Wall Street finished the week slightly higher as fresh inflation data signalled a continued easing in price pressures, strengthening expectations that the Federal Reserve will lower interest rates next week. Traders assessed the final key economic update before the decision, taking confidence from signs that monetary policy may soon begin to ease while acknowledging some recent softness in labour indicators. With major indices holding close to record territory, attention now turns to whether the central bank will confirm a shift toward easier financial conditions to support momentum into the new year.

Key Takeaways:

- Dow Rebounds into the Close: The Dow Jones Industrial Average gained 104.05 points, or 0.22%, to finish at 47,954.99 as traders positioned ahead of next week’s Federal Reserve decision. The index has risen 0.5% over the week, supported by expectations that easing inflation will allow the central bank to start lowering rates.

- S&P 500 Nears Record on Four-Day Win Streak: The S&P 500 closed up 0.19% at 6,870.40, placing it less than 1% below its all-time intraday high. The benchmark has now advanced in nine of the last ten sessions and gained 0.3% for the week as markets price in a shift toward lower borrowing costs.

- Nasdaq Edges Higher as Tech Gains: The Nasdaq Composite rose 0.31% to 23,578.13, supported by strength in chipmakers and media stocks despite declines among cryptocurrency-linked names. The index advanced nearly 1% over the week, helped by upbeat corporate news and easing inflation pressures.

- Europe Mixed as Growth and Orders Improve: European markets ended broadly flat, with the Stoxx 600 unchanged as investors awaited the Fed meeting. The FTSE 100 is down 53.50 points or 0.55% this week at 9,667.01, while France’s CAC 40 slipped 0.1% to 8,115 and Italy’s FTSE MIB fell 0.2% to 43,433 on Friday. Germany’s DAX rose 0.68% after data confirmed Eurozone GDP grew 0.3% in Q3 and employment rose 0.2%. Italy’s retail sales increased 0.5% month-on-month in October, ahead of forecasts, and German factory orders climbed 1.5%, building on a revised 2.0% jump in September.

- Asia-Pacific Markets Mixed as Japan Falls and Autos Surge in Korea: Asia-Pacific equities delivered a varied performance on Friday. Australia’s ASX/S&P 200 gained 0.19% to 8,634.6. Japan’s Nikkei 225 dropped 1.05% to 50,491.87 and the Topix also fell 1.05% to 3,362.56 as the 10-year government bond yield rose to 1.94%, the highest since July 2007. South Korea’s Kospi jumped 1.78% to 4,100.05, driven by an 11.11% surge in Hyundai Motor and a 2.74% rise in Kia following the US decision to cut tariffs on car imports from South Korea. Hong Kong’s Hang Seng added 0.5% and the mainland CSI 300 increased 0.84% to 4,584.54, led by Moore Threads, which soared more than 400% on its Shanghai debut. India’s Nifty 50 climbed 0.59% after the Reserve Bank of India reduced its policy rate by 25 basis points to 5.25%.

- Oil Supported by Geopolitical Tensions: Brent crude rose 0.89% to $63.82 per barrel and WTI gained 0.85% to $60.18 as stalled Ukraine peace talks offset concerns about oversupply, with Saudi Arabia’s price adjustments and steady OPEC output limiting upside.

- Yields Tick Higher Ahead of Fed Meeting: US Treasury yields edged up, with the 10-year at 4.137%, the 30-year at 4.791% and the 2-year at 3.564% as markets focused on next week’s policy decision and the outlook for easing into early 2025.

- US Core Inflation Eases, Reinforcing Case for Rate Cut: The Fed’s preferred price gauge showed core PCE inflation slowed to 2.8% year-on-year in September, while rising 0.2% month-on-month. Headline PCE matched forecasts at 0.3% monthly and 2.8% annually. The cooler readings support expectations of a rate cut next week, while consumer sentiment strengthened to 53.3.

FX Today:

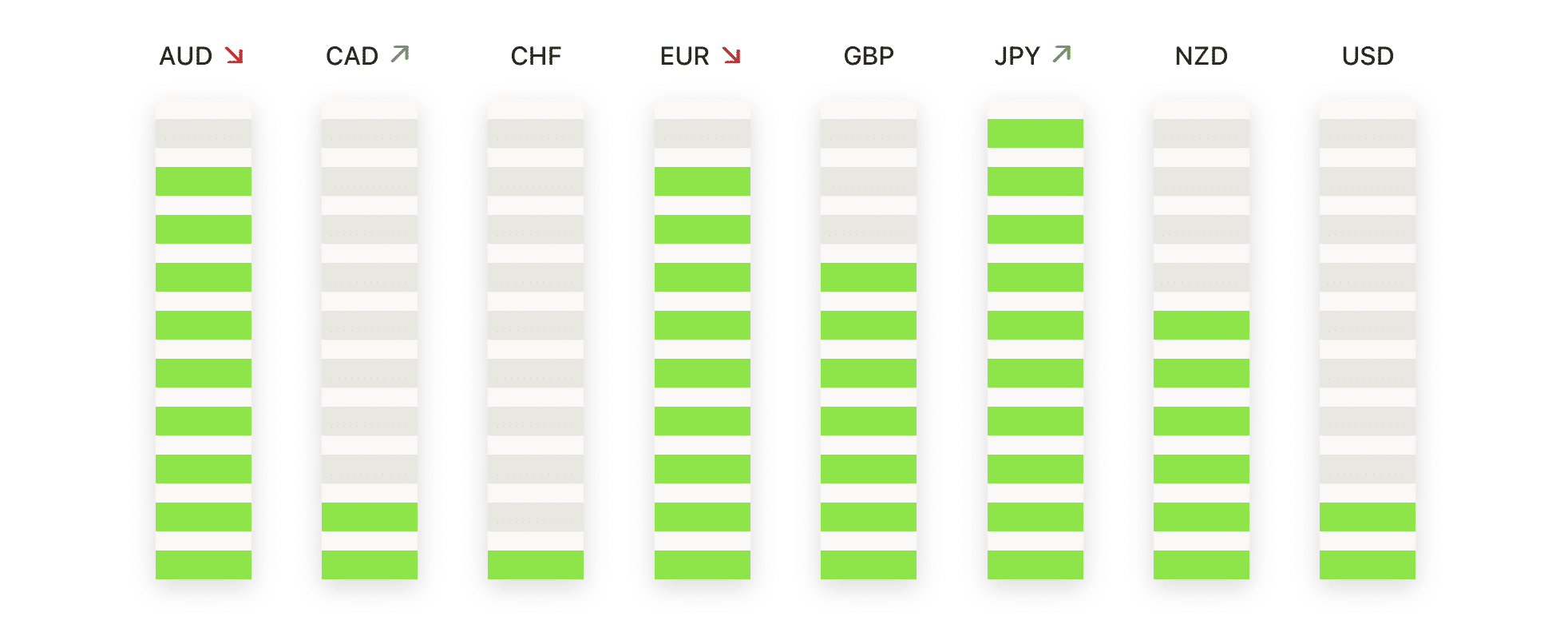

- EUR/USD Holds Above Key Support as Uptrend Continues: EUR/USD rose 0.01% to close at 1.1645 after trading between 1.1672 and 1.1628, finishing near the midpoint of its range. Price remains above the 50-day SMA at 1.1610 and the 200-day SMA at 1.1463, while sitting directly on the 100-day SMA at 1.1645, maintaining the broader bullish structure. The recovery from early November continues with higher highs and higher lows signalling firm underlying demand. Resistance is seen at 1.1672 and then 1.1691, ahead of the October highs near 1.1850. Initial support is at 1.1645 and then 1.1610, and a close below 1.1610 would point toward a deeper retracement into the 1.1550 region.

- GBP/USD Presses Higher After Reclaiming Long-Term Support: GBP/USD edged up 0.06% to 1.3335 after a range of 1.3362 to 1.3316, holding late-session gains above the 200-day SMA at 1.3329. The pair remains capped by the 100-day SMA at 1.3368, with the 50-day SMA at 1.3267 providing underlying support as the rebound off November lows develops. Resistance is focused around 1.3368 and the session high near 1.3362, with a break through 1.3382 opening the way toward 1.3450 and the October high at 1.3550. Support lies at 1.3329 and then 1.3267, with a fall below those levels risking renewed bearish pressure.

- AUD/USD Extends Breakout With Bull Trend in Full Control: AUD/USD climbed 0.47% to finish at 0.6640 after trading between 0.6649 and 0.6605, closing near the top of the daily range. The pair continues to trade well above the 50-day SMA at 0.6533, the 100-day SMA at 0.6536 and the 200-day SMA at 0.6470, confirming strong bullish momentum. Buyers are now targeting the 0.6700 region, aligned with early October highs, with further upside potential toward 0.6750 if strength persists. Support sits first at 0.6605 and then around the 0.6533–0.6536 area, where dip buyers are expected to defend the trend.

- USD/CAD Weakens as Break Below Key Averages Signals Shift: USD/CAD fell 0.95% to close at 1.3825 after moving between 1.3960 and 1.3824, ending near the session low. The pair has dropped below the 50-day SMA at 1.4007, the 100-day SMA at 1.3990 and the 200-day SMA at 1.3910, marking a bearish turn after weeks of consolidation. Downside focus remains on the session low at 1.3824, with further weakness exposing 1.3750, a prior swing low from September, further boosted by a drop in Canada’s unemployment rate to 6.5% in November, and then 1.3650 if bearish momentum persists. Any rebound is likely to encounter resistance at 1.3910 initially and then the 100-day SMAs, which must be reclaimed to ease selling pressure.

- USD/JPY Remains Firm After Shallow Correction: USD/JPY rose 0.16% to close at 155.30 after trading between 155.49 and 154.34, keeping the pair in a tight consolidation near recent highs. The uptrend stays dominant above the 50-day SMA at 153.20, the 100-day SMA at 150.46 and the 200-day SMA at 148.11. Resistance is at 155.49 and then 157.50, a major technical barrier where rallies have stalled previously. Support sits at 154.34 and then 153.20, with only a clean break below the latter suggesting a deeper corrective move toward 151.00 and the 100-day average.

- Silver Drives Higher as Rally Reaches Fresh Peaks: Silver surged 2.27% to settle at $58.39 after trading between $59.33 and $56.89, maintaining a strong upward slope. Price is far above the 50-day SMA at $50.56, the 100-day SMA at $45.10 and the 200-day SMA at $39.46, highlighting a powerful bullish trend. Immediate resistance is at $59.33 before the $60.00 psychological level, while support is at $56.89 and then $55.00, where strong buying recently emerged.

- Gold Consolidates Above Support as Bulls Pause: Gold dipped 0.18% to close at $4200 after ranging between $4260 and $4195, signalling a consolidation phase after recent gains. The metal remains well above the 50-day SMA at $4068, the 100-day SMA at $3767 and the 200-day SMA at $3486, keeping the long-term uptrend intact. Resistance stands at $4260 before the prior swing high near $4350, with initial support at $4195 and stronger support at $4100, where buyers may re-enter if price softens.

Market Movers:

- Netflix Weakens After Announcing WBD Acquisition: Netflix shares ended more than 2% lower despite the strategic move, as investors weighed the scale and timing of the planned $72 billion deal, expected to close within 12 to 18 months. Meanwhile, WBD gained more than 6%.

- Crypto-Exposed Shares Slide as Bitcoin Falls: Galaxy Digital dropped more than 7% and Marathon Holdings fell over 5%, with Riot Platforms down more than 4% and MicroStrategy more than 3% as cryptocurrency prices weakened. Coinbase also slipped more than 1%.

- Rubrick Surges on Revenue Beat and Upgraded Outlook: Shares jumped more than 21% after the company reported Q3 revenue of $350.2 million.

- Parsons Plunges on Contract Loss: Parsons dropped 21% after the FAA and Department of Transportation awarded a key US air-traffic control contract to competitor Peraton.

- SentinelOne Falls on Margin Warning: The cybersecurity stock slid more than 15% after the company guided for a weaker-than-expected operating margin in Q4.

- DocuSign Drops on Revenue Outlook: DocuSign lost more than 8% after forecasting Q4 revenue below the midpoint of consensus expectations, weighing on sentiment in the software sector.

Equities finished the week in positive territory with traders increasingly confident that the Federal Reserve will confirm the first rate cut of the cycle next Wednesday, following further evidence that inflation continues to cool. While overall gains were modest, the market remains well supported near record levels as investors look for clarity on policy direction heading into 2025. Corporate news helped maintain momentum, particularly the headline acquisition agreement between Netflix and Warner Bros Discovery, which kept deal activity in focus. With the final Fed decision of the year now approaching, attention turns to whether softer price pressures and stabilising sentiment can sustain the rally as December progresses.