Risk appetite softened on Thursday as investors stepped back from financials and reassessed geopolitical and credit-market risks, leaving US equities broadly lower by the close. Concerns around liquidity in private credit intensified after a major asset manager moved to tighten investor access, while rising oil prices added another layer of unease amid escalating rhetoric between Washington and Tehran. The cautious tone was reinforced by renewed pressure in software shares and a sharp sell-off in select consumer names, keeping markets defensive despite pockets of resilience in economic data.

Key Takeaways:

- Dow Jones Industrial Average Slides on Financial Weakness: The 30-stock index declined by 267.50 points, or 0.54%, to finish at 49,395.16. Losses were primarily driven by a sharp retreat in asset managers and financial institutions after liquidity concerns in the private credit market.

- S&P 500 Hovers Near Break-Even for the Year: The broad-market index slipped 0.28% to close at 6,861.89, leaving it with a marginal year-to-date gain of just 0.2%. Sentiment was weighed down by a mix of lacklustre earnings guidance from major retailers and geopolitical uncertainty.

- Nasdaq Composite Pressured by Software and AI Concerns: The tech-heavy index fell 0.31% to end at 22,682.73, extending its 2026 decline to over 2%. Software stocks faced significant headwinds following executive commentary suggesting that artificial intelligence could displace a substantial portion of existing enterprise software.

- Europe Slides as Earnings Weigh Despite Mixed Data Signals: European equities finished lower, with the STOXX 600 down 0.6% and major bourses ending in the red, led by a 1.22% fall in Italy’s FTSE MIB to 45,794 and a 0.93% drop in Germany’s DAX to 25,044, while the FTSE 100 fell 0.69% to 10,613 and the CAC 40 slipped 0.36% to 8,399. Airbus shares fell about 7% after guiding to 870 commercial aircraft deliveries in 2026, slightly below expectations, while Renault ended around 3% lower after reporting 2025 revenue up 3% to €57.9 billion but a net loss of €10.9 billion driven by a one-off Nissan-related charge. On the data front, the UK’s CBI order book balance improved to -28 in February from -30, still weak but the slowest pace of decline since September, Ireland’s inflation eased to 2.7% in January from 2.8%, and Eurozone construction output fell 0.9% year on year in December, a softer contraction than November as civil engineering growth offset ongoing weakness in building activity.

- Asia-Pacific Rallies Led by Korea Record High: Asian markets advanced, led by South Korea where the Kospi surged more than 3% to a record close of 5,677.25, with Samsung Electronics up 4.86% and SK Hynix up 1.59%, while the Kosdaq jumped nearly 5% to 1,160.71. Australia’s S&P/ASX 200 rose 0.88% to 9,086.2 as unemployment held at a seven-month low in January, though employment growth of 17.8K undershot forecasts, and New Zealand’s NZX 50 climbed 1.3% to 13,420. Japan’s Nikkei 225 added 0.57% to 57,467.83 and the Topix rose 1.18% to 3,852.09, while Hong Kong and mainland China remained closed for the Lunar New Year.

- Oil Extends Weekly Gains as Iran Standoff Intensifies: Oil prices rose sharply after President Donald Trump said he would decide within 10 days whether to launch military strikes against Iran, keeping markets on edge through the session. US crude settled up $1.54, or 2.36%, at $66.73 per barrel, while Brent gained $1.53, or 2.17%, to $71.88. WTI is up more than 5% this week and nearly 16% so far this year, underscoring how geopolitics is becoming a more direct input into risk pricing.

- Treasury Yields Hold Steady as Investors Weigh Stronger Data: US Treasury yields were little changed, reflecting a market balancing improved macro signals against upcoming inflation data and broader risk headlines. The 10-year yield dipped by less than 1 basis point to 4.075%, the 30-year eased similarly to 4.704%, and the 2-year was 1 basis point higher at 3.47%. The muted move suggested investors largely absorbed the day’s upbeat economic releases without materially repricing the near-term rates outlook.

- US Jobless Claims Drop to Lowest Level of the Year: Initial jobless claims fell by 23,000 to 206,000 in the second week of February, well below expectations for 225,000, pointing to a steadier labour backdrop. Continuing claims rose by 17,000 to 1,869,000 in the first week of February, consistent with slow firing momentum alongside softer hiring. Claims filed by federal employees rose by 80 to 695, remaining a closely watched detail as markets assess broader public-sector disruption risks.

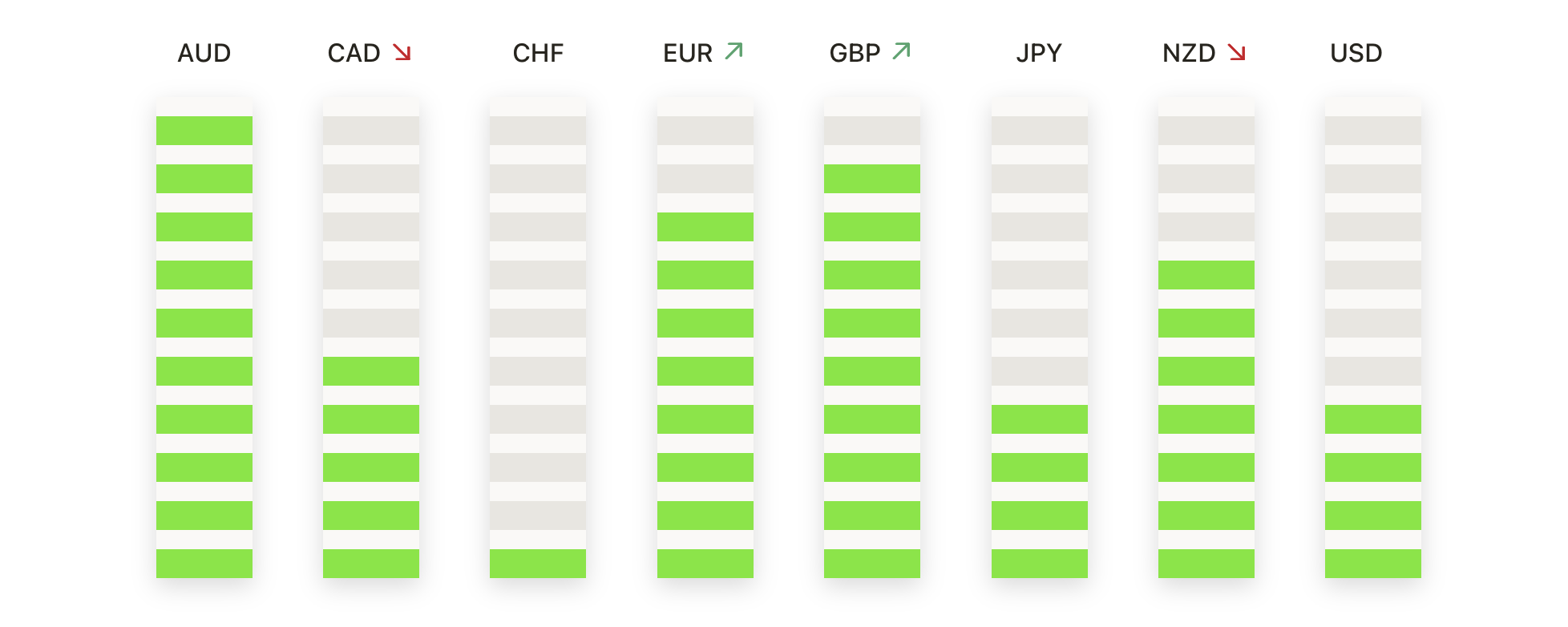

FX Today:

- EUR/USD Holds Above Medium-Term Support: EUR/USD edged lower, closing at 1.1768, down 0.13% after trading between 1.1807 and 1.1742. The pair eased from recent highs but continues to trade just below the 50-day SMA at 1.1769 while holding comfortably above the 100-day and 200-day SMAs at 1.1688 and 1.1644, respectively. The pullback reflects a loss of short-term momentum following the February peak rather than a structural shift, with price still consolidating gains made since late 2025. Dip demand remains evident near the 1.1740 area, while the 1.1688 region continues to act as a deeper support zone. Resistance is clearly defined at 1.1807, ahead of the psychologically important 1.1900 level.

- GBP/USD Stays Pressured Below Key Resistance: GBP/USD closed at 1.3458, down 0.26%, after failing to sustain gains above 1.3500 earlier in the session. Price remains capped below the declining 50-day SMA at 1.3525, reinforcing near-term selling pressure, though the pair continues to trade between the 100-day SMA at 1.3393 and the 200-day SMA at 1.3442. The inability to reclaim the 50-day average highlights fading upside momentum following the strong rally from late-2025 lows. Immediate resistance remains clustered around 1.3517–1.3525, while initial support is located at 1.3454. A move below 1.3393 would tilt the outlook more decisively lower, while holding above the longer-term averages may allow consolidation to develop.

- USD/JPY Rebounds from Medium-Term Support: USD/JPY closed at 155.07, up 0.20%, after bouncing from an intraday low of 154.54. The pair found support close to the 100-day SMA at 154.74, signalling renewed buying interest after the recent pullback from multi-year highs. While price remains below the 50-day SMA at 155.96, it continues to trade well above the rising 200-day SMA at 150.60, preserving the broader uptrend. Resistance is now seen at 155.34 and then at the 50-day average, which remains key for upside continuation. On the downside, sustained trading above 154.74 keeps the recovery narrative intact, while a break below 154.54 would expose deeper support toward the 200-day SMA.

- Gold Consolidates Above Rising Averages: Gold settled at $5,001, up 0.50%, after trading between $5,022 and $4,960. The metal rebounded from intraday weakness to close higher, maintaining a clear position above the 50-day, 100-day, and 200-day SMAs at $4,863, $4,385, and $3,860. Recent price action reflects consolidation following the sharp February rally to record highs, with buyers continuing to defend dips above the 50-day average. Resistance remains defined at $5,022, ahead of the prior swing high near $5,200. On the downside, initial support sits at $4,960, with stronger backing near the 50-day SMA. A sustained break above resistance would refocus attention on fresh highs.

- Silver Rebounds but Faces Overhead Resistance: Silver closed at $78.43, up 1.59%, after staging a sharp recovery from a session low of $76.51. The bounce highlights strong dip-buying interest, though the metal remains below the 50-day SMA at $80.19, keeping short-term momentum constrained. Silver continues to trade well above the 100-day and 200-day SMAs at $65.37 and $51.38, preserving the longer-term bullish structure. Resistance is clustered near $79.47 and the 50-day average, which remains a key pivot. Support is seen at $76.51, followed by the recent swing low near $71.00. A sustained move above $80.19 would strengthen the bullish case, while failure to hold support would reopen downside risks.

Market Movers:

- Omnicom Jumps on Revenue Beat and Fresh Buyback: Shares surged 15% after fourth-quarter revenue came in at $5.5 billion, up nearly 28% year on year, and the board authorised a $5 billion share repurchase programme, including a $2.5 billion accelerated buyback.

- Deere Rallies After Lifting Full-Year Profit Outlook: The stock jumped more than 11% after Deere raised its full-year net income forecast to $4.5 billion–$5.0 billion from $4.0 billion–$4.75 billion.

- Etsy Climbs as Depop Sale to eBay Reshapes Portfolio: Shares advanced 9% after Etsy agreed to sell Depop to eBay for $1.2 billion in cash, while earnings of 92 cents per share beat expectations despite revenue of $882 million landing slightly below consensus.

- Wayfair Slumps as International Sales Disappoint: The stock sank 13% after international net revenue of $395 million came in just below the $398.3 million consensus estimate, overshadowing a quarterly beat on headline earnings and revenue.

- Avis Plunges After Results Fall Well Short of Estimates: Shares tumbled 22% after adjusted EBITDA was just $5 million versus expectations of $145.8 million, while revenue of $2.66 billion also missed the $2.74 billion consensus.

Thursday’s session reflected a clear shift toward caution, as investors reassessed both financial market plumbing and geopolitical risk at the same time. Liquidity concerns in private credit prompted a sharp rotation out of alternative asset managers, while rising oil prices underscored how quickly Middle East tensions are feeding back into broader risk pricing. Despite resilient US labour data and firm import demand, equity leadership remains in flux, with software and select growth areas under renewed pressure. Against this backdrop, stronger relative performance in parts of Asia highlights an uneven global landscape, leaving markets increasingly sensitive to earnings delivery, energy developments, and the durability of underlying economic momentum.