-year low at 1.0%. Australia’s S&P/ASX 200 slipped 0.57% to 8,967.4 after hitting 9,000 for the first time Thursday. India’s Nifty 50 fell 0.67% and the Sensex dropped 0.62%.

- Oil Prices Steady but Record Weekly Gain: Brent crude settled at $67.73 and WTI at $63.66, up 0.09% and 0.22% respectively on Friday. Both contracts rose for the first time in three weeks, with Brent gaining 2.9% and WTI 1.4% for the week. Prices were supported by a larger-than-expected US stockpile draw of six million barrels and ongoing supply risks from the Russia–Ukraine conflict, including damage to refineries and the Druzhba pipeline.

- Treasury Yields Fall as Fed Cut Bets Surge: US Treasury yields dropped after Powell’s speech. The 10-year yield fell more than 7.5 basis points to 4.256%, while the 2-year yield dropped 10 basis points to 3.69%. Markets are now pricing a more than 91% probability of a September rate cut, up from around 75% earlier in the week.

FX Today:

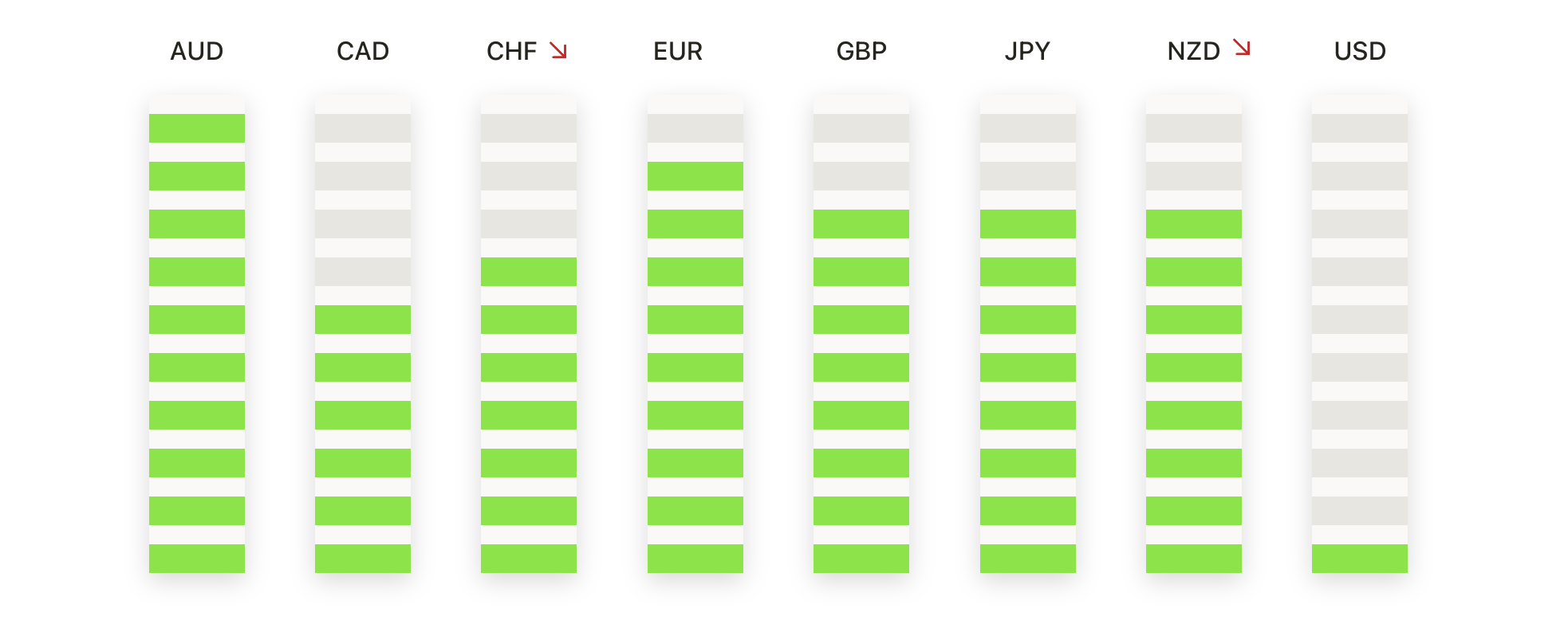

- EUR/USD Breaks Higher as Bulls Eye Resistance: EUR/USD closed at 1.1722, up 1.00% after trading between 1.1583 and 1.1743, with a strong green candle extending the rebound from earlier lows. The close above the 50-day SMA at 1.1648 confirmed renewed momentum, while the broader bullish structure remains intact with the 100-day SMA at 1.1483 and the 200-day at 1.1007 both trending higher. The pair has been consolidating beneath the 1.1850 ceiling since June, but higher lows above the 100-day SMA continue to underpin the uptrend. Immediate resistance is now 1.1745, with a break opening the path toward 1.1800–1.1850. Support lies at 1.1650 and deeper at 1.1480, keeping the bias bullish while above 1.1650.

- GBP/USD Rebounds Sharply as Buyers Reclaim Control: GBP/USD settled at 1.3528, up 0.85% after trading between 1.3391 and 1.3544, as a strong green candle reversed the prior pullback. The close above the 50-day SMA at 1.3495 and the 100-day SMA at 1.3416 highlighted regained strength, with the broader uptrend supported by the rising 200-day SMA at 1.3023. The rebound confirms 1.3400 as a key floor, with topside resistance at 1.3550 and then 1.3650, followed by scope to extend toward 1.3750. On the downside, support remains at 1.3495 and 1.3415, keeping the outlook bullish while above these levels.

- USD/CHF Extends Decline Toward Support: USD/CHF closed at 0.8014, down 0.91% after ranging between 0.8010 and 0.8100, producing a decisive red candle that dragged the pair to fresh August lows. The close beneath the 50-day SMA at 0.8031 showed sellers regaining control, with the broader structure remaining bearish as both the 100-day SMA at 0.8144 and 200-day SMA at 0.8544 continue to slope lower. Since May, rallies have consistently failed beneath these averages, keeping pressure to the downside. Immediate focus is 0.8000, with a break likely exposing the July low near 0.7930, while resistance stands at 0.8050 and then 0.8140. Bias stays bearish while below 0.8050.

- USD/JPY Slides Back as Sellers Defend 148.50 Region: USD/JPY ended at 146.93, down 0.97% after moving between 146.57 and 148.78, printing a large red candle that erased the prior day’s rally. The close just under the 50-day SMA at 146.79 signalled fading momentum, while the broader picture remains mixed with the 100-day SMA at 145.45 acting as support and the 200-day SMA at 149.08 continuing to cap the topside. Structurally, the pair has been consolidating within a 144.50–150.50 range since July, with repeated failures above 149.50. Support is now at 146.50 and then 145.50, while rebounds face resistance at 147.50 and 148.50. The bias remains tilted lower while capped beneath the 200-day SMA.

- AUD/USD Bounces Back as Buyers Defend 0.6450 Base: AUD/USD closed at 0.6492, up 1.12% after trading between 0.6415 and 0.6501, forming a strong green candle that reversed earlier weakness. The recovery above the 100-day SMA at 0.6457 underscored demand at this level, though the 50-day SMA at 0.6513 still acts as nearby resistance. The longer-term floor remains the 200-day SMA at 0.6385. Price continues to oscillate between 0.6400 and 0.6650 since June, with yesterday’s rebound reinforcing the importance of the 0.6450 zone. Resistance is now eyed at 0.6515, 0.6550, and 0.6620, while support stays at 0.6450 and 0.6385.

- Gold Rallies Back Toward Resistance: Gold closed at $3,371, up 0.99% after ranging between $3,322 and $3,378, with a firm green candle rebounding from earlier pullbacks. The close above the 50-day SMA at $3,349 and 100-day SMA at $3,309 highlighted buyers regaining momentum, while the 200-day SMA at $3,042 continues to support the broader uptrend. Gold has been consolidating beneath the $3,450 ceiling while holding support above $3,300. Resistance now sits at $3,378 and then $3,400, with scope to retest the July highs if broken. Support is layered at $3,349 and $3,309, keeping the outlook bullish above the 50-day SMA.

Market Movers:

- Chipmakers Lead Broad Market Gains: Semiconductor stocks surged as ON Semiconductor jumped more than 6%, while GlobalFoundries and Intel climbed over 5%. NXP Semiconductors and Microchip Technology gained more than 4%, and ARM Holdings advanced over 3%. Additional strength came from AMD, Texas Instruments, Marvell Technology, ASML, and Qualcomm, all of which closed up more than 2%.

- Megacap Technology Stocks Rebound Sharply: The Magnificent Seven provided a major boost, with Tesla soaring over 6%, Alphabet and Amazon rising 3%, and Meta advancing 2%. Apple and Nvidia added more than 1% each, while Microsoft finished higher by 0.59%.

- Travel and Leisure Stocks Jump on Economic Optimism: Airlines and cruise operators rallied as Norwegian Cruise Line, American Airlines, and Alaska Air gained more than 7%. Carnival, Delta, and Royal Caribbean advanced over 6%, while United Airlines and Southwest Airlines both added more than 5%.

- Homebuilders Rally as Yields Fall: Housing-related stocks surged after the 10-year Treasury yield dropped to a one-week low, easing financing costs. Builders FirstSource gained more than 8%, Mohawk Industries added over 7%.

- Ubiquiti Soars on Strong Earnings Beat: Ubiquiti surged more than 29% after reporting Q4 revenue of $759.2 million, well ahead of consensus expectations of $621 million.

- Zoom Communications Jumps on Upgraded Outlook: Zoom rose 12% after reporting Q2 revenue, slightly ahead of forecasts, and lifting its 2026 revenue guidance to $4.83 billion.

- Intuit Sinks on Weak Guidance: Intuit fell more than 5% to lead declines in the S&P 500 and Nasdaq 100 after issuing 2026 adjusted operating income guidance of $8.61–$8.69 billion.

- Workday Slips on Unexpected Loss: Workday eased more than 2% after reporting a surprise $5 million loss in Q2 professional services adjusted gross profit, compared with expectations of a $9.5 million profit.

Friday’s rally marked a dramatic turnaround for global markets, with Powell’s Jackson Hole remarks resetting expectations for a September rate cut and driving the Dow to fresh records. The renewed strength in megacap technology, combined with broad gains across housing, travel, and semiconductors, reinforced optimism that looser financial conditions could support risk appetite in the weeks ahead. Yet, with Europe still wrestling with weak growth signals and Asia facing mixed momentum, investor focus now shifts to upcoming data and central bank guidance to confirm whether this rally can extend into September.