Friday’s session was shaped by a complex mix of legal clarity, renewed trade uncertainty and softening economic momentum. A Supreme Court ruling altered the landscape for US trade policy, while President Donald Trump’s swift announcement of a new 10% global tariff kept investors cautious. US equities recovered from early weakness triggered by a sharp miss in fourth-quarter GDP, as markets weighed slower growth against the potential impact of shifting tariff policy. Inflation data showing price pressures holding steady added to the cautious tone. Overall, the session reflected selective risk-taking rather than outright optimism, with investors navigating competing policy and macro signals.

Key Takeaways:

- Dow Gains 230 Points After Late Rebound: The Dow Jones Industrial Average rose 230.81 points, or 0.47%, to close at 49,625.97, reversing an earlier decline of more than 200 points after disappointing economic data. Fourth-quarter GDP growth came in well below expectations, initially weighing on sentiment before equities recovered. The Dow finished the week up 0.3%.

- S&P 500 Rises on Tariff Relief Hopes: The S&P 500 advanced 0.69% to close at 6,909.51 as investors welcomed the Supreme Court ruling that the International Emergency Economic Powers Act does not authorise the president to impose tariffs. The index posted a weekly gain of 1.1%.

- Nasdaq Gains as Mega-Caps Lead: The Nasdaq Composite climbed 0.9% to 22,886.07, outperforming broader benchmarks as large-cap technology and consumer internet stocks moved higher. The Nasdaq rose 1.5% on the week, snapping a five-week losing streak.

- European Markets Rally Across the Board: European equities closed sharply higher, taking their cue from the improved tone in US markets following the Supreme Court ruling. The pan-European Stoxx 600 ended the session up 0.8%, with all major bourses in positive territory. The FTSE 100 climbed more than 0.5% to a record close of 10,687, supported by gains in banking and consumer goods stocks. France’s CAC 40 rose 113 points, or 1.35%, to 8,512, while Germany’s DAX gained 199 points, or 0.79%, to 25,242. Italy’s FTSE MIB surged 668 points, or 1.46%, to 46,462. Macro data also supported sentiment, with UK retail sales volumes rising 1.8% year-on-year in January 2026, far above expectations, and the UK posting a record £30.4 billion public sector surplus. In Germany, producer prices fell 3% year-on-year due to an 11.8% drop in energy costs, while the HCOB Flash Germany Composite PMI rose to 53.1, signalling faster business activity. France remained weaker, with the HCOB Flash services PMI at 49.6.

- Asia Markets Mixed as Korea Hits Fresh Highs: Asia-Pacific markets were mostly lower, driven by regional developments after Wall Street declined overnight amid weakness in private credit stocks and rising US-Iran tensions. South Korea’s Kospi stood out, closing 2.31% higher at 5,808.53 for a second consecutive record, powered by a 6.15% gain in SK Hynix and an 8.09% surge in Hanwha Aerospace. Japan’s Nikkei 225 fell 1.12% to 56,825.7, while the Topix declined 1.13% to 3,808.48, despite PMI data showing the strongest expansion since May 2023. Japan’s core CPI rose 2.0% year-on-year in January, in line with expectations, and the 10-year government bond yield fell 4 basis points. Hong Kong’s Hang Seng slipped 0.98% to 26,443.69, weighed down by technology stocks, while mainland China markets were closed for the Lunar New Year. Australia’s ASX 200 edged lower to 9,081.40, and New Zealand’s NZX 50 fell 122 points, or 0.9%, to 13,322 despite the trade deficit narrowing to NZD 519 million from NZD 549 million.

- Oil Holds Near Six-Month Highs on Iran Risk: Oil prices were broadly stable as investors monitored tensions in the Middle East after President Trump said he was considering a limited military strike to pressure Iran over its nuclear programme. Brent crude futures with April delivery rose 10 cents to settle at $71.76 per barrel, while US West Texas Intermediate futures with March delivery slipped 4 cents to $66.39. Both contracts had settled at six-month highs in the previous session, keeping geopolitical supply risks firmly in focus.

- 10-Year Treasury Yield Ticks Higher as Fiscal Worries Build: The 10-year US Treasury yield rose less than 1 basis point to 4.083% as investors digested the Supreme Court ruling and the day’s macro data. The 30-year Treasury bond yield climbed 2 basis points to 4.724%, while the 2-year note yield rose more than 1 basis point to 3.482%. Bond investors focused on the possibility that reduced tariff revenue could add to fiscal deficit concerns, potentially weighing on demand for US debt.

- GDP Miss and Sticky Inflation Keep Rates in Focus: Fourth-quarter US GDP rose at an annualised rate of 1.4%, sharply below the 2.5% increase expected by economists polled by Dow Jones and down from a 4.4% gain in the third quarter. The Commerce Department said the record-breaking government shutdown shaved roughly 1 percentage point from growth during the quarter. Inflation data showed price pressures remained firm, with core PCE holding at 3% in December and headline PCE accelerating to 2.9%. Both measures rose 0.4% on the month, exceeding expectations and reinforcing the Federal Reserve’s cautious stance.

FX Today:

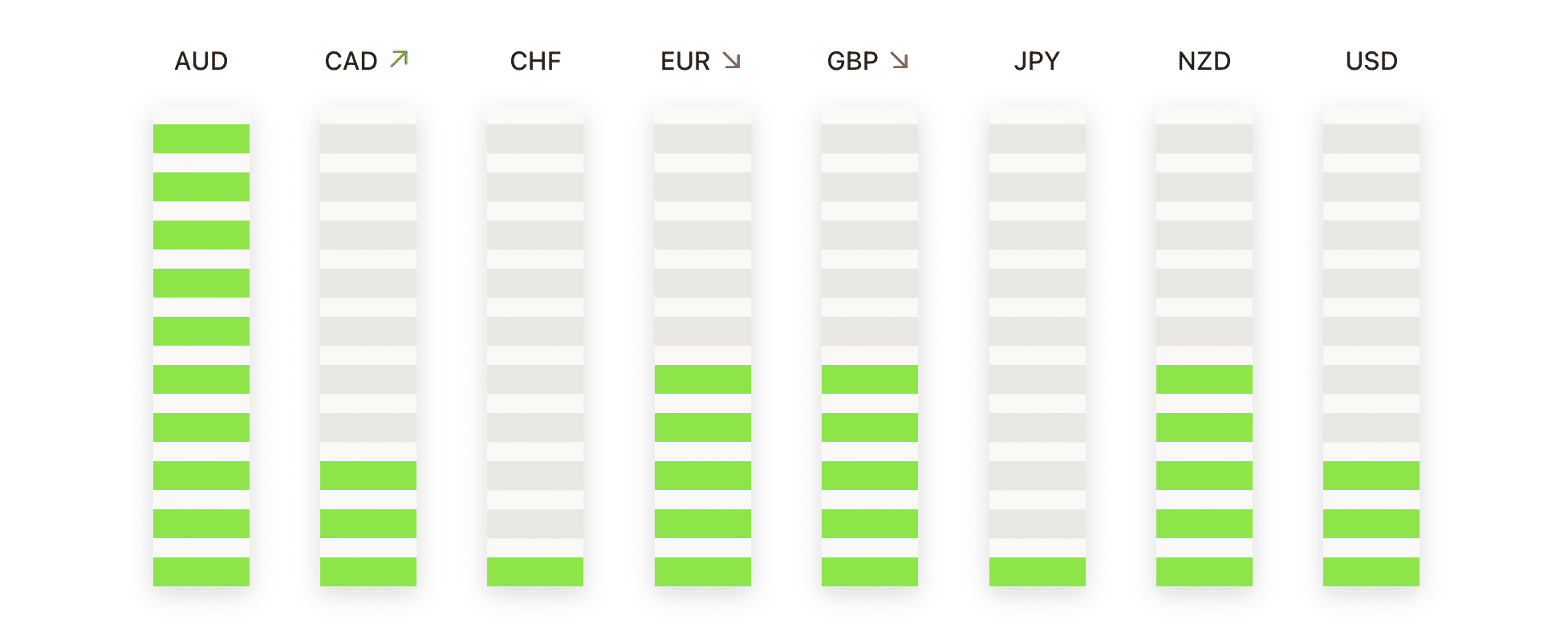

- EUR/USD Stabilises Above 50-Day Support: EUR/USD closed at 1.1777, up 0.11%, after trading between a high of 1.1808 and a low of 1.1744. The pair ended the session marginally above the 50-day simple moving average at 1.1772, confirming this area as near-term support amid consolidation. EUR/USD remains well above the 100-day SMA at 1.1689 and the 200-day SMA at 1.1648, maintaining a constructive medium-term structure. The broader trend reflects higher highs and higher lows since late 2025. Momentum has cooled following the early February peak, pointing to consolidation rather than reversal. Immediate resistance is located at 1.1808, with further upside capped near the early February swing high above 1.2000. Initial support rests at 1.1744, followed by the 100-day SMA.

- GBP/USD Trades Sideways Near Key Averages: GBP/USD closed at 1.3490, up 0.19%, after oscillating between a high of 1.3515 and a low of 1.3438. The session reflected narrow-range trading as the pair consolidated following its recent pullback from February highs. Price remains below the 50-day SMA at 1.3527, which continues to act as a near-term ceiling. However, the pair is holding above the 200-day SMA at 1.3444, helping to stabilise the broader structure. The 100-day SMA at 1.3394 provides additional downside protection if selling pressure resumes. While the broader trend from late 2025 remains positive, near-term momentum has softened. Resistance is seen at 1.3515 and then the 50-day SMA, while initial support is located at 1.3438.

- AUD/USD Recovers From Intraday Lows: AUD/USD settled at 0.7083, up 0.41%, after rebounding from a session low of 0.7015 and trading as high as 0.7095. The recovery highlighted renewed buying interest following the recent dip from February highs. Price remains well above the 50-day SMA at 0.6831, the 100-day SMA at 0.6683, and the 200-day SMA at 0.6602, all of which continue to slope higher. This alignment confirms that the broader uptrend remains intact despite near-term consolidation. Immediate resistance is located at 0.7095, followed by the recent peak around 0.7150. Initial support sits at 0.7015.

- Gold Surges Back Above $5,000: Gold closed at $5095, up 1.88%, after trading between a low of $4982 and a high of $5096. The strong rebound followed the sharp correction earlier in the month, with buyers stepping in decisively to reclaim key psychological levels. The close near the session high signalled renewed bullish momentum. Gold remains firmly above its 50-day SMA at $4682, the 100-day SMA at $4379, and the 200-day SMA at $3889, reinforcing the strength of the longer-term trend. Immediate resistance is seen at $5096, followed by the prior peak near $5600. Initial support is located at $4982.

- Silver Reclaims 50-Day Average on Sharp Bounce: Silver closed at $84.51, up 7.61%, after trading between a high of $84.81 and a low of $77.49. The session delivered a powerful recovery, with the market closing near the day’s high and signalling strong buying pressure. Silver recaptured the 50-day SMA at $80.73, strengthening the near-term technical picture after the recent correction. The metal remains well above the 100-day SMA at $65.78 and the 200-day SMA at $51.62, confirming the broader bullish trend. Immediate resistance is located at $84.81, with initial support at $77.49.

Market Movers:

- Akamai Technologies Slumps on Weak Guidance: Shares of the cloud computing company plunged 14% after issuing weaker-than-expected guidance.

- Grail Craters After Failed Drug Trial: Shares collapsed around 50% after the company said a clinical trial for one of its drugs failed to meet its primary endpoint. The study did not show a statistically significant reduction in Stage III-IV cancer.

- Cloudflare Declines Amid AI Security Competition: Shares fell more than 8% as cybersecurity stocks broadly sold off following the introduction of a new AI-driven security feature by Anthropic. Investors worried automated code scanning could disrupt traditional cybersecurity platforms.

- RingCentral Surges Following Earnings Beat: Shares jumped more than 32% after reporting fourth-quarter adjusted earnings of $1.18 per share, beating expectations.

Friday’s session highlighted a market attempting to balance improving policy clarity with persistent macroeconomic challenges. The Supreme Court ruling removed a significant source of uncertainty around tariffs, offering relief to sectors exposed to global trade, even as the announcement of a new global levy limited enthusiasm. Slower growth and stubborn inflation kept caution elevated, particularly in rates markets. Strength in European equities and selective resilience in Asia underscored the role of regional drivers. With fiscal concerns, trade policy and central bank decisions still in focus, markets look set to remain sensitive to incoming data and headlines.